When it comes to financial advice, there are few people as well-known as Dave Ramsey. His 7 Baby Steps have helped millions of people get their finances in order and achieve their goals.

But you may be asking yourself, does the program really work?

In this blog post, we will break down each step of the program and give you our opinion on whether or not it is effective.

We will also provide some tips on how you can follow the steps yourself and see results!

This post may contain affiliate links; please see our disclaimer for details.

Breaking Down the Dave Ramsey 7 Baby Steps

Dave Ramsey’s philosophy for personal finance is based on the idea that you shouldn’t take unnecessary risks with your money.

A simple and disciplined approach will set you up for success in the long run.

It is not the most exciting approach, but it has proven effective for many people.

However, it may not work for everyone. This is because mindset and behavior are key factors in financial success.

Some people don’t find any issue with a slow and methodical approach, while others crave the excitement of taking risks.

Dave Ramsey’s baby steps will work wonders for someone looking to settle down, raise kids and save for retirement.

Young entrepreneurs with ambitions that differ from these aspirations may find the program too restrictive.

It depends on your goals, lifestyle, and risk tolerance.

That said, Dave Ramsey’s baby steps include insightful wisdom about personal finance that anyone can benefit from.

Let’s explore each of his financial steps in more detail!

Baby Step 1: Save $1,000 to start an emergency fund

The first step is to save $1000 as quickly as possible.

This may seem like a lot, but it is important to have an emergency fund in case something unexpected comes up.

Once you have saved this money, you can move on to the next step.

Tips for this baby step:

Start by saving $50 from each weekly paycheck. This will get you to your goal of $1000 in 20 weeks.

If you get a bonus or tax refund, put it towards your emergency fund.

Cut back on expenses so that you can save more money each month.

Dave Ramsey recommends this because it will save you a lot of money in interest payments.

He also believes that your home should be paid off before you retire.

Having a place where you can live rent-free can be a huge financial burden lifted off your shoulders in retirement.

It can free up cash flow for other things, like travel or hobbies.

Tips for this baby step:

Make extra payments each month.

Refinance to a shorter loan term.

Apply any windfalls towards your mortgage balance.

Baby Step 7: Build Wealth and Give (Like No One Else!)

Dave Ramsey recommends that you invest in mutual funds.

He also believes that you should give generously to charities and other causes that are important to you.

His belief on wealth is that it should be used to bless others and not just for your personal gain.

Dave Ramsey is not a fan of gambling or higher-risk investments. This is because he has seen too many people lose their hard-earned money in these types of investments.

Tips for this baby step:

Invest in a mix of different mutual funds to help minimize risk.

Save automatically each month with a dollar-cost-average strategy.

Give generously to charities and other causes that are important to you.

Do the Baby Steps Really Work?

Ramsey’s baby steps have helped people across the globe get out of debt and live better lives.

Although we do not follow all of his steps, we feel most of his teachings are on the right track, especially for those looking to gain control over money and avoid risk.

Having an emergency fund has provided us with profound peace of mind. The debt snowball helped me pay off 56K in student debt!

Using cash to buy reliable second-hand cars has been a great benefit to us as well.

We have also opened up education savings accounts for both of our kiddos.

We follow most of Dave’s teaching but with a few key differences.

We believe that you should start saving for retirement as early as possible.

The earlier you start, the more compounding interest will work in your favor, even if it’s just a little each month.

We agree that consumer debt should be paid off aggressively. However, not all debt is bad debt.

Debt can be a wise investment decision and can be used to purchase assets, such as real estate or a business.

We currently have one rental property and see it as a valuable asset where the reward outweighs the risk.

Using credit cards to build credit has been a great tool for us, but they must be used very carefully.

Step 5 is also not applicable to everyone as some people prefer not to have children or cannot have children. In this scenario, people can still benefit from following the other steps.

All in all, we think that Dave Ramsey’s baby steps are a great starting point for anyone looking to get out of debt and improve their financial situation.

