My Wife and I hit Coast FIRE number which is close to $500,000 this year, allowing us to quit our 9-5 jobs, move abroad to China, and more fully pursue our passions in life at age 26.

You may be asking yourself, what is this Coast FIRE term exactly?

In a nutshell, Coast FIRE is a popular retirement strategy involving saving enough money so your nest egg can grow without additional contributions. Once you reach Coast FIRE, you no longer need to work to save for retirement; instead, you only work to pay for current living expenses. This allows you to enjoy a more relaxed lifestyle and focus on activities you enjoy rather than working simply to earn a paycheck.

Before breaking down our $500,000 net worth, I want to share some interesting statistics.

The average net worth by age for Americans

Let’s see the average net worth by age for Americans according to CNBC.

For those under age 35, the average net worth of Americans is $76,300.

For those ages 35 to 44, the average net worth of Americans is $436,200.

For those ages 45 to 54, the average net worth of Americans is $833,200.

For those ages 55 to 64, the average net worth of Americans is $1,175,900.

For those ages 55 to 64, the average net worth of Americans is $1,217,700.

For those ages 75 and above, the average net worth of Americans is $977,600.

Our Net Worth Breakdown

Now let’s take a closer look at our net worth broken down into 7 categories.

1) US Checking Accounts: $5000

Not much to add here, we have about $5,000 cash sitting in our checking accounts in the US.

2) China Bank Accounts: $3100

We currently have around 20,000 CNY which is $3100 in our China bank account. If you wonder how much it costs to live in China, you can check our other blog post – Cost to Semi-Retire in China (Our First Month Expenses).

3) High Yield Saving Account: $21,000

We have one high-yield saving account, which acts as our emergency fund.

Having an emergency fund gives us peace of mind. For example, we have rental properties in the US and if something happened, we have money to fix it.

Actually, we have $40,000 total because of the Biden student loan refund. We put it there to receive higher interest payments. Once we know if the forgiveness part will pass or not we know how to use this money. We don’t account this as our net worth since we don’t know the final results yet.

4) Retirement/Tax-Advantaged Accounts: $100,000

These include all of our Roth IRAs, HSA, Rollover IRAs, etc. Even though after hitting Coast FIRE you can choose to stop investing, we still want to max our IRAs if possible so our nest egg can grow even larger.

5) Brokerage Accounts: $2,300

In Robinhood, we did some higher risk investing like crypto, but only a very small bit compared to the rest of our net worth. As you know recently the market has not been very good so the value dropped a lot!

6) Single house rental Property: $200,000

We built a single-family house and finished the basement and yard after we moved in. In total, it is 0.12 ace with 2300 sqft. 4 bedrooms and 3.5 baths.

When we move to China, we decided to rent it out.

The total home value now minus the loan we have is about $200,000, which is our equity.

7) Condo Rental Property: $150,000

We have another rental property which is a cozy 3 bedroom/2 bath condo.

We checked condos in the same community and can say we have at least $150,000 house equity in it.

Side note: when calculating net worth for home loans you take the current market value minus what you owe on the loan.

TOTAL: $481,400

“When you invest, you are buying a day that you don’t have to work.”

Aya Laraya

Thank you for reading! Please drop a question or comment below – we’d love to hear your thoughts.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

My wife and I contacted our student loan provider shortly after the Biden Student Debt Relief Program was first announced last year.

We received a refund from our loan provider but have been waiting to see if the forgiveness portion will eventually get passed, or not. Regardless, the refund was just sitting in my bank account and not being very productive there, so I had to make a decision, I’ll jump into more on that later.

The most current update is that the student debt relief plan is still blocked, and if it’s not resolved by June 30, 2023, the loan repayment freeze will end and payments will continue 60 days after that.

In this article, I will share our process for applying for a refund/loan forgiveness and how it actually turned out to be a great investment opportunity for us.

This post may contain affiliate links; please see our disclaimer for details.

