The main differences between renting and buying a home include the type of contract, monthly payments, credit score requirements, and upfront costs.

When you rent a home, you sign a lease agreement that typically lasts one year. This allows you to move if your job changes or you want to live elsewhere.

You’ll also have to pay a security deposit equal to one month’s rent, which is usually refundable if you leave the rental in good condition.

Monthly rent payments are generally lower than mortgage payments because you’re only paying for the use of the property – not the entire purchase price.

A credit score is not required to rent a home, but most landlords will check your credit history to see if you’ve been a responsible borrower.

When you buy a home, there are several upfront costs you’ll need to pay, including the down payment, closing costs, and home inspections.

This cost can add up to thousands of dollars, so saving up in advance is important.

The type of contract needed is a mortgage loan that must be repaid over 15 to 30 years. It’s important to keep in mind that your monthly payments will be higher than if you were renting.

You’ll also need a good credit score to qualify for a mortgage. That’s why it’s important to start building your credit score now.

A down payment ranging from 3-20% of the home’s purchase price is also required.

If you want your monthly mortgage payments to be lower, you can pay more than the required down payment.

Although the mortgage payments can be high, you can consider renting out a room or the basement to tenants to help offset the costs.

As the homeowner, you have this option where a renter does not.

Of course, you can avoid the mortgage entirely if you have the cash to pay for the property outright.

However, you still need to factor in the costs of homeownership such as maintenance, property taxes, and homeowners insurance.

Another difference to consider is that buying a home is an investment that can appreciate over time.

This means the value of your home could increase, and you could make money if you sell it in the future.

If you own a home, it can also be difficult to move if you aren’t happy with where you live.

In this case, you would need to sell the property, which can take time and money. As a renter, you can move with much less hassle.

Now that we’ve gone over some of the key differences between renting vs. buying, let’s consider whether you should buy a house based on your own lifestyle and preferences.

Should I Buy a House?

Renting vs. buying is a personal decision that depends on your financial situation, lifestyle, and long-term goals.

If you’re not ready to commit to property ownership or don’t think you can afford the monthly payments, renting may be your best option.

On the other hand, buying may be the way to go if you have a steady income and are looking for a place to call home. This is a common occurrence for young couples looking to start a family or those who want to plant roots in their community.

As mentioned earlier, you’re responsible for maintenance and repairs when you own a home. This could be anything from a broken window to a leaky roof. But, you’ll build equity in your home as you make mortgage payments.

Another factor to consider is your lifestyle. Renting may be the better option if you like to move around frequently. With renting, you can move when your lease is up.

On the other hand, buying a house may be the right choice if you’re looking for a more stable environment. Once you close on a property, it’s yours for as long as you’d like.

It’s also important to remember that where you live also plays a role in this decision. In some areas, it’s more expensive to buy a home than in others.

For example, the average cost of a home in San Francisco is nearly $1 million while the average cost in Omaha is around $250,000.

If you answer “Yes” to the following questions, you may benefit from buying a home.

Do you plan on staying in the same area for at least five years?

Are you ready to commit to a 15- or 30-year mortgage?

Do you have a down payment saved up?

Do you have good credit?

Are you prepared to handle maintenance and repairs?

It’s important to think about your long-term goals when making the rent vs. buy decision. Renting could be a better option if you want to move in the next few years.

But, if you plan on staying in one place for a while, buying a house could be the way to go. Buying a home is a major financial commitment that should not be taken lightly.

Buying Pros and Cons

The biggest advantage of owning a home is building equity over time. With each mortgage payment, you’re slowly paying off the loan and increasing your ownership stake in the property.

Another benefit of owning a home is that you can make changes and improvements as you see fit.

You can paint the walls, renovate the kitchen, or add a deck without having to get permission from your landlord.

Here are a few more benefits of homeownership:

You may be able to deduct mortgage interest and property taxes on your income taxes

Your monthly payments will stay the same while rent prices continue to increase

You’ll have a place to call your own and can build long-term wealth

While there are many advantages to buying a home, there are also a few drawbacks to keep in mind.

The biggest disadvantage of owning a home is that it’s a major financial commitment. Once you sign a mortgage, you’re responsible for the payments even if you lose your job or have other financial setbacks.

Another downside of owning a home is that you’re responsible for all the payments. You may have to sell your home if you can’t make ends meet. Foreclosure is a possibility if you can’t keep up with your mortgage payments.

Here are some drawbacks to consider before buying a home:

You’ll need to come up with a down payment, usually around 20% of the purchase price

You’ll have to pay for closing costs, which can be around $2000 – $5000

You may need to get private mortgage insurance if you don’t have a 20% down payment

Now that we’ve gone over the pros and cons of buying vs. renting let’s consider whether it would be a better financial decision to rent a home instead.