However, it is important to take into account your personal circumstances when following his advice.

Some people believe that Dave Ramsey’s advice is too ‘old school’ and that he is too rigid with his approach.

Critics believe that he needs to get caught up with the new realities of finances. However, it is difficult to deny the timeless wisdom he teaches.

It clearly applies to money management, no matter what the current economic conditions may be.

Dave Ramsey Baby Steps: Conclusion

Whether you agree with him or not, Dave Ramsey’s baby steps have helped millions of people get out of debt and improve their financial situation.

For that, we believe that he is worth considering if you are looking for advice on getting your finances in order.

Dave Ramsey seems like a genuine person and really does take plenty of time to help people.

He is America’s favorite financial coach, and for good reason.

Ramsey provides practical solutions that have helped millions get out of debt and improve their lives.

Although we do not agree 100% with his exact steps, his teachings are fundamental and can undoubtedly be a saving grace for many people, including us.

We hope this has helped clear some things up for you if you are wondering whether Dave Ramsey’s baby steps actually work.

Do your own research and be sure to carefully consider your personal circumstances before making any financial decisions.

If you are considering using Ramsey’s baby steps to help you get out of debt, we suggest you speak with a financial advisor to see if it is the best action for your unique situation.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Living paycheck to paycheck is a common occurrence for many Americans. A recent study found that over 64% of Americans are now living paycheck to paycheck.

If you’re one of those people, don’t worry – you’re not alone. It does NOT mean that you have to continue living this way.

You can take steps to stop living paycheck to paycheck and start building wealth for the future.

It’s important to have strategies and steps to break the cycle of living paycheck to paycheck.

Here are the five ways that you can do just that:

1) Know Thy Spending

This may seem like an obvious step, but hear me out.

It’s important to sit down and figure out where your money goes each month.

The first step is to make sure you have a clear understanding of your spending.

Next, you can make changes to ensure your money goes where you want it to.

To budget effectively, make sure to track all of your spending for at least a month.

Many helpful apps and websites, such as Mint or You Need a Budget (YNAB), can make this process easier.

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

Budgeting is the first step because it shows exactly how much money you have coming in and where it’s going.

From there, you can make changes to ensure that your spending aligns with your goals.

Take action on this first step to help you stop living paycheck to paycheck.

2) Make Saving a Priority

It can be difficult to save money when you feel like you are already struggling to meet ends.

However, it is important to remember that saving is an investment in your future.

You should set aside a certain amount of money each month that will go directly into savings.

This will help you build up a cushion for unexpected expenses.

Not to mention it also brings peace of mind knowing that you have some financial security.

One way to do this involves first looking at your current lifestyle. Then make changes that will allow you to live within your means.

For example, if you eat out several times a week, try cooking at home more often.

Or if you have a gym membership that you never use. Make sure to cancel it and start working out at home or outside instead.

Many people live paycheck to paycheck, not necessarily because they do not have a sufficient income. The problem occurs when spending money is spent on unnecessary items instead of allocated to savings.

Make saving a priority by setting up a budget and sticking to it.

Refining your money mindset to no longer need instant gratification and instead focus on long-term gain.

You will be well on your way to breaking the cycle of living paycheck to paycheck.

3) Pay Yourself First and Invest!

One of the best ways to break the paycheck-to-paycheck cycle is to pay yourself first.

Instead of paying the Uber driver, nightclub staff, and brand owners, put that money into savings first.

One of the best investments you can make is in yourself.

Examples include taking care of your health, continuing your education, and building your skillset.

When you invest in yourself, you are ensuring that you will always have something to offer.

Instead of investing your energy in non-productive activities, use that time to build a skillset or improve your wealth by attaining skills.

These investments will last a lifetime and provide you with more opportunities.

If your emergency fund is sufficient, you should also start investing your money instead of letting it sit in a savings account.

This is because inflation will keep you living paycheck to paycheck.

If the inflation rate is at 10%, for example, you would need a 10% raise to maintain your current standard of living.