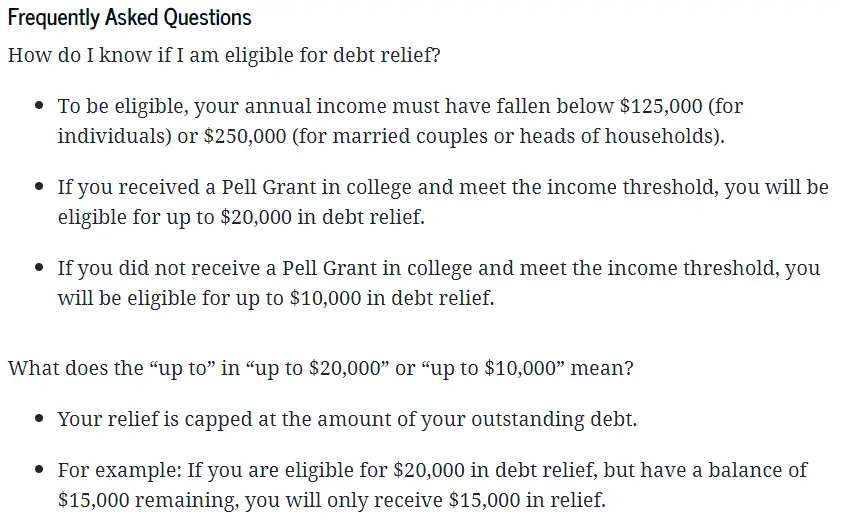

Biden Student Debt Relief Program Details

Those with federal student loan balances on or before June 30, 2022 could potentially receive a refund of up to $20,000. Loans dispersed after July 1, 2022 don’t qualify and private loans do not qualify.

Here are some more eligibility details from studentaid.gov:

Credit: Studentaid.gov

The good news is that since I had paid off my loans during the pandemic (I made payments since March 2020), I was eligible for a refund! Next, I’ll share my exact application process for the refund and forgiveness parts.

Our Application Experience

My student loans were housed with Navient but then moved to a company called Aidvantage. Upon hearing the debt relief announcement, I called Aidvantage to see if I was eligible for a refund.

It was pretty funny because they did not have a formal process yet but took down my request and put me on a list. After calling back and waiting a bit longer, I eventually received a refund for a little over $20,000 since I previously had pell grants.

So I want to add an important note that I only received the refund, NOT the forgiveness. So technically, the $20,000 is still owed as of right now, but the good news is that I don’t have any payments due and zero interest charges.

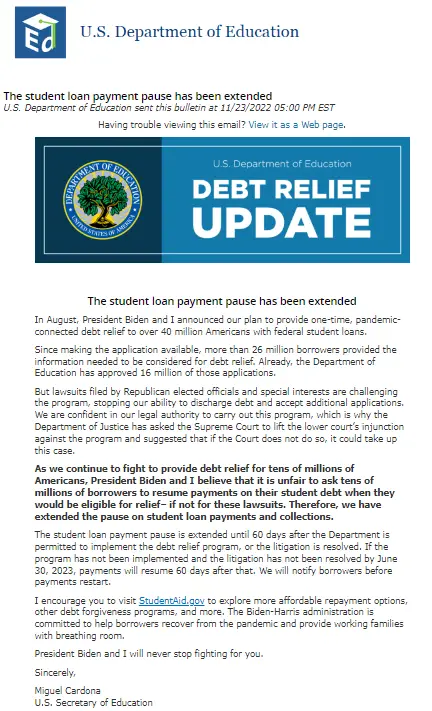

I submitted my application for the forgiveness portion of the Biden student debt relief program on studentaid.gov, but as mentioned before, it has been blocked, and they are not accepting any more applications at this time.

Here is a copy of the email I received saying I was approved for loan forgiveness, but the pause had been extended.

Why is it an Investing Opportunity

With the debt relief plan continually getting blocked, my wife and I realized it probably wasn’t the best option to have that refund sitting in our regular bank account.

That would increase our high-yield savings balance to about $40,000 and give us about $120 in MONTHLY in interest payments! This is because our high-yield savings account is with CITI bank with an interest rate of over 3%!

Although it may not seem like a lot, those interest payments can really add up, and we could have well over $700 by the time the refund amount is forgiven from our loan provider or we have to pay back the $20,000, but keep the interest.

Why a high-yield savings account?