If you are tight on cash and looking for an affordable way to invest in Real Estate now, then FUNDRISE is an excellent choice. They provide a crowdsourcing real estate investing platform where the investing minimums are only $10.

Should I Rent a House?

If you are considering renting a house, you should consider all possibilities. Renting a house can be a great option if you are not ready to buy a home, are looking for a short-term solution, or do not have the necessary down payment.

If you answer “Yes” to the following questions, you may benefit from renting a home.

Do you plan on moving in the next few years?

Would you prefer not to have to maintain a home?

Do you want to live in a luxurious home without a long-term financial commitment?

If you answered “Yes” to any of the questions above, renting might be the best option. However, renting may not be suitable for you.

If you do not like paying someone else’s mortgage or want to build equity in a property, then renting might not be the best option.

While renting may seem easier and more affordable, it’s important to weigh all the pros and cons before making a decision.

Renting Pros and Cons

The main advantage of renting is that it’s a more flexible arrangement than buying a home.

If you need to move for work or personal reasons, it’s usually easier to find a new place to rent than it is to sell a home.

Another benefit of renting is that you don’t have to worry about maintenance and repairs. If something breaks, it’s usually the landlord’s responsibility to fix it.

Here are some more benefits of renting:

You don’t need a large down payment

Your monthly payments will be lower than if you were to buy a home

You’re not responsible for property taxes or homeowners insurance

While there are many advantages to renting, there are also a few drawbacks.

The biggest disadvantage of renting is that you’re not building any equity in the property. You’re essentially throwing your money away each month instead of investing in a home you will eventually own.

Another downside of renting is that you may not have as much control over your living situation. For example, if your landlord decides to sell the property, you may have to move.

Here are some more drawbacks to consider before renting a home:

Your rent could go up at any time

You may not be able to make changes to the property

You’re at the mercy of your landlord

Now that we’ve gone over the pros and cons of buying vs. renting, you should know which option is best for you.

The Bottom Line

There are pros and cons to both renting and buying a home. It’s important to weigh your options and decide what’s best for you based on your circumstances.

Each option can have its benefits and disadvantages.

You can make the best decision by assessing your preferences and circumstances.

Feel free to share this article with anyone considering renting or buying a home soon!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

There are a lot of factors to consider when deciding whether to buy or build a house.

This blog post will discuss the pros and cons of buying and building a home so you can make an informed decision about what is best for your family!

This post may contain affiliate links; please see our disclaimer for details.

Is it Cheaper to Buy or Build a House?

The answer to this question depends on several factors.

For starters, you need to consider the housing market’s current state.

If your area rises, buying an existing home now may be cheaper than waiting and building later.

On the other hand, building a new home may be a better option if prices are falling or are expected to fall since you can lock in today’s prices for materials and labor.

Another factor to consider is the cost of land.

If you already own a piece of property, then building a new home will be cheaper than buying an existing one since you won’t have to pay for the land.

However, if you don’t own any property and need to buy a lot on which to build, that will increase the cost of building a new home.

You also need to think about the type of home you want.

If you’re looking for a particular type of home that’s not common in your area, it may be cheaper to build it yourself rather than try to find an existing home that meets your needs.

On the flip side, if you’re looking for a basic starter home, there are probably plenty of existing homes on the market that would fit your needs and budget.

Labor costs should also be considered when making your decision.

If you can find a good deal on labor, then building a new home may be cheaper than buying an existing one.

You do not want to skip on the quality of labor if you want a quality and safe home.

Permits and fees are another important consideration.

If you’re planning to build a new home, you’ll need to obtain the necessary permits and pay any associated fees.

These costs can add up, so be sure to factor them into your decision. Some permits that you would need are a building permit, a zoning permit, and a septic tank permit.

You may also be responsible for renting specialized machines and equipment for your laborers, such as a Bobcat or an excavator.

These additional expenses can add to the costs, so make sure you factor them in.

You would also need to buy insurance for your new home, which can be expensive. The insurance cost depends on the size and location of your home and the type of coverage you choose.

Both built and bought homes need to be insured, so this is an important consideration for both options.

However, providers will often give discounts for new homes since they’re less likely to have claims.

Another factor that can determine if building a house is cheaper would be the climate. If you live in an area with a warm climate, it would be cheaper to build a house since there’s no need for special materials or equipment to protect against the elements.

If you live in an area with a cold climate, building a house would be more expensive since you’ll need to use special materials and equipment to protect against the elements.

You should also consider the availability of materials when making your decision.

Finding good deals on materials could make building a new home cheaper than buying an existing one.

However, if materials are limited in your area, it may be more expensive to build a new home.

A period of high inflation may raise the prices of basic building materials such as lumber, resulting in more costs to build your new home.