A common misconception is that you need a lot of money to start investing.

However, there are many options available that allow you to start investing with very little money.

For example, Acorns is an app that allows you to invest your spare change. You can get $10 signing up when you use this link! – ACORNS $10 SIGNUP BONUS.

With the rate of money printing stealing your wealth and advertisers asking you to pay their businesses first, it can be difficult to resist this temptation.

However, if you want to stop living paycheck to paycheck, you must start paying yourself first.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

We only have so many hours we can work each day. Even if we consistently got a raise, the total amount of money we could make is still capped.

The best way to increase your income is to create or invest in passive cash flow-producing assets. Then you can start making money 24/7.

Making money while resting, improving your skillset, or being busy with any other activity is essential to financial success.

You can invest in stocks, bonds, and mutual funds to get started.

You can also create a blog or YouTube channel and generate revenue through ads and sponsorships.

You can buy a rental property or create an online course if you have more money to invest.

There are many options available to you, and it is important to research to find the best option.

However, once you have started investing in passive cash flow-producing assets, you will be on your way to financial freedom.

The key to financial freedom is reinvesting this passive income each month to allow for more cash flow and eventually break the paycheck-to-paycheck cycle.

You will be surprised by how much of a difference even a few hundred dollars a month can make on your bottom line.

If you do not have any money to invest in a passive income source, focus on creating one in your spare time.

For example, a dropshipping business can be started with very little money. The key is to focus on generating revenue and not letting your expenses exceed your income.

Another online business that can be set up to create passive income is a content creation service.

You can hire virtual assistants for a low cost and train them to use free design programs like Canva.

Once the system is built, you can sell your services to brands and outsource all the design work to your team.

You can also sell unused items in your home and reinvest that money in passive income-producing assets such as vending machines or a rental property.

If you are a few dollars short, consider working overtime or picking up a second job to afford the investment.

Of course, you can invest in dividend-paying stocks or distribution-producing REITs to generate passive income.

Another option is to try peer-to-peer lending. These require fewer business skills and more research to find the best opportunities.

However, they can be a better option for some people as they can be easier to start.

Once you have started generating passive income, it is important to reinvest that money so you can continue to grow your wealth.

As you can see, being creative in your approach can unlock many opportunities to bring you out of the paycheck-to-paycheck cycle.

Passive income is not reserved for those that are already rich.

In fact, it is often the best way for those with limited resources to get started on the path to financial freedom.

5) Say Bye Bye to Debt

We left this step last because it is the most difficult one to overcome.

Debt is so difficult to pay down because it has a way of creeping back up on you after you have made progress.

It may be helpful to focus on passive income-producing assets first because you can use that income to pay down your debt faster.

The extra cash flow will give you more breathing room to make progress on paying off your debt without sacrificing other areas of your budget.

Just make sure you are paying down at least the minimum while mastering the other steps on this list. This will help prevent your debt from spiraling out of control.

If you are struggling to make ends meet, consider using a debt consolidation loan or credit counseling service to help you get out of debt.

These services can help you develop a plan to pay off your debt and get your finances back on track.

Remember that not all debt is bad debt.

Debt can be used to purchase assets that produce cash flow and help get you out of a paycheck to paycheck cycle.

Just be sure to use it wisely and not let it get out of control.

Consumer debt, such as credit cards and lines of credit, should be paid down as quickly as possible.

If you can focus on avoiding this type of debt, you will be in a much better position to stop living paycheck to paycheck.

The Bottom Line

If you want to stop living paycheck to paycheck, you need to increase your monthly income while decreasing your monthly expenses.

Once you have a positive cash flow, invest that difference into income-producing assets.

Repeat this step by reinvesting and start paying down your consumer debt if you have any.

There are many different ways to increase your income and decrease your expenses. The most important part is to start now.

You can be creative in your approach, or you can follow a simple strategy.