First: a high-yield savings account is a type of savings account that offers a higher interest rate than a traditional savings account. This can really add up over time.

Second: you can access the money immediately. Let’s say Biden’s loan forgiveness doesn’t go through, I’d still be able to quickly pull out the funds and pay off the debt. It would take longer to pull the money out of a 401k or other investment account, not to mention it would be riskier in those types of investment accounts.

When choosing a high-yield savings account, it is important to compare the features and fees of each option to find the best fit for your needs.

You can find high-yield savings accounts at both online and brick-and-mortar banks.

Many online banks offer higher interest rates than traditional banks, so it is worth considering an online option if you are looking for the best return on your investment. For more, you can visit this article I wrote sharing High Yield Savings Accounts – Should you have one?

A great place to get started with your savings account isCIT Bank. They offer very competitive saving rates with no monthly maintenance fees.

With their Saving Connect Account, you can earn 12x the national average! There are no ATM fees, and you have the convenience of online banking.

If you find yourself in the same boat where you have a refund sitting in your bank account, it may be a good idea to get it moved over to a high-yield savings account. Overall it is considered very safe.

I would definitely NOT recommend putting your refund into the stock market or somewhere with higher risk and volatility. Sorry crypto, maybe next time.

The same principle goes for any extra money you have lying around. Instead of keeping it a low-interest, regular savings account, move it on over to a high-yield savings account.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Many people want to get started investing but aren’t sure what strategy to use. Others aren’t sure if it’s possible at a young age or with a lower income. Don’t worry; that’s why I wrote this article to help give you insights into our Real Estate strategy.

Real Estate investments can be a powerful tool to help you achieve financial freedom, and it doesn’t have to be hard or complicated. My Wife and I love real estate and started our investing journey as young college students in Utah.

When we purchased our first property, we were just college students, ages 21 and 23!

We did not have a lot of money. We did not have high-paying jobs.

Through hard work, we saved up $20,000 and kickstarted our real estate journey. Now that $20,000 has become $400,000 after five years!

Since we did not have a lot of income, we couldn’t follow the BRRRR strategy strictly.

More on that to come…

This post may contain affiliate links; please see our disclaimer for details.

Video Sharing Our Real Estate Strategy

Our Real Estate Numbers and Timeline

First Real Estate Property

Our first property turned out to be a nice townhome located in Utah. It was built in 1970 and had two bedrooms plus 1.5 baths.

The total price was $100,000 in 2017. My sweetheart was 21 years old, and I was 23.

In total, we saved up $20,000 for our down payment. Since the downpayment was 20% of the house price, we did not have to pay mortgage insurance!

Our monthly mortgage payment was around $850 with HOA, taxes, etc.

We lived there for over a year and then rented it out for almost two years.

The rental income was $1000 a month, giving us $250 extra cash flow each month!

In 2020 we ended up selling the property for $140,000.

Second Real Estate Property

We bought our second property (a condo) in 2018 when My wife was 22 and I was 24.

It was after accepting a job offer as an account manager that we decided to upgrade our home and rent out the first property, becoming first-time landlords.

The condo we found had 3 bedrooms/2 baths and was built-in in 2002.

As our second property, we could only apply for a conventional loan with a minimum requirement of 5%.

We also had to pay PMI (mortgage insurance) since the down payment did not reach 20% of the loan’s total amount.

The total price of the condo was $171,000. Our down payment + closing costs were $10,000 in total.

The monthly payment with HOA and mortgage insurance included was just about $1,200. When COVID-19 happened, the interest rates dropped significantly.

We noticed these great interest rates and decided to refinance this condo!

After refinancing, our monthly payment went down to around $1,000 (Mortage, HOA, etc.), saving us $200 a month!

After living in the condo for around two years, we rented it out. We are still renting this condo, and the rental price is $1330 now, which gave us around $330 a month in cash flow!

Recently, the same condo sold in our community is around $300,000. When we bought it, it was only $170,000.

Third Real Estate Property

Our new home was under construction in July 2020. The building process was exciting and took ten months to finish.

We officially closed on the house / third property in May 2021 when my wife was 24 and I was 26.

