This post may contain affiliate links; please see our disclaimer for details.

Managing money is a huge source of stress for a lot of people. Figuring out how to effectively manage your money can be daunting, but it doesn’t have to be.

There are some simple rules that you can follow to help make managing your finances easier. The 50/30/20 rule is one such rule.

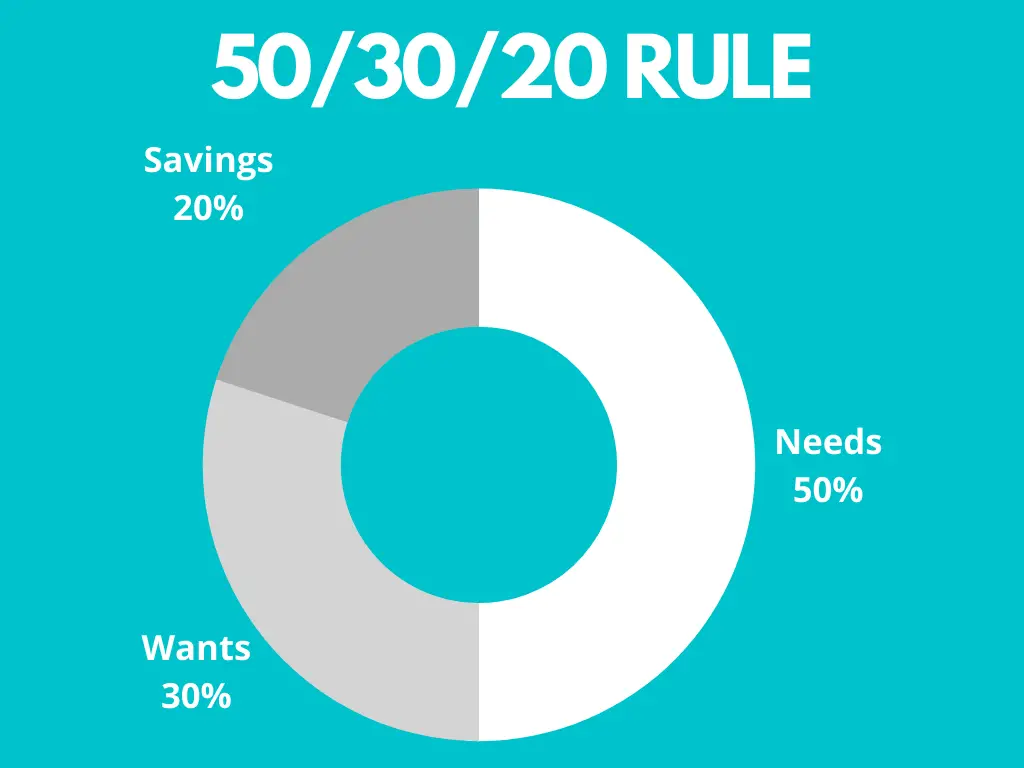

The method states that you should allocate 50% of your income toward essentials, 30% towards wants, and 20% towards savings.

In this article, I discuss the 50/30/20 rule in more detail and provide tips on how to apply it to your own life!

Related Content: How We Save 56% of Our Income [Family of 3]

Table of Contents

What Is The 50/30/20 Rule?

The 50/30/20 rule is a simple and effective way to manage your money. The rule states that you should spend 50% of your income on necessities, 30% on wants, and 20% on savings and debt repayment.

This may seem like a lot of work, but it doesn’t have to be.

You can start by creating a budget and tracking your spending for a month. This will give you an idea of where your money is going and where you can cut back.

Once you understand your spending patterns, you can begin to implement the 50/30/20 rule.

Start by allocating 50% of your income to necessary expenses such as rent, food, transportation, and utilities.

Then, allocate 30% of your income to wants such as entertainment, dining out, and shopping.

Finally, allocate 20% of your income to savings and debt repayment.

If you spend more than 50% of your income on necessities, try to find ways to cut back.