The journey to financial freedom varies, so find what works best for you and stick with it.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Generational wealth is a term used to describe the accumulation of assets and income over successive generations.

In this article, we will answer the following questions-

What is generational wealth?

Why is it important?

How to go about building it?

This post may contain affiliate links; please see our disclaimer for details.

Generational Wealth

We will also explore ways in which you can pass down valuable assets to future generations.

Keep on reading to learn more!

What is Generational Wealth?

Generational wealth is the transfer of assets from one generation to another. The concept of generational wealth is important because it allows families to maintain their economic status and accumulate wealth over time.

It can be in the form of property, stocks, bonds, or other assets.

Many families pass down their wealth through trusts or other legal mechanisms. It is important to note that not all families have generational wealth.

Most families do not have significant amounts of wealth. For these families, intergenerational transfers are often in the form of human capital (skills and knowledge) or social capital (networks and relationships).

However, for families with generational wealth, it can be a powerful tool for maintaining economic stability and upward mobility.

Several factors contribute to the accumulation of generational wealth.

One of the most important is education. Families with higher educational attainment levels are more likely to have wealth.

Another important factor is inheritance. Families who inherit property or other assets are more likely to have generational wealth.

Finally, families who own businesses are more likely to have more money and assets that can be passed down to children and others.

Education, inheritance, and business ownership are all important factors in accumulating generational wealth.

However, they are not the only factors.

Generational wealth is just one tool families can use to maintain their economic stability and improve their prospects for upward mobility.

Individuals can still accumulate wealth without receiving money from past ancestors.

My wife and I hope to give our children some generational wealth to support them, but MORE importantly, we will strive to help them understand and take dominion over their finances.

Teach wealth-building habits

Why is Generational Wealth Important?

Generational wealth is important because it allows families to maintain their economic status and accumulate wealth over time.

Families with this type of multi-generational wealth can transfer assets from one generation to another, giving them a leg up in maintaining their economic stability.

In addition, these families are more likely to own their businesses, which can provide a source of income and additional stability.

While generational wealth is not the only factor contributing to a family’s economic success, it can be important.

Families with generational wealth are more likely to be economically successful than those without, but teaching correct money habits is equally, if not more important.

Therefore, building generational wealth is a good place to start if you are looking for ways to improve your family’s economic prospects.

With generational wealth and proper finance education, you can ensure that your family has a bright future.

If you are not born into generational wealth, don’t worry because you can begin building it now!

It’s important to ask yourself –

How can you build generational wealth?

How can you create a legacy that will last long after you are gone?

The fact that you are interested and have the desire already puts you ahead of most people. There are a few key things to remember when building up your wealth:

Start Early

There are many ways to approach this, but one of the most important things is to start early.

The earlier you start saving and investing, the more time your money has to grow.

This is why it is so important to teach financial literacy to young people. They need to understand how money works and how to make it work for them.

Build a Business

Another way to build generational wealth is by starting your own business. This can be anything from a small online business to a brick-and-mortar store.

If you are passionate about something and have a unique offering, there is no reason why you cannot be successful.

Not only will you be creating your wealth, but you will also be creating jobs for others.

Invest

Make sure to take the time to invest in yourself and others.

You can do this through education, mentorship, or investing in stocks and real estate.

Investing in yourself increases your chances of success and makes it more likely that you will be able to help others succeed as well.

The more financial knowledge you acquire, the more you can pass on to future generations!

Taking the time to educate others about money and how it works is also a great way to build generational wealth.

When you can help others learn about personal finance, you set them up for success.

This way, the community your children grow up in will be prosperous and full of opportunity.

Stocks can compound over time and create a lot of wealth.

If you continue to pass on these assets over generations, the compounding effect will work wonders for generational wealth.

Investing in the community will allow your family to be accepted and respected by future generations.

Doing so will open doors of opportunities for the next generation because they will know they have their elders’ support.

One way you can increase your savings and investments is by mico-investing.

ACORNS is a popular platform that can round up money from purchases and automatically allocate those funds to diversified investments.