This should be considered as constructing a new home typically takes at least several months.

It can be cheaper to buy a house if:

You’re able to find a good deal on an existing home

The market in your area is favorable

The cost of land is high

You only need a small or starter home

Building a house can be cheaper if:

You want a particular type of home that’s not common in your area

The market in your area is not favorable.

You’re able to find a good deal on labor

You already own the land on which you would build.

The climate in your area is favorable.

The availability of materials in your area is good.

Ultimately, there is no simple answer to the question, “Is it cheaper to buy or build a house?”

However, by considering all the factors mentioned above, you should be able to make the right decision.

Example story of when building a house would be cheaper:

Susan and Abel recently came across the idea of building an Earthship. After seeing the housing costs rise beyond their budget, they decided they would rather build an Earthship themselves.

They are both retired and were able to purchase property away from the city for a lower price.

They could find a good deal of labor through friendships and volunteers. The couple purchased the necessary permits and paid any associated fees.

Luckily, there weren’t too many because they were building their home outside of the city.

With some friends’ help, they could find all the materials they needed for their home at a fraction of the cost.

Abel and Susan now live in their own Earthship and couldn’t be happier with their decision to build rather than buy.

In this example, it was cheaper for Susan and Abel to build their own home because they could find a good deal on labor and materials.

They could also purchase their land for a lower price because they bought it outside the city.

Example story of when building a house would be more expensive:

The Joneses have been known for always having the nicest house on the block. When they decided it was time for an upgrade, they knew they wanted something that would wow their neighbors.

Since they couldn’t find a unique house to meet their needs, they decided to build their own.

They hired an architect to design their home and a contractor to oversee the construction.

The materials they used were all high-end and custom-made. The Joneses had to pay for the necessary building permits and fees.

The attention of their neighbors was caught, but not in a good way. Multiple fines were given for various violations, including noise and construction hours.

The Joneses also decided to stay at a luxury hotel rather than being seen at a lower-end one while their home was being built.

In the end, the Joneses got the unique home they wanted. The cost to them was a lot more compared to buying an existing home.

In this example, it was more expensive for the Joneses to build their own home because they hired an architect and a contractor.

They also used high-end materials that were custom-made. These factors all contributed to the increased cost of building their home.

When considering whether to buy or build a house, try writing out your personal story and how each option would affect you.

Building a house can be cheaper than buying one, but it depends on each individual’s circumstances.

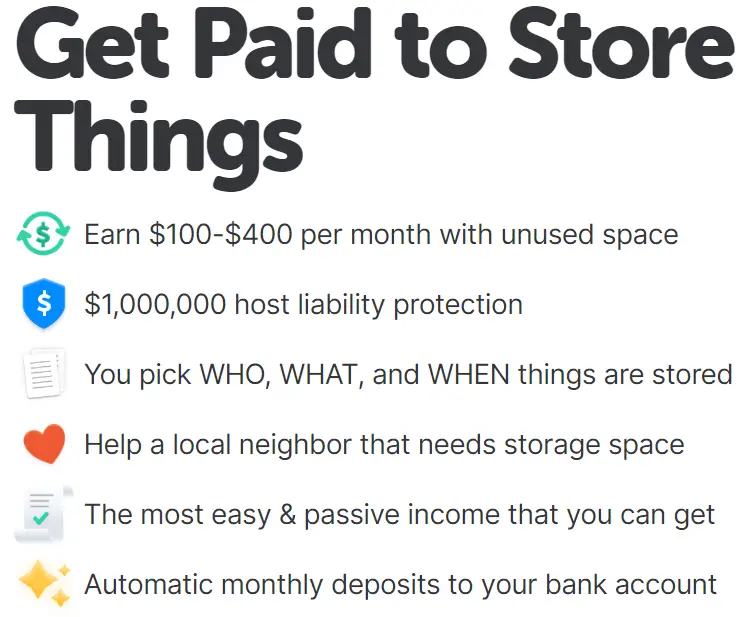

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

Buying An Existing Home: Pros and Cons

The main advantage of buying an existing home is knowing exactly what you’re getting.

There won’t be any surprises in terms of the property’s condition or the construction’s quality.

Another benefit is that you’ll be able to move in right away. If you’re building a new home, it can take months or even years to complete the construction process.

However, there are also some disadvantages to buying an existing home. One is that you may have to make repairs or renovations.

This can be expensive and time-consuming. Additionally, existing homes may not have all the features and amenities you want or need.

Building A New Home: Pros and Cons

One main advantage of building a new home is that you can customize it to your needs and wants.

You’ll be able to decide on the layout, the number of rooms, and all the features and finishes.

Another benefit is that you won’t have to worry about making repairs or renovations.