The total price of our new single-family home was just around $340,000. The home’s square footage is 2,300, with a lot size of 0.12 acres. We put down a 5% down payment which cost us $20,000.

Our locked interest rate is 3%. In total, our mortgage payment each month is $1,530. After we moved in, we finished both our yard and basement.

The cost of finishing both our yard and basement will be approximately $20,000. A lot we did by ourselves, but some parts were hired out.

Recently the exact same model that sold in our community is $500,000 without a furnished yard and basement. Yet, when we bought it, it was only $340,000.

Since we hit Coast FIRE and moved abroad, this third property is now rented out, providing us with positive cash flows. We rent it out for $2,200 a month. Our total monthly expense, including mortgage payments, HOA, etc., is $1,600. This gives us a monthly cash flow of $600.

Now let’s talk about what BRRRR is first, and then we will share our real estate investing strategy.

So you can compare both of their similarities and differences so that you can decide which one is right for you!

“If you can, you should, and if you’re brave enough to start, you will.”

Stephen King

What Is The BRRRR Method?

The BRRRR method is a strategy for real estate investing that stands for “buy, rehab, rent, refinance, repeat “.

This methodology can be used in both residential and commercial real estate investing.

Buy: The first step is to find an investment property you want to purchase in a good location.

Once you have found a property, you will need to put down a deposit and then close on the deal.

Rehab: After you have purchased the property, you will need to renovate or repair it so that it is in good condition and value is added.

Once the repairs are complete, you can start renting the property to tenants.

Rent: After the property has been rented out for some time, you can refinance the property loan.

Refinance: You can conduct a cash-out refinance where you take out cash for the equity in your property and use it to purchase your next one.

Repeat: Once you have refinanced the property, you can then repeat the process by finding another property to purchase and rehab.

Our Real Estate Investment Strategy

Here is a quick overview of our strategy:

Buy as owner-occupied (residential property).

Do some easy remodeling while living there.

Save up a downpayment for the next property.

Buy the next house and rent out the previous one.

Repeat the process.

Let’s go over each step of this strategy so that you can understand how it works and decide if it is right for you!

1) Buy as Owner-Occupied (Residential Property)

Once you have saved enough for a down payment, you will purchase your house as owner-occupied/residential property.

If you buy an owner-occupied/residential property, you can obtain a better interest rate, saving you a lot of money in the long run!

This is a crucial tip – When we look for a house, we always research how much we could rent out a property for and whether it can provide positive cash flows after mortgage payments and other expenses.

When we bought our first owner-occupied/residential property, our lender required us to live there for at least one year before converting it to a rental property.

Different lenders might have different rules, so it is good to check your lender.

During the time we lived in the property, we had time to remodel and start saving a down payment for the next home.

Remember to ONLY buy the house you can afford, NOT your dream home. Then, when you have a better financial situation, you can always upgrade to a better house next time!

My wife and I always told ourselves this is NOT our forever home; it doesn’t need to be perfect. It will be our rental one day, and we will work hard for our next one.

This has been an excellent motivation for us and reminds us to live within our means.

2) Do Some Easy Remodeling While Living There

As mentioned before, our lender required us to live there for at least one year before we could convert it to a rental property.

We were college students back then and didn’t have a lot of money. There was no way we could afford to buy rental property directly like some people, or spend a lot of money to hire professional contractors for remodeling.

Our first and second homes are second-hand houses, but our 3rd property was a brand new house we built. The nice thing about that third home is there was no remodeling needed so we did some house improvements such as finishing the yard and basement.

So we did some simple remodeling when living in our first and second properties, like painting doors, kitchen cabinets, and switched some old appliances, etc.

To make the place look nicer when we rent. Cleaning and painting are the BEST, EASIEST and CHEAPEST ways to remodel your house and make it look 100 times better.

Another note is that the seller must have owned the home and used it as their principal residence for two out of the last five years (up to the closing date).

This means if you lived in the house for two years, you can sell it with ZERO CAPITAL GAINS TAX within three years. If you have the plan to sell, it’s a good idea to stay there for at least two years!

3) Save up a Downpayment for the Next Property

If you know your goal is to purchase another home, you should start saving your next house down payment ASAP.