Finally, one of the most important things to remember when building wealth is to be generous and think outward.

It is important to give back to the community and those less fortunate.

By doing this, you are not only helping others, but you are also building a good reputation for your family.

Future generations will reflect on your generosity and be proud to call themselves part of your legacy.

These are just a few ideas to start your journey to building generational wealth.

The most important thing is to start now and never give up on your dreams.

Remember, it is never too late to begin building your legacy!

Protect Your Purchasing Power Through Generations

Inflation is one of the biggest silent killers of wealth.

It’s important to have a game plan to protect the purchasing power of your wealth through generations.

One way to do this is by owning assets that increase in value faster than inflation. For example, if you own a rental property, the rent you charge will likely go up over time as inflation increases. This will help offset any decrease in purchasing power that your wealth may experience.

Another way to protect your wealth from inflation is by investing in assets such as gold and silver. These commodities have a long history of retaining their value during inflation.

If you believe future generations will live in a more digitalized world, cryptocurrencies could provide a hedge against inflation and a possible option to explore.

You can also hedge against inflation by investing in stocks of companies that are likely to benefit from rising prices.

For example, companies in the healthcare sector tend to do well when inflation is on the rise. This is because people will continue to need medical care regardless of how much prices increase.

Utilizing these strategies will help you protect your wealth from the ravages of inflation and ensure that it retains its purchasing power for generations to come.

Building generational wealth is not something that happens overnight, but it is possible with dedication and hard work.

It’s important to start early, invest in yourself and others, and always be learning.

By staying consistent and never giving up, you can create a legacy that will last long after you are gone. 🙂

How to Pass Down Your Wealth?

Many families pass down their generational wealth through trusts or other legal mechanisms.

This gives them more control over how the assets are used and helps to preserve the family’s wealth.

You can pass down your wealth through several different methods, but choosing the right method for your family is important.

You’ll need to consider your family’s needs and objectives and the tax implications of each method.

Here are a few different ways to pass down generational wealth:

Trusts

Wills

Gifting

Trusts are a popular way to pass down wealth because they offer several advantages.

Trusts can be used to control how the assets are used and can also help protect the family’s wealth from creditors or lawsuits.

Wills are another common way to pass down generational wealth. With a will, you can specify how your assets should be distributed after you die.

You can also use a will to appoint a guardian for your children.

Gifting is another option for passing down generational wealth.

You can gift assets to your children or grandchildren during your lifetime. This can be a great way to help them get a head start on building their wealth.

When you’re planning to pass down generational wealth, working with a financial advisor is important.

They can help you choose the best method for your family.

The Bottom Line

Financial knowledge is the most important aspect of passing down generational wealth.

You need to understand your family’s financial situation and objectives clearly.

Your heirs need to know how to manage and invest the money.

And you’ll need to have the plan to transfer the wealth.

We sincerely wish you the best in building your legacy and generational wealth!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Are you considering the idea of quitting your job?

You’ve probably heard of the great resignation by now. Many people are looking to leave their current workplace to find more flexible employment, pursue working for themselves, or retire early.

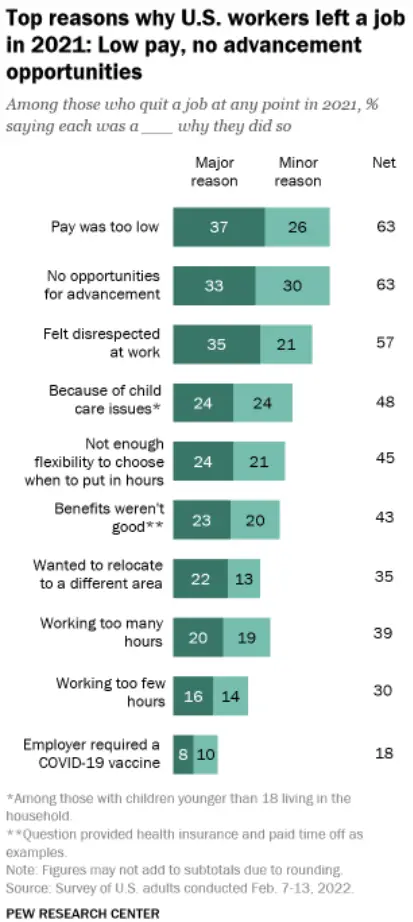

Here are the reasons for the great resignation, according to Pew Research Center:

“Majorities of workers who quit a job in 2021 say low pay (63%), no opportunities for advancement (63%), and feeling disrespected at work (57%) were reasons why they quit, according to the Feb. 7-13 survey. At least a third say each of these were major reasons why they left.”

Roughly half say childcare issues were a reason they quit a job (48% among those with a child younger than 18 in the household).

A similar share point to a lack of flexibility to choose when they put in their hours (45%) or not having good benefits such as health insurance and paid time off (43%). Roughly a quarter say each of these was a major reason”.

It’s crucial to make sure that you do everything possible to prepare for the transition of quitting your job.

Quitting a job can be scary, but if you plan ahead and take the time to do things correctly, it can be a much smoother process.

This article will discuss fourteen things you must do before quitting your job.

By following these tips, you’ll be able to make the transition as smooth as possible!

This post may contain affiliate links; please see our disclaimer for details.

The Benefits of a Smooth Departure

When you leave a job on good terms, it can benefit you in several ways.

For one, getting a positive reference from your former employer will be much easier.

Additionally, if you ever need to return to that company later down the road, they will be more likely to welcome you back with open arms.

Finally, quitting your job on good terms is simply the right thing to do – it’s respectful and professional.

What Should You do Before Quitting Your Job

There are a few key things you should do before quitting your job. Make sure you do these if you wish to leave on good terms. He

Buckle up because here are fourteen things you should do before you quit your job:

1) Give Enough Time Notice

One of the most important things you can do before quitting your job is to give your employer two weeks’ notice. Although this is standard protocol, giving your employer time to find a replacement for you.

Additionally, by giving two weeks’ notice, you’re showing that you respect your employer and the company.

They will be much more likely to give you a positive reference if you give them this courtesy.

Schedule a meeting with your boss to deliver the news in person.

This way, they can ask any questions, and you can explain your decision further.

Giving two weeks’ notice is one of the most important things you can do when quitting your job – make sure not to forget it!

2) Clean Up Your Work Area

Another thing you should do before leaving is to clean out your desk.

Doing so shows that you respect your employer and their property and makes the transition easier for your successor.

Plus, once you’ve cleaned your desk, you won’t have to worry about returning to retrieve any personal belongings – they’ll all be gone!

To clean your desk, start by going through all your drawers and removing any personal items.

Next, review your files and remove anything specific to you or your work. Finally, wipe down your surfaces and vacuum the floor around your desk.

By taking the time to clean out your desk before quitting, you’re making things much easier for everyone involved.

3) Tie Up Loose Ends

Before quitting your job, you should also take the time to tie up loose ends.

Make sure to finish any projects you’re working on, wrap up any open tasks, and ensure that everything is organized and in its proper place.

Tying up loose ends before you leave shows your employer that you’re a responsible and reliable employee. Additionally, it will make the transition smoother for whoever takes over your role.

So take time to finish up anything incomplete – it will benefit everyone involved!

4) Train a Backup or Replacement

If possible, you should also try to train your replacement before leaving your job.

This is a great way to show that you’re committed to the company and want to see it succeed – even after you’re gone.

Training your replacement can be as simple as showing them how to do your job, answering any questions they may have, and providing helpful feedback.

Of course, not everyone will be able to train their replacement, but if you can, it’s worth doing!

5) Save For a Rainy Day

Before quitting your job, you should also save up some money.

This way, you’ll have a cushion in case you need it – whether for unexpected expenses or to tide you over.