For example, you may save money on food by cooking at home more often or cutting back on unnecessary expenses.

If you are spending more than 30% of your income on wants, try to find ways to reduce your spending in this area.

For example, you may save money by watching movies at home instead of going out to the theater.

The 50/30/20 rule is a great way to get a handle on your finances.

By following this rule, you can ensure that you are spending your money in a way that is both responsible and enjoyable. So what are you waiting for? Start budgeting today!

Where Did The 50/30/20 Rule Come From?

The 50/30/20 rule is a personal finance guideline popularized by Senator Elizabeth Warren in her book, All Your Worth: The Ultimate Lifetime Money Plan.

The 50/30/20 budgeting method is designed to help you assess your financial needs and make changes to your spending habits if needed.

The goal is to end up with a balanced budget at the end of each month.

How To Budget Your Money With The 50/30/20 Rule?

The 50/30/20 rule is simple. You take your after-tax income and divide it into three categories:

How to budget your money with the 50/30/20 rule

- 50% goes towards needs like rent, food, transportation, and utilities

- 30% goes towards discretionary spending like entertainment, dining out, shopping, etc.

- 20% goes towards savings or debt repayment

Let’s say you make $2000 per month. With the rule, you would only have 50% of that to spend on living costs which is $1000. This probably means you won’t be able to get an upscale apartment or enjoy the luxury of the finest groceries and utilities.

30% of $2000 would be $600. That’s the amount you can spend on fun activities such as eating, watching a movie, or taking a trip.

The final 20% is $400. You would save or use this to pay off debt each month. In this particular scenario, the budget will look like $1000/$600/$400.

This leaves little room for error and forces you to be mindful of every penny you spend. However, it can be a great way to get your finances in order and start saving money.

The rule is flexible, though—if you have high student loan payments or are trying to save up for a down payment on a house, you can adjust the percentages accordingly.

The most important thing is that you are aware of your spending and are trying to save money.

The key concept is to ensure that the 20% assigned for savings and debt repayments does not go any lower.

It can be helpful to increase that number, but you should never look to decrease it.

Be careful with these other common mistakes when using the 50/30/20 rule…

Not including all expenses: When budgeting with the 50/30/20 rule, include all necessary expenses in the 50% category. This includes your phone bill, internet service, and health insurance.

Forgetting to account for irregular expenses: Remember to account for expenses that occur less often, such as car insurance and property taxes.

Treating the 50/30/20 rule as a hard and fast rule: The 50/30/20 rule is meant to be a guideline, not a strict set of rules. If you find that you can’t stick to the percentages exactly, don’t worry. Just try to get as close as you can and adjust as needed.

Examples of The 50/30/20 Method

Earlier in this article, we used the example of an income of $2000 per month. Let’s explore some more examples of different situations and levels of income.

If you earn $4000 per month, you will break it down into:

- $2000 for 50% needs

- $1200 for 30% wants

- $800 for 20% savings & debt repayment

You earn $8000 per month, you would break it down into:

- $4000 for 50% needs

- $2400 for 30% wants

- $1600 for 20% savings & debt repayment

If you earn $12,000 per month, you will break it down into:

- $6000 for 50% needs

- $3600 for 30% wants

- $2400 for 20% savings & debt repayment.

The lessons from these examples are that your percentages will always stay the same, but the actual dollar amounts will obviously change based on your income.

Another thing to remember is that these are just guidelines, and you can adjust them according to what works best for you and your unique financial situation. It’s important to tailor this rule (or any financial rule, for that matter) to fit your own life and needs.

Now that we’ve gone over the basics of the 50/30/20 rule, let’s talk about how you can implement it in your own life.

Here are the steps to getting started…

Determine your after-tax monthly income: This is the amount of money you have to work with each month after taxes, and other deductions have been taken out of your paycheck.

Track your spending for one month: This will give you a good idea of where your money goes each month and where you may be able to cut back to save more.