Everything will be brand new, so you shouldn’t have any issues for many years.

However, there are also some disadvantages to building a new home. One is that completing the construction process can take a long time.

Additionally, hiring professionals to help with the design and construction can be expensive.

In Summary

Making the decision to buy a new or existing home depends on your specific circumstances and what’s important to you.

The building may be the best option if you’re hunting for a house completely custom to your needs.

However, if you’re looking for a move-in ready home that won’t require any repairs or renovations, then buying an existing home may be the better choice.

Consider all of your options and make the decision that is best for you. There’s no right or wrong answer when buying or building a house. It all comes down to personal preference.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Do you ever wonder how long it would take for your invested money to double?

If so, you are not alone.

There is a whole field of study devoted to answering this question, called financial mathematics.

And one of the most popular methods for estimating doubling time is the Rule of 72.

In this blog post, we will discuss the rule of 72, how to use it, and how accurate it is. We will also show you how to apply this rule to your investment planning so that you can make smart decisions about your money!

What Is the Rule of 72?

The rule is a simple formula that can help you estimate how long it will take for an investment to double in value. The rule is based on the idea that investments grow at a compound interest rate. It shows how many years it will take for an investment to double if it grows at a given compound interest rate.

Think of it as a financial tool to help you understand the power of compounding!

The rule of 72 was developed by a 19th-century Italian mathematician named Leonardo Pisano, also known as Fibonacci.

It can be used for any investment, including stocks, bonds, and savings accounts.

You can use this rule to estimate the doubling time if you know the compound interest rate.

The Formula for the Rule of 72

The rule of 72 formula is as follows:

72 / Compound Annual Growth Rate = the number of years until your money doubles.

For example, if you are earning a 12% compound annual return on your investment, it would take approximately 72/12 = 6 years for your money to double.

A great way to use the formula is to estimate how long it will take for an investment to double.

The rule cannot be used to estimate other financial goals, such as how much money you will have after a certain number of years.

It is also important to know that the rule of 72 only applies to investments that compound interest regularly.

The rule of 72 is not an exact science. It’s a general guideline that can help you estimate how long it will take for your money to grow.

The math is accurate, but often investments won’t have a fixed interest rate.

In addition, the rule of 72 doesn’t take into account any fees or taxes that may be associated with your investment.

So, the rule of 72 can give you a general idea of how long it will take for your money to grow.

Talk to a financial advisor to get a more specific estimate when it comes to your own investments.

In general, the rule of 72 is accurate, but you must consider other factors that may affect your situation.

When using the rule of 72 for your investment planning, it’s important to be mindful of these variables.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

How to Use the Rule of 72 for Your Investment Planning

Now that you know the rule of 72 and how it works, you can start using it to help make investment decisions.

For example, let’s say you are considering investing in a stock with a history of growing at a rate of 20% per year.

Using the rule of 72, we can estimate that it would take approximately 72/20 = roughly 3.6 years for your investment to double in value.

This can be a beneficial way to compare different investments and decide which one is right for you.

You can also use the rule of 72 to see how much your investment would compound and double over and over again.

Imagine you had a $1000 investment that doubled every four years. That would be an 18% interest rate (72/16 = 4).

After only 12 years, you would have $8000.

Now, let’s explore the wonders of compound interest and stretch the timeline to 24 years.

After 24 years, assuming a consistent 18% interest rate minus fees and other expenses, you would have $64,000.

As you can see, with just $1000 and a little time, the rule of 72 can have your money working hard for you.

You would have made $63,000 in profit for no extra work. Consistent contributions and a larger initial investment can increase this.

Let’s say you have just $5000 instead of $1000; here is what the rule of 72 shows us:

After only 12 years, you would have $40,000. In 24 years, your investment of $5000 would grow to $320,000.

With the rule of 72, you can get a quick estimate of how your investment will grow over time. This can be helpful when you’re trying to decide how to invest your money.

The rule of 72 can Estimate How to Pay Off Debt

For example, let’s say you have a credit card with a balance of $1000 and an interest rate of 18%.

If you missed your four-year payments your debt would double to $2000 (72/18 = 4). After another four years, you would owe an additional $2000 with a total of $4000 in debt.

The rule of 42 can be used to see how quickly debt can compound out of control.

It’s a clear mathematical model that depicts the potential scenario if you don’t take action to get your debt under control.

This rule can help you plan and budget for your debt repayment. It also shows how compounding can also work against you if you’re not careful.

The rule of 72 can be a helpful tool when you’re trying to make financial decisions.

It’s important to remember that the rule is just an estimate and other factors can affect your specific situation.

Always speak to a financial advisor to get the most accurate information for your circumstances when in doubt.

In Summary

In conclusion, the rule of 72 is a helpful tool that can estimate how long your money will take to grow.

