My wife and I contacted our student loan provider shortly after the Biden Student Debt Relief Program was first announced last year.

We received a refund from our loan provider but have been waiting to see if the forgiveness portion will eventually get passed, or not. Regardless, the refund was just sitting in my bank account and not being very productive there, so I had to make a decision, I’ll jump into more on that later.

The most current update is that the student debt relief plan is still blocked, and if it’s not resolved by June 30, 2023, the loan repayment freeze will end and payments will continue 60 days after that.

In this article, I will share our process for applying for a refund/loan forgiveness and how it actually turned out to be a great investment opportunity for us.

This post may contain affiliate links; please see our disclaimer for details.

Table of Contents

Biden Student Debt Relief Program Details

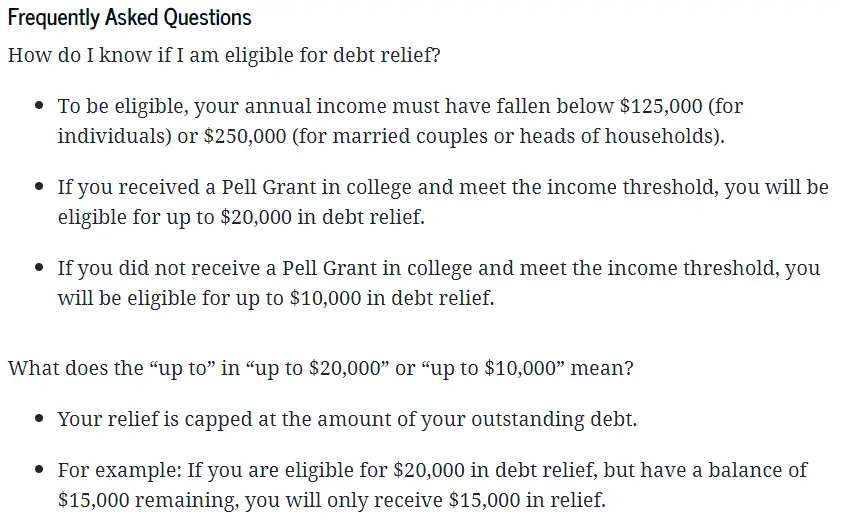

Those with federal student loan balances on or before June 30, 2022 could potentially receive a refund of up to $20,000. Loans dispersed after July 1, 2022 don’t qualify and private loans do not qualify.

Here are some more eligibility details from studentaid.gov:

The good news is that since I had paid off my loans during the pandemic (I made payments since March 2020), I was eligible for a refund! Next, I’ll share my exact application process for the refund and forgiveness parts.

Our Application Experience

My student loans were housed with Navient but then moved to a company called Aidvantage. Upon hearing the debt relief announcement, I called Aidvantage to see if I was eligible for a refund.

It was pretty funny because they did not have a formal process yet but took down my request and put me on a list. After calling back and waiting a bit longer, I eventually received a refund for a little over $20,000 since I previously had pell grants.

So I want to add an important note that I only received the refund, NOT the forgiveness. So technically, the $20,000 is still owed as of right now, but the good news is that I don’t have any payments due and zero interest charges.

I submitted my application for the forgiveness portion of the Biden student debt relief program on studentaid.gov, but as mentioned before, it has been blocked, and they are not accepting any more applications at this time.

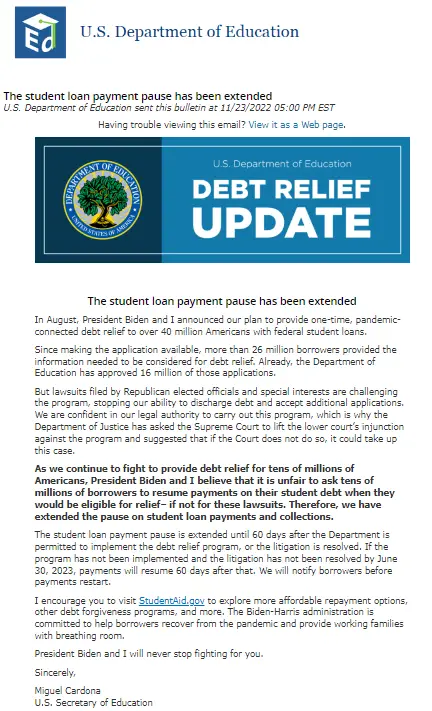

Here is a copy of the email I received saying I was approved for loan forgiveness, but the pause had been extended.

Why is it an Investing Opportunity

With the debt relief plan continually getting blocked, my wife and I realized it probably wasn’t the best option to have that refund sitting in our regular bank account.

We could instead have it work harder for us by putting it into a high-yield savings account.

That would increase our high-yield savings balance to about $40,000 and give us about $120 in MONTHLY in interest payments! This is because our high-yield savings account is with CITI bank with an interest rate of over 3%!

Although it may not seem like a lot, those interest payments can really add up, and we could have well over $700 by the time the refund amount is forgiven from our loan provider or we have to pay back the $20,000, but keep the interest.

Why a high-yield savings account?

First: a high-yield savings account is a type of savings account that offers a higher interest rate than a traditional savings account. This can really add up over time.

Second: you can access the money immediately. Let’s say Biden’s loan forgiveness doesn’t go through, I’d still be able to quickly pull out the funds and pay off the debt. It would take longer to pull the money out of a 401k or other investment account, not to mention it would be riskier in those types of investment accounts.

When choosing a high-yield savings account, it is important to compare the features and fees of each option to find the best fit for your needs.

You can find high-yield savings accounts at both online and brick-and-mortar banks.

Many online banks offer higher interest rates than traditional banks, so it is worth considering an online option if you are looking for the best return on your investment. For more, you can visit this article I wrote sharing High Yield Savings Accounts – Should you have one?

A great place to get started with your savings account is CIT Bank. They offer very competitive saving rates with no monthly maintenance fees.

With their Saving Connect Account, you can earn 12x the national average! There are no ATM fees, and you have the convenience of online banking.

Rest assured, CIT Bank is also FDIC insured!

Conclusion

If you find yourself in the same boat where you have a refund sitting in your bank account, it may be a good idea to get it moved over to a high-yield savings account. Overall it is considered very safe.

I would definitely NOT recommend putting your refund into the stock market or somewhere with higher risk and volatility. Sorry crypto, maybe next time.

The same principle goes for any extra money you have lying around. Instead of keeping it a low-interest, regular savings account, move it on over to a high-yield savings account.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!