Once you have a better-paying job or are ready to upgrade your home, you will have the money ready.

It would help if you had an idea of how much your next house would cost so you can know how much of a down payment to save.

This part is different than BRRRR because we typically don’t refinance our properties and pull money out to buy the next property. We 100% save up the down payment by ourselves because we felt it was a better option with less risk for our family.

4) Buy the Next House and Rent out the Previous One

This step is very exciting! Once you are ready to buy a new place, it’s time to rent the one you live in.

Usually, you need to rent it out and provide the rental agreement and security deposit to your lender to close your new house.

Also, check with your HOA and city to see if other landlord licenses or documents are required. Our first property HOA required a copy of our city’s landlord license certificate but our second property HOA did not.

5) Repeat the Same Process

This step doesn’t need a whole lot of explanation, haha. Just re-start the steps and you’ll find it’s a very easy and enjoyable process!

Keep the process going and know you can reach your goals in time, and eventually get into your dream home!

Some tips for this step: Repeat

Keep track of your finances.

Diversify your portfolio.

Stay disciplined and learn from past mistakes.

Our real estate strategy can be a great way to succeed in investing and help lower risks associated with typical investing.

If you are patient and careful, you can use this strategy to build a portfolio of assets that will provide passive income!

Remember…

“Landlords grow rich in their sleep.”

John Stuart Mill

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

Real estate investing can be a great way to make money and build wealth over time.

But every investment has its risks. It is essential to do your research and understand everything before getting started.

One more thing I want to say is that we have also been very fortunate.

The past few years have been a perfect time to invest in real estate in Utah. We could buy a house when the price was still relatively low and then watch it increase in value.

The value is still increasing, and having rental income as passive income is a fantastic thing!

We are grateful we have made $400,000 in profits with our real estate strategy.

Although we don’t place all our investment eggs in real estate, it has still been a powerful FIRE tool!

We’d love to hear your thoughts! Feel free to drop a comment or question below.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

So, you’ve decided to invest in real estate in Utah, but you’re not sure how. Yes, how. It may sound odd initially, but figuring out how is the hardest part.

After all, now you’re focusing on the nuts and bolts of the real estate buying process. The good news is that we’re here to help.

First, let’s talk about what you need to do before you start searching for properties.

You’ll need to have a clear idea of your investment goals. What are you hoping to achieve by investing in real estate?

Are you looking to generate income, build equity, or both? Once you know your goals, you can search for properties that fit your criteria.

If your investment goal is to get stinking rich, you must rethink everything from the ground up. No, but seriously, clearly understand what you want to achieve with your real estate investment before you start searching for properties.

Are you looking to generate income, build equity, or both?

Don’t make the mistake of thinking that you will make huge amounts of money overnight. It doesn’t work like that.

Yes, you can make money from real estate, but it takes time, patience, and a lot of work. We enjoy investing where our cash flows are healthy, and we rent out for the long term.

Now that you know your investment goals, it’s time to start searching for properties. But where do you even start?

The first step is determining the type of property you’re looking for. Are you interested in single-family homes, multi-family homes, or commercial properties?

So once you’ve decided on the property type, you can start looking for specific properties that fit your criteria. When you’re searching for properties, be sure to keep your investment goals in mind.

For example, if you’re looking to generate income, you’ll want to find a property in a good location with the potential for positive cash flow. On the other hand, if you’re looking to build equity, you’ll want to find a property with the potential for appreciation.

We have an excellent Realtor, but my wife found a new listing before our Realtor when looking for our second property in Utah. We love using UtahRealEstate.com but Zillow and other real estate listing sites work too.

3. Get pre-approved for a loan

If you’re planning on financing your real estate purchase, the next step is to get pre-approved for a loan. The best way to do this is to talk to a lender and get an idea of what you qualify for.

Getting pre-approved for a loan will give you a better idea of your buying power and make the real estate buying process a lot smoother.

Here’s what you need to know about the pre-approval process:

-The lender will look at your credit history and income to determine how much money you can borrow.

The lender will also give you a pre-approval letter, which says how much money you can borrow.

The pre-approval letter does not guarantee you will get the loan but shows sellers that you’re a serious buyer.