However, the rule of 42 only works if you have a fixed interest rate and doesn’t consider any fees or taxes.

The rule can be used to predict both investment growth and debt repayment.

When using the rule of 72, it’s important to remember that it’s just an estimate and other factors can affect your specific situation.

Always speak to a financial advisor to get the most accurate information for your circumstances when in doubt.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

If you are new to the world of cryptocurrency, you may have heard the term NFT before.

But what does it even mean?

And more importantly, should you consider investing in them?

In this blog post, we will explain everything you need to know about NFTs – from what they are, to how to invest in them.

We’ll also discuss the pros and cons of investing in this new type of asset so that you can make an informed decision about whether or not it’s right for you.

YouTube Video I Made Covering NFTs

What is an NFT?

NFTs, or non-fungible tokens, are digital assets that are unique and cannot be replaced. They’re like virtual collectibles you can buy, sell or trade like any other asset. NFTs are on a blockchain, a decentralized ledger that records all transactions.

NFTs have been gaining in popularity lately due to the rise of cryptocurrencies and the growing interest in digital art and gaming.

For example, the popular game CryptoKitties allows players to buy, sell, or trade virtual cats that are each represented by an NFT.

Similarly, the online art platform SuperRare allows artists to sell their digital artwork as NFTs.

So why are NFTs so popular?

One reason is that they’re scarce and thus have the potential to be quite valuable.

Another reason that NFTs are interesting is because of the utility value that can be attached to them.

For example, you could use an NFT to represent a ticket to a concert or a virtual world.

Some people believe that NFTs will revolutionize the way we interact with the digital world.

Many traditional industries may also start adopting NFTs.

The real estate industry could start using NFTs to represent ownership of property.

NFTs are still in their early days and it’s hard to say where they will go from here.

But one thing is for sure: they’re providing a new way for people to interact with and invest in digital assets.

So if you want to learn about the world of NFTs, be sure to do your research and understand the risks before investing.

NFTs, or non-fungible tokens, use the same blockchain technology but are not technically classified as cryptocurrency.

They are non-fungible, meaning they are unique and cannot be replaced by another token.

On the other hand, cryptocurrencies such as Bitcoin and Ethereum fall within the same token category.

NFTs are can represent digital assets, such as art, music, or videos. While cryptocurrencies are tokens that help blockchains run.

With these, you can purchase goods and services, or trade for other assets.

NFTs are not the same as cryptocurrencies, but they are similar.

You can decide to buy, sell, or trade both NFTs and cryptocurrencies which are digital assets.

And both NFTs and cryptocurrencies are stored on a blockchain.

All cryptocurrencies must be identical for them to be convertible.

NFTs benefit from their unique qualities. This is because NFTs can represent assets that are one-of-a-kind, like a piece of digital art or limited edition access to utility functions.

Unlike Bitcoin or Ethereum, which can be divided into smaller units, NFTs cannot be divided or exchanged for other assets.

This divisibility is one of the reasons why Bitcoin and Ethereum have value. NFTs, on the other hand, have what is called “intrinsic value.”

Intrinsic value is the value that an asset has because of its usefulness or rarity.

How To Invest in NFTs?

If you’re interested in investing in NFTs, there are a few things you need to know.

First, it’s important to understand that NFTs are still a new and emerging asset class.

As such, they come with a higher degree of risk than more traditional investments.

Before investing in NFTs, be sure to do your research and understand the risks involved.

You should also have a clear investment strategy and know what you want from your investment.

General tips for investing in NFTs:

Start small: When investing in any new asset class, it’s always best to start small and gradually increase your exposure as you become more comfortable with the asset and the market.

Diversify your portfolio: Don’t put all your eggs in one basket.

When investing in NFTs, be sure to diversify your portfolio across several different assets and platforms.

Do your research: Like any investment, it’s important to do your research and understand the risks involved before investing.

Read up on the history of NFTs and the projects you want to invest in.

With these tips in mind, you should be well on your way to making smart and informed investments in NFTs.

Steps to investing in an NFT

Find a reputable NFT marketplace: There are several different NFT marketplaces where you can buy, sell, or trade NFTs.

Some of the more popular ones include OpenSea, Rarible, and SuperRare.

Create a web 3.0 wallet: To store and manage your NFTs, you’ll need a web-based wallet that supports the ERC-20 token standard.

Some popular options include MetaMask, Trust Wallet, and Coinbase Wallet.

If you are buying from another blockchain, you would need to use their native web 3.0 wallet.

Deposit funds into your wallet: Once you have your wallet set up, you’ll need to deposit funds into it so you can start buying NFTs.

The easiest way to do this is by purchasing Ethereum (ETH) with a credit or debit card on a site like Coinbase.

