This post may contain affiliate links; please see our disclaimer for details.

Hello F.I.R.E. friends!

Budgeting for expenses, savings, and investments each month is imperative to achieving financial independence.

We hope that you will receive some valuable insights by seeing our monthly spending breakdown.

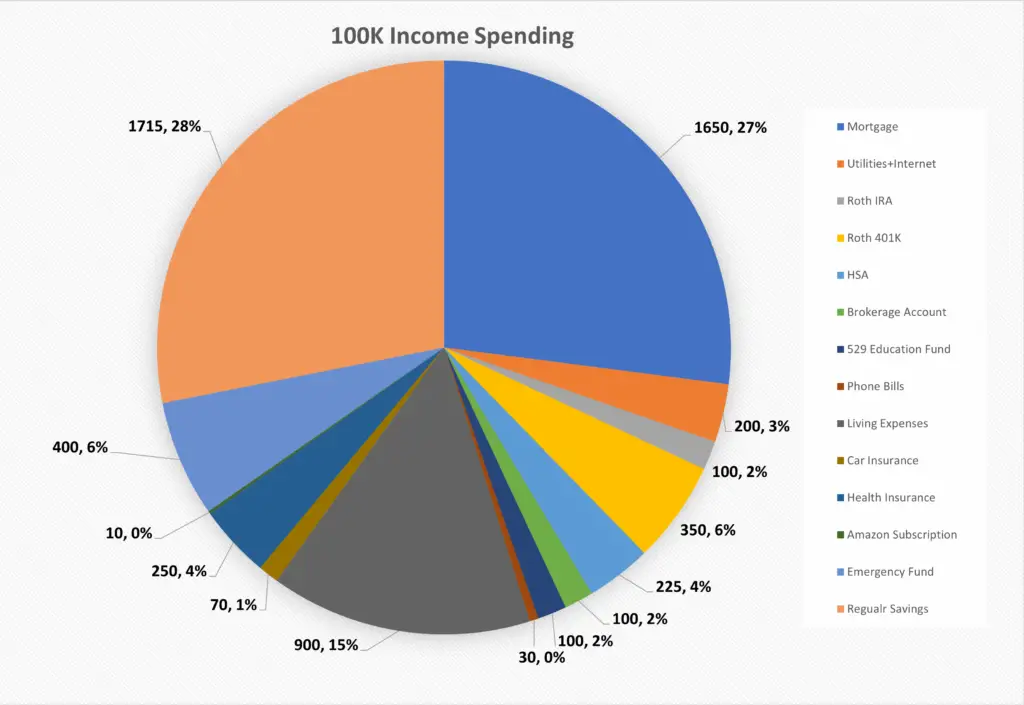

My wife and I’s total pre-tax income is currently $100,000, including both of our salaries (basic salary + bonuses) and our extra rental income.

After taxes, we are at $7,000 a month net income.

Now I’d like to share with you how we spend our $100,000 income as a family of 3 (soon to be 4)!

Here is a video of this content if you prefer to watch it instead!

Table of Contents

1. Housing Expenses

Our largest expense comes from our monthly mortgage payments. When applying for our house loan, we tried to keep all of our house costs (mortgage+utilities+internet) under 30% of our net income.

The goal is to keep our mortgage payment as low as possible.

We feel this is a healthy percentage and don’t want to max out our house loan debt because we’d rather not be house poor.

We want extra money to invest!

2. Investment Accounts

We are completely debt-free except for the mortgage. This allows us to use more of our income to invest! As you can see from the pie chart, most of our income is going to tax-advantaged accounts/retirement accounts.

My wife and I chose to use Roth IRAs because we don’t want to worry about tax at all when we retire. The thought of being a tax-free millionaire in the future is very exciting.

My wife holds her IRA at Vanguard and mine is with Fidelity. Both investment companies have been great to work with!

If interested, I wrote another article explaining the 5 key differences between Roth IRAs and Traditional IRAs.

After paying off our student loan debt we started to max out our two Roth IRAs each year. The max contribution is $6000 per IRA, so we invest $12,000 total for both of us. We also contribute enough to our companies’ Roth 401Ks to get the company match. Our companies match 4% but we have to contribute 5% to obtain the full 4%.

My wife and I are on separate health insurance plans. I have an HDHP plan and my company matches the money I put into my HSA.

I max out my HSA every year which is $3,200 and invest most of the money into an HSA because it has triple tax benefits and can also be your secondary/regular retirement account when you are 65 years old.

Related Content: Why Invest In A Health Savings Account (HSA)

2022 HSA Contribution Limits

In 2022, you can contribute up to $3,650 for self-only coverage and up to $7,300 for family coverage into an HSA. HSA funds roll over yearly if you don’t spend them and never expire. That’s about a 1.5 percent increase from 2021. Let’s invest more in 2022!

We invest $100 into our regular brokerage account and another $100 for our son’s 529 education fund. Invest in your kid’s future if you can, even just $10 a month!

Small contributions can really add up over time.

Compound interest is the most wonderful thing in the world!

3. Phone Bill

We pay only $15 each per month for our phone bill!

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

4. Living Expenses

Our living expenses include food, outside eating, gas, etc. We have a baby so there are also formula and diaper costs too. We try very hard to minimalize and only spend money on things we need and buy items when on sale.

5. Insurance

We only have one car right now (paid off), and our car insurance is $70 per month. Health insurance and life insurance are through our employers and are $250 a month for our family of 3. Combining all insurances cost totals 4.9% of our monthly net income.

6. Subscriptions

Amazon Prime is currently our only Subscription and it’s been amazing! The most benefits we love are free 2-day shipping and unlimited photo storage space! Amazon Music is also a great plus. It totally worth the money because we have tons of photos!

The monthly cost is $12.99 (plus taxes), and if you buy yearly like us will be even cheaper at $119 (plus taxes). If you are a student, it will be $6.49 per month and $59 yearly.

8. Savings

We transfer $400 a month to our High Yield Saving Account – our Emergency Fund. We will keep transferring money until we save enough for 6 months of expenses.

During times like the 2008 economic recession and COVID-19, tons of people lost their jobs. An emergency fund isn’t just in case of losing a job but also applies to other big and sudden things that happen in life.

For example, the car engine might just break down. Just imagine having enough money in a specific account for all types of emergencies – the peace of mind is real.

We also have a regular savings account. After our expenses, investments, etc., all the rest of the money we have left goes to our standard savings account for other purchases like Christmas gifts, new clothes, travel, even our next house down payment, etc.

Are you looking for a robust app to help you gain awareness of your spending habits and stay on top of budgeting? If so, we highly recommend Rocket Money (formerly Truebill). Their app is extremely easy to use and can help you gain better control over your finances and know your net worth. Feel free to check them out today!

| Mortgage | 23.6% | $1,650 |

| Utilities+Internet | 2.9% | $200 |

| Roth IRA | 14.3%: | $1,000 |

| Roth 401K | 5% | $350 |

| HSA | 3.2% | $225 |

| Brokerage Account | 1.4% | $100 |

| 529 Education Fund | 1.4% | $100 |

| Phone Bills | 0.4% | $30 |

| Living Expenses | 12.9% | $900 |

| Car Insurance | 1.0% | $70 |

| Health Insurance | 3.6% | $250 |

| Amazon Subscription | 0.14% | $10 |

| High Yield Saving account/Emergency Fund | 5.7% | $400 |

| Regular Savings | 24.5% | $1,715 |

| Total | 100% | $7,000 |

Now you know how we spend our $100,000 income as a family of 3.

Comment below or email and tell us how you budget your income! Share with us any other money-saving tips you use!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!