4. Find a real estate agent

If you’re unfamiliar with the real estate market in Utah, finding a real estate agent who can help you with your search is a good idea.

An excellent real estate agent will be familiar with the area, and they’ll be able to help you find properties that fit your investment goals.

You don’t have to go through a real estate agent, but it might be a good idea to have someone who knows the market help you if you’re not from the area.

If you plan on going on your own, be sure to do your research so you know what you’re doing.

5. Get the building inspected

Most people overlook this step; however, it’s one of the most important steps in the process. Once you’ve found a property that you’re interested in, you need to get it inspected.

A home inspection is important because it will help you identify any potential problems with the property. For example, if there are any structural issues or problems with the plumbing or electrical system.

A home inspection is not required, but it’s a good idea. It’s better to know about any potential property problems before making an offer.

6. Make an offer

Once you’ve found a property you’re interested in and inspected, it’s time to make an offer. Always make an offer that’s well below the asking price.

The seller will usually counter your offer, and you can start negotiating. Remember, the goal is to get the property for the lowest price possible.

Don’t feel like you have to rush into making an offer. Take your time and make sure you’re getting the best deal possible.

If you feel that the seller is unreasonable and you’re interested, wait for a few months to see if the house is still on the market. If it is, they may be willing to negotiate more since they know you’re still interested.

7. Close on the property

If your offer is accepted, it’s time to close on the property. This is the final step in the process, and it’s when you’ll sign all the paperwork and officially become the property owner.

Before closing on the property, ensure you have all your financing. You don’t want to get to the closing table and realize you don’t have enough money to buy the property.

Closing on a property can take a few weeks, so be patient. Once everything is finalized, you’ll be the proud owner of a new piece of real estate.

Congratulations! You’ve just learned how to invest in real estate in Utah. Just remember to take your time, research, and ensure you get the best deal possible.

If you’re new to this great state, give yourself time to get familiar with the different areas. You can start searching for properties that fit your investment goals.

You need to know where the hot spots are and where people want to move. With that knowledge, you’ll find properties that will appreciate over time.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

When Warren Buffet talks, we all tend to listen. So, it’s no surprise when he talks about the S&P 500 as a reliable investing choice that people want to learn more about it.

This article provides a solid background for understanding what the S&P 500 is, why Warren Buffet recommends it, how to invest in it, and much more!

What is the S&P 500?

The Standard & Poor’s 500, or S&P 500 for short, is an index containing 500 large-cap stocks. It’s considered a benchmark for the stock market, and it’s often used to gauge the overall market’s performance.

The main thing that makes the S&P 500 attractive to investors is its diversified index. This means that it’s made up of various stocks, which helps mitigate risk.

The answer to that question is quite simple: he believes it’s a good investment.

Warren Buffett once said, “In my view, for most people, the best thing is to do is owning the S&P 500 index fund”.

There are a few reasons why Buffett thinks the S&P 500 is a good investment.

First, he likes that it’s a diversified index. As we mentioned before, this helps to mitigate risk.

Second, Buffett likes the S&P 500 because it’s a long-term investment. This is something that he’s always been a big proponent of. He believes you should invest long-term and not try to time the market.

Lastly, Buffett likes the S&P 500 because it has a history of outperforming actively managed mutual funds. Over the long run, the S&P 500 has consistently outperformed mutual funds. This is likely because mutual fund managers often make poor investment decisions.

Which S&P 500 funds does Warren Buffet own?

Warren Buffet owns a few different S&P 500 index funds. These include the Vanguard 500 Index Fund (VOO) and the SPDR S&P 500 ETF (SPY).

Why does he own these funds in Berkshire Hathaway?

The answer to this question is twofold. First of all, as mentioned before, Buffett is a big proponent of index investing. By owning these funds, he can get exposure to the S&P 500 without picking individual stocks.

Secondly, Berkshire Hathaway is a large holding company. This means that it can hold a lot of different stocks and not be as impacted by the performance of any one stock.

How much can you earn with the S&P 500?

You can earn 10% on average with the S&P 500. This return is based on the historical average return of the index. Of course, depending on the overall market’s performance, you can earn more or less than 10%.