If you buy from another blockchain, you’ll need to purchase their native currency.

Choose the right asset: When investing in NFTs, it’s important to choose the right asset.

Make sure you select an asset you’re comfortable with that aligns with your investment goals.

Complete the transaction: Once you’ve found the right asset, the next step is to complete the transaction.

You can do this using a cryptocurrency exchange or NFT marketplace.

Be sure to carefully review the terms and conditions of the transaction before completing it.

How To Sell An NFT?

If you are ready to sell an NFT, you will need to take the following steps:

Decide where you want to sell: You can sell your NFT on popular platforms such as OpenSea, Rarible, and SuperRare.

You would want to ensure the marketplace supports the type of NFT you own.

Price your NFT: When setting a price for your NFT, consider the following factors: the rarity of the asset, the demand for the asset, and the current market conditions.

Create a listing: Once you’ve decided on a price, the next step is to create a listing for your NFT. You can do this in the marketplace of your choice.

Be sure to include clear and concise descriptions of the asset and any pertinent information potential buyers might need.

Wait for a purchase or promote your listing: The final step is to wait for a buyer to purchase your NFT or promote your listing to attract more buyers.

Once a buyer has been found, the transaction will be completed and the NFT will be transferred to the buyer’s wallet.

Pros And Cons of Investing in NFTs

The benefits of investing in NFTs include the following:

You cannot replicate NFTs, which makes them a scarce asset.

They are stored on a blockchain, which makes them immutable and secure.

You can buy, sell, or trade NFTs 24/7 on several marketplaces.

They can unlock networking and collaboration opportunities with other NFT owners.

You may obtain a distribution or intellectual property rights if it is written in the NFT’s smart contract.

However, there are also some drawbacks to investing in NFTs.

First of all, they’re still a relatively new technology and there’s no guarantee that their value will continue to increase.

Additionally, since NFTs are on a blockchain, they can be quite difficult to sell or trade due to the high transaction fees associated with blockchain transactions.

Finally, it’s important to remember that NFTs are still subject to the cryptocurrency market’s volatility.

Should I Buy an NFT?

There is no easy answer to this question. It depends on several factors, including your investment goals, risk tolerance, and the current market conditions.

If you support an artist or creator, find benefit in networking with a community, enjoy the utility, and/or can clearly articulate the appreciation potential, then buying an NFT might be a good idea for you.

However, if you’re not comfortable with the risks of investing in NFT and only want to invest to join the hype, then you might want to reconsider.

If you’re considering buying an NFT, be sure to do your research and consult a financial advisor to ensure that it’s the right decision for you.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

When it comes to investing, many different options are available to you! You can invest in stocks, bonds, real estate, and other assets. However, many people don’t know about the available types of funds. This article will compare mutual funds, ETFs, and index funds.

This post may contain affiliate links; please see our disclaimer for details.

Difference between Mutual Funds, ETFs, and Index funds

Let’s discuss the similarities and differences so that you can have a better idea of how to start investing!

You can also check out my YouTube video explaining Mutual Funds, ETFs, and Index Funds.

My YouTube video explaining Mutual Funds, ETFs, and Index Funds

What are Mutual Funds?

Mutual Funds

A mutual fund is an investment vehicle that consists of a pool of funds. The funds are from many investors who invest in securities such as stocks, bonds, or other assets. Professional money managers help manage mutual funds.

They aim to allocate the fund’s assets and attempt to produce capital gains or income for the fund investors.

Thus, you will need a brokerage account or 401(k) investing account to start investing since you cannot trade them on the open stock market.

These money managers receive a management fee, typically a percentage of the fund’s assets.

Mutual Funds – Advantages & Differences

The main advantage of mutual funds is that they provide small investors access to professionally managed portfolios of securities that would otherwise be unavailable to them.

This can be helpful if you don’t have the time or expertise to manage your investments.

Another advantage is that mutual funds are relatively easy to buy and sell and offer liquidity, meaning that you can cash out your investment at any time without having to sell the underlying securities.

A key difference between mutual funds, ETFs, and Index funds is that they can be bought or traded once the market closes for the day instead of during open market or extended market hours.

Mutual funds come with several risks, however. One is that the fund’s performance depends on the fund manager’s skill, and even the best managers can have a bad year.

Another risk is that mutual funds are subject to market risk, meaning their value will go up and down with the stock market.

Mutual fund managers will work to reduce these risks by diversifying the fund’s holdings.

Before investing in a mutual fund, research the fund’s objectives, fees, and track record.

You should also consider your own investment goals and risk tolerance.

What Is an ETF (Exchange-Traded Fund)?

An ETF is an investment vehicle that consists of a basket of assets, such as stocks, bonds, or commodities.