Calculate your 50/30/20 breakdown: Once you know how much money you have to work with each month, you can start allocating it into different categories.

Make a budget and stick to it: This is probably the most important step in managing your money effectively. Once your budget is set, please do your best to stick to it as closely as possible.

Review and adjust as needed: As we said before, these guidelines are just that – guidelines. They’re not set in stone, so if something isn’t working for you or your circumstances have changed, don’t be afraid to adjust your budget accordingly.

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

They offer free financial tools and many resources to help you achieve your financial goals! See how you can better understand and manage your money today!

Why The 50/30/20 Rule Generally Works

This rule works so well because it forces you to think about your spending differently. Most people spend all their money on wants and then try to save whatever is leftover.

The 50/30/20 rule flips that around by ensuring you save money and use the remaining amount for your wants.

The 50/30/20 rule is a great way to start saving and budgeting because it provides a simple framework you can follow.

Once you understand how the rule works, you can start to tweak it to better suit your needs.

For example, if you have a lot of debt, you may want to adjust the percentages to put more toward debt repayment.

How the 50/30/20 Method Works

You spend 50% of your income on necessities like housing, food, transportation, and healthcare. This number works because, for most people, these expenses stay relatively constant from month to month.

30% of your income goes towards wants or discretionary purchases. This could include things like travel, entertainment, and clothes. Using 30% should work for these purchases because they shouldn’t cost more than your living expenses.

It also gives a fair amount of wiggle room for unexpected expenses.

20% of your income is saved or invested for the future. This could be for retirement, an emergency fund, or other financial goals.

Consistently saving, investing, or paying down debt with 20% of your income works because it allows you to make significant progress on your long-term financial goals.

Is The 50/30/20 Budget Right For You?

Ask yourself these questions to find out if the 50/30/20 budget is right for you.

- Do I have a shopping habit?

- Do I get paid a lot but don’t have money to pay down debt?

- Do I have trouble setting a framework for my personal finances?

- Do I need to start budgeting to have more financial freedom?

If you answered “yes” to any of the above questions, the 50/30/20 budget might be a good fit for you.

If you find that you are not able to stick to the 50/30/20 rule, don’t worry. The most important thing is that you start trying to save and budget your money.

The 50/30/20 Rule Is Right for you if…

- You want a simple framework to follow

- You need help allocating your income into different categories

- You want to start saving and budgeting but don’t know where to begin.

It’s up to your lifestyle & money choices

In some circumstances, the 50/30/20 budget might not be right for you. This can be true for those that don’t need to spend anywhere close to 30% on fun activities and have most of their living expenses covered (living with relatives, walking to work or working from home, etc.)

If you have high debt or want to save to invest sooner, you can adjust a percentage from the 30% fun category and increase your 20% savings column.

For some people, the rule can look like 50/10/40. This scenario would result in very little discretionary spending, but it will also get you out of debt or save for investments much more quickly.

If you have low living expenses and not much desire to spend on fun activities. The rule in this case, can look something like 30/10/60. This means 30% goes to living expenses, 10% to fun, and 60% to savings, debt repayment, and investing.

This accelerated rule is a great way to reach financial freedom faster, but it can be stressful. That’s why the 50/30/20 rule is great. It’s a stress-free and manageable way to budget effectively!

So is the 50/30/20 budget right for you?

As you can see, there is no one-size-fits-all answer to this question. The 50/30/20 budget may be right for you, or you may need to adjust it to fit your unique circumstances. The most important thing is to make an effort to save and budget your money.

Try out different methods and see what helps you save the most money.

You may even want to try using multiple methods at once. However, this can overcomplicate things. That’s why the 50/30/20 rule is the perfect standard to follow.

For most people, the 50/30/20 budget is a great starting point. It’s simple and easy to follow, making it perfect for those just getting started with budgeting.

If you believe you can benefit from the 50/30/20 budget, give it a try! You may be surprised at how much easier it is to save money than you thought.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!