You’ll likely make more than 10% if the market does well. However, if the market does poorly, you could earn less.

It’s possible to earn even more than 10% if you invest in a fund that tracks the S&P 500. Some examples include VOO and SPY.

So it’s essential to start investing as soon as possible and consistently over the years. My wife and I started in our early 20’s and have loved the S&P 500 index fund. The power of compound interest will work wonders for you.

You may wonder how much you would need to invest in the S&P 500 each month to become a millionaire. I’ve put together the following numbers based on an annual 10% rate of return, starting with zero money in investments and retiring at the age of 60.

Age

Monthly Investment Amount

20

160

25

270

30

450

35

770

40

1330

45

2425

50

4900

How long to get one million by investing in the S&P 500. Using the Dave Ramsey Investment Calculator.

You can try many more scenarios using the Dave Ramsey Investment Calculator! We love this calculator and have used it many times to help us stay on track and adjust when necessary.

How Much Does It Cost to Invest in the S&P 500?

It doesn’t cost much to invest in the S&P 500. You can invest in it through index funds or ETFs.

If you’re looking for the cheapest way to invest in the S&P 500, Vanguard’s S&P 500 ETF (VOO) has an expense ratio of 0.03%, while the Vanguard 500 Index Fund Admiral Shares (VFIAX) has an expense ratio of 0.04%. So, you can see that it doesn’t cost much to invest in these index funds.

Do S&P 500 ETFs and Funds Pay a Dividend?

Yes, both S&P 500 ETFs and index funds pay a dividend. The dividend yield on the S&P 500 is around 2%.

If you invest $10,000 in the S&P 500, you can earn $200 in dividends yearly. But, of course, this number will fluctuate depending on the overall market’s performance.

What Are the Risks of Investing in the S&P 500?

You should be aware of a few risks before investing in the S&P 500.

First, it’s important to remember that the stock market is volatile. This means that it can go up or down at any time.

If you’re investing long-term, this shouldn’t be too much of a concern. However, if you need your money sooner, you should be aware of the risks.

Another risk to consider is the fact that you’re investing in a basket of 500 stocks. This means that if one stock goes down, it could significantly impact your investment.

To mitigate this risk, you can invest in an S&P 500 index fund or ETF. This will help to diversify your investment and reduce the impact of any one stock.

As with any investment, there’s risk involved. You’ll find that generally speaking, the S&P 500 is a fairly safe investment. However, it would be best if you always did your own research before investing in anything.

Should I invest in S&P 500?

Warren Buffet thinks so! The S&P 500 has outperformed mutual funds over the long run. This is likely because mutual fund managers often make poor investment decisions.

Index investing is a much simpler way to invest. You don’t have to worry about picking individual stocks. Instead, you can get exposure to the entire market by investing in an S&P 500 index fund or ETF.

The problem with choosing another form of investing is that you have to outsmart the market. This is a difficult task for even the most experienced investors.

If it were so easy, everyone would be like Warren Buffett. If you want to mitigate the risk as much as possible, invest in the S&P 500.

Diversity is your friend when it comes to investing. Remember, the S&P 500 is made up of 500 different stocks. This provides you with a good level of diversification.

Many people enjoy the strategy of investing in the S&P 500. It’s a simple and effective way to get exposure to the stock market. Plus, it doesn’t require you to outsmart the market.

If you’re looking for a simple and effective way to invest, the S&P 500 is a great choice!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you’re looking for a sound investment, you should consider investing in real estate in Utah. The market here is booming, thanks to a strong economy and a growing population. And with relatively affordable prices, now is the perfect time to buy.

In this article, I’m excited to share 11 reasons why investing in real estate in Utah is smart.

This post may contain affiliate links; please see our disclaimer for details.

Delicate Arch from Arches National Park, Utah

1. The economy is strong and growing

Utah’s economy is one of the strongest in the nation, with a job growth rate that outpaces the national average. And as more people move to the state, that growth is expected to continue. That means there will be more demand for housing, which is good news for investors.

The economy has grown steadily since the Great Recession and is now one of the strongest in the nation. The job market has recovered, and the state is seeing population growth thanks to in-migration. All of this is good news for the real estate market.