You can buy and sell ETFs like regular stocks and trade them on stock exchanges.

One advantage of ETFs is that they offer investors exposure to a broad range of asset classes in a single investment.

For example, an ETF that tracks the S&P 500 Index provides exposure to 500 large-cap U.S. stocks. This is beneficial because it allows investors to diversify their portfolios without purchasing individual stocks.

Market investors enjoy ETFs due to their low costs, tax efficiency, and flexibility.

Their popularity has exploded in recent years, with more and more people wanting to manage their investments themselves.

However, ETFs also come with some risks.

For example, because ETFs are traded on stock exchanges, their prices can be subject to market fluctuations.

Additionally, some ETFs are more volatile than others. It’s important to research and understand the risks before investing in an ETF.

If you’re considering adding ETFs to your investment portfolio, it’s important to understand how they work and the risks involved.

With a little research, you can make an informed decision about whether or not ETFs are right for you.

What are Index Funds?

Index funds are investment funds that track a specific market index, such as the S&P 500.

These funds are passively managed, which means they aim to track the performance of the underlying index.

Index funds typically have lower fees than actively managed mutual funds, which can be a good choice for investors who want to invest in a broad market index.

You can buy or sell like other types of investment funds and hold them in taxable and tax-advantaged accounts.

When you buy an index fund, you buy shares in the fund itself, not in the underlying assets (such as stocks or bonds) that make up the index.

The value of your investment in an index fund will rise and fall with the value of the underlying index.

You may want Index funds as part of a broader investment strategy, such as asset allocation or dollar-cost averaging.

When used this way, index funds can help you diversify your portfolio and manage risk.

Comparing the similarities and differences.

If you want to invest in an entire sector, index funds may be the way to go.

For example, if you want to invest in the U.S. stock market, you could buy an index fund that tracks the S&P 500. This would expose you to 500 large-cap U.S. stocks without purchasing individual stocks.

ETFs also share this feature as they can track an index or sector.

For example, Ark ETFs tracks innovative industries such as automation, genomics, and artificial intelligence.

Both ETFs and index funds have the added benefit of being traded on stock exchanges.

So investors do not have to go to a financial advisor or banker like mutual funds.

However, ETFs may be more volatile than index funds because they are traded like stocks.

Additionally, some ETFs are more volatile than others. It’s important to research and understand the risks before investing in an ETF.

Positions within an ETF are traded throughout the day as the market fluctuates, which can result in investors seeing large changes in their investments.

Index funds are passively managed, which means they aim to track the performance of the underlying index.

ETFs, on the other hand, are actively managed. This means that a team of professionals constantly decides which stocks to buy and sell to outperform the market.

Because of this, ETFs typically have higher fees than index funds.

Regarding risk, ETFs, index funds, and mutual funds can potentially lose money if the underlying asset declines in value.

However, with a mutual fund, you may not panic and sell as your advisor will decide when to buy and sell.

With an ETF or index fund, you may be more tempted to sell if the market starts to decline, which could lead to losses.

The main difference between ETFs and mutual funds is that money managers do not actively manage ETFs.

Instead, they track a specific index, such as the S&P 500.

This means that ETFs have lower management fees than mutual funds. Thus, there is no need to pay a professional money manager to manage the fund.

In conclusion, the similarities of all three are that they allow investors to gain exposure to the stock market in a diversified way.

They differ in the amount of control and fees an investor incurs.

Mutual Funds vs. ETFs vs. Index Funds: Which One Is Better?

A strong advantage of ETFs is that they offer greater transparency than mutual funds because you know exactly what the fund owns at all times.

ETFs are more tax-advantaged than mutual funds, one of their many advantages. This is because ETFs are not subject to the same tax rules as mutual funds.

For example, when a mutual fund realizes a capital gain, it must distribute the gain to its shareholders, who are then subject to capital gains taxes.

On the other hand, ETFs do not require the distribution of gains to shareholders. This can make them more attractive to investors looking to minimize their tax liability.

Another advantage of ETFs is that they tend to be more cost-effective than traditional mutual funds.

Mutual fund fees can eat into your investment returns, but ETFs typically have lower fees because you do not need to manage them actively.

For example, the expense ratio for the Vanguard S&P 500 ETF is just 0.03%, while the expense ratio for the Fidelity 500 Index Fund is 0.09%.

A mutual funds management fee can be up to several percent. This may not seem like a big difference, but the lower fees can add to significant savings over time.

In Summary

To sum it up, it depends on what you are looking for as an investor. If you are hands-on and want the lowest cost, then an index fund is probably the best choice.

A mutual fund is a better choice if you are looking for more professional management and are willing to pay a higher fee. And if you are looking for something in between, then an ETF might be the right investment.

Self-awareness is key when it comes to investing.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

Consider your risk tolerance, investment goals, and time horizon when making any decisions.

Remember, there is no one-size-fits-all answer when it comes to investing.

The most important thing is that you invest in something you are comfortable with that aligns with your financial goals.

Do your own research and consult a financial advisor to determine which type of investment is right for you.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

A house can be an asset or liability.

There’s no question that a house can be a valuable asset, but only under certain circumstances.

Per data collected from Trading Economics, the rate of household owners in the united states is currently 65.4%.

But, not all homeowners’ homes are assets.

But is it always an asset? This is a question many of us will ask ourselves at some point.

According to Rich Dad Poor Dad, the answer is no. In his book, Robert T. Kiyosaki taught that a house could be either an asset or a liability, depending on your perspective.

Let’s look at what he means by this and how you can apply it to your own life!

Before we go into depth on whether a house is an asset or a liability, let’s first understand the difference between the two.

In the simplest of terms, an asset puts money in your pocket. A liability is something that takes money out of your pocket!

For example, a rental property would be considered an asset because it generates income (through rent) which goes into your pocket.

On the other hand, a primary residence would be considered a liability because it costs money (in the form of mortgage payments, insurance, taxes, etc.) to maintain and keep up.

That said, let’s dive into whether a house is always an asset or can sometimes be a liability…

When is a House an Asset?

There are situations when a house can be an asset.

Let me illustrate this with a couple of examples…

If you’re a landlord and rent out your properties, the houses would be considered assets because they generate income.

You’re in a situation where a house can be an asset if you live in a paid-off home and have the extra cash flow to invest in things like renovations or improvements.

When is a House a Liability?

There are also situations when a house can be more of a liability than an asset.

Typically this is the case when someone has a mortgage or is otherwise upside down on their home.

Meaning you owe more than you own!

In these situations, it cannot be easy to make ends meet. The house then becomes more of a burden than anything else.

Another situation where a house might be considered a liability is if the market crashes and home values plummet.

When this happens, it leaves homeowners in a very difficult position.

Especially if they need to sell but can’t get out from under their mortgage.

Asset Accumulation Mindset

If you view your house as an asset, you will likely treat it as such.

This means you’ll invest in it, keep it well-maintained, and improve its value!

As a result, your house will appreciate over time and provide you with a solid return on investment.

You will also make sure that it provides passive income each month. Think about renting it out or generating income in some other way.

In this case, your house works for you and puts money back into your pocket each month.

Get on the right track to financial success by understanding the importance of accumulating assets or turning things from liabilities into assets.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

On the flip side, if you view your house as a liability, you’re likelier to let it fall into disrepair.

You probably won’t invest much money in maintaining or improving it, and as a result, its value will decline.

The house will be a liability because the mortgage payments and general cash flow will be negative.

You will also have difficulty achieving financial freedom because you’ll be stuck in this never-ending cycle of debt.

People will often buy houses with mortgages they can’t afford to pay off out of their own earned income. This is a recipe for disaster and will likely lead to financial ruin.

It’s important to remember that a house is just a tool.

A tool that can be used to achieve financial freedom, or it can be a ball and chain that keeps you in debt for the rest of your life.

The choice is up to you!

Changing a Liability into an Asset

Here is a story example of how the Rish family turned their house which was originally a liability, into an asset:

After Mr. Rish read the book ‘ Rich Dad Poor Dad’, he and his wife had a change of mindset.

They realized that the house they had been living in for years was a liability instead of an asset.

They decided to make some changes and turned their house into an asset!

First, they renovated their basement and began charging rent.

Second, they used that money to pay off their mortgage so that they no longer had monthly payments – pretty awesome right?

Third, when their children moved out, they decided to move to a small apartment but keep their original home for renters.

There were two vacant rooms on the main floors and bedrooms in their home, allowing them to be rented out.

They charged another family to live there and collected additional rent money to cover more than their new living expenses at their small apartment.

The house provides income each month through the tenant’s rent and puts money into the couple’s pockets as they live happily ever after.

By making these changes, they could increase the value of their house and create a passive income stream.

As a result, they achieved financial freedom and could retire early.

This is just one example of how changing your mindset about your house can lead to financial success.

If you’re stuck in the mindset that a house is always an asset, but it’s costing you money each month, it’s time to make a change!

Start by looking at your situation and see how you can turn your house from a liability into an asset.

It may take some work, but it’s possible to achieve financial freedom by doing so.

Conclusion

As you can see, there is no clear-cut answer as to whether a house is always an asset or a liability.

It is an asset if it is putting money into your pocket each month and increasing in value.

However, if it costs you money each month and not increasing in value, then it is a liability.

Make sure to carefully consider your situation before making any decisions about your house!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.