2. Prices are still relatively affordable

Although prices have been rising recently, they’re still relatively affordable compared to other countries markets. That means there’s still room for appreciation, making now a great time to invest in Utah real estate.

If you invest now, you’ll be able to buy low and sell high as prices continue to rise. There’s little doubt that prices will continue to go up in the coming years, so now is the time to get in on the action.

3. The market is diversified

The Utah real estate market is quite diversified, with various property types. Whether you’re looking for single-family homes, condos, apartments, or even commercial real estate, you’ll be able to find it here.

This diversity allows investors to diversify their portfolios and hedge against risk. You can invest in different property types to spread out your risk and maximize your chances for success.

4. There’s a strong rental market

The rental market in Utah is quite strong, thanks to the state’s growing population. More people are moving to Utah than ever, and many are looking for rental properties.

Investing in rental property is a great option if you’re looking for a steady income stream. You can charge market rent and enjoy a healthy return on your investment.

We currently have one rental property in Utah, which has provided us with nice cash flow each month. The rental market is indeed solid here. I wrote a separate article you can check out about How We Became First Time Landlords In Our 20’s. We have loved the opportunity to invest in the Utah real estate market.

5. The market is primed for growth

Thanks to the strong economy and growing population, the Utah real estate market is primed for growth. Prices are still relatively affordable, and there’s a strong demand for housing.

Utah is definitely worth considering if you’re looking for a potential market. Now is the perfect time to invest in this booming market.

6. You can get in with a small investment

If you compare Utah with, let’s say, California, you’ll see that the entry point to investing here is much lower. In California, you’ll need millions of dollars to get started in the market. But in Utah, you can get started with a small investment.

It only takes a couple hundred thousand dollars to get started here. And with relatively affordable prices, you can buy a lot more property for your money. That gives you the potential for a higher return on your investment.

7. There are plenty of financing options

If you’re worried about financing, don’t be. Whether you’re looking for a conventional loan or a more creative financing solution, many options are available.

You can get started in the Utah real estate market with as little as 3% down. And if you have good credit, you can qualify for even better terms.

Financing is such a big issue for investors because it can make or break a deal. If the financing falls through, the whole deal can collapse. But with so many options available, you’re sure to find a solution that works for you.

8. The market is accessible

The Utah real estate market is quite accessible, especially if you’re from out of state. There are direct flights from all over the country, and the state is well-connected by roads and highways.

You can easily get to Utah no matter where you’re in the USA. And once you’re here, getting around is a breeze. That makes it easy to check out properties and meet with potential tenants.

9. You can find turnkey properties

You can always find turnkey properties if you don’t want the hassle of fixing a property yourself. These properties are already in good condition and ready to be rented out.

You can find turnkey properties in a variety of price ranges. And with the strong demand for housing, you’re sure to find tenants quickly.

10. Utah has lots of undeveloped lands

Maybe you want to build the next suburban enclave that houses many families. If that’s the case, you’ll be happy to know that Utah has lots of undeveloped lands.

Building permits are easy to come by, and you can find plenty of contractors to do the work. With a little planning, you can build the development of your dreams.

11. Utah is a peaceful place you’ll love calling home

Lastly, it’s worth mentioning that Utah is a great place to live. It’s safe and clean, and the people are friendly. Utah is worth considering if you’re looking for a place to raise a family or retire.

The reason is simple: Utahians aren’t like anyone else in the country. They’re hardworking, honest, and down-to-earth. You won’t find a more friendly or welcoming group anywhere else.

The people here have values that are the foundation of the state. And that’s something you can’t put a price on.

Final thoughts

Summing up, there are plenty of reasons to invest in the Utah real estate market. Prices are still affordable, and there’s a strong demand for housing. The market is accessible, and you can find turnkey properties.

Utah is worth considering if you’re looking for a safe, peaceful place to live or invest. The people here are hardworking and down-to-earth, and they have values that are the foundation of the state. You won’t find a more friendly or welcoming group anywhere else.

Don’t wait – investing in Utah real estate is now. With relatively low prices, you can potentially make a great return on your investment. So get in while you can and reap the rewards for years.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.