Most experts recommend saving up to three to six months’ worth of living expenses, but depending on your situation, you may want to save more.

Ideally, it would help if you aimed to save enough money to cover your living expenses for at least three months. This may seem like a lot, but it’s better to be safe than sorry!

Another important thing to do before quitting your job is to create at least one source of passive income. This will help you keep financial stability even when you’re not working a traditional job.

There are many ways to create passive income, but some of the most popular methods include investing in real estate or stocks.

You can even create a passive income source such as a blog, youtube channel, or online business.

Creating a source of passive income is a great way to prepare for quitting your job – it’ll help ensure that you’re still able to support yourself financially even when you’re not working!

If you are transitioning to another job, having a source of passive income can still be a helpful safety net.

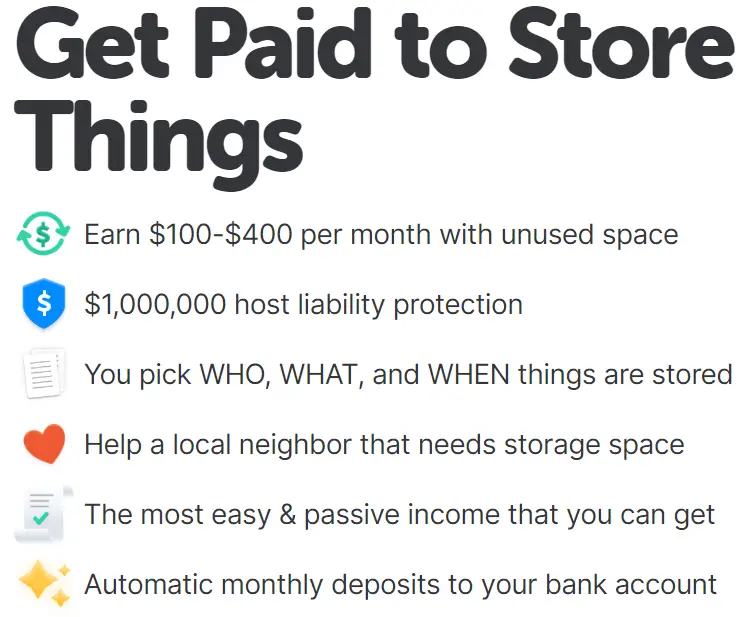

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

7) Have a Plan B

In addition to saving money and creating a source of passive income, you should also have a Plan B in case quitting your job doesn’t work out.

Your Plan B could be anything from finding another job to moving in with family or friends. The important thing is that you have a backup plan in case things don’t go as planned!

Having a Plan B is always a good idea – you never know what might happen, so it’s better to be prepared!

When we quit

8) Continue Your Relationship with Co-Workers

Just because you’re quitting your job doesn’t mean you have to say goodbye to your co-workers!

If you have a good relationship with them, there’s no reason why you can’t stay in touch after you leave the company.

You can stay in touch with your co-workers by connecting on social media, meeting up for coffee or lunch, or simply sending them an email now and then.

Staying in touch with your co-workers is a great way to maintain relationships and keep networking – even after you’ve left your job!

If you are quitting your job to enter a new career that provides a stable income, this is the time to pay off your debts.

By doing so, you can start your next adventure with a clean slate and without the stress of debt hanging over your head.

If you are quitting your job to pursue a more risky career with an unstable income, it is even more important to get out of debt before making the switch.

This will provide a safety net if your new career doesn’t work out as planned.

No matter your reason for quitting your job, it’s always a good idea to get out of debt before making the switch.

Then you can ensure the start of your new chapter in life happens on the right foot!

There are a few different ways to pay off debt, but the most important thing is to make a plan and stick to it!

You can also talk to a financial advisor to help create a debt payoff plan.

10) Have Life Insurance Figured Out

When it comes to life insurance, there are two main types: term and whole life.

The main difference between whole life and term life insurance is that whole life insurance provides lifelong coverage. In contrast, term life insurance only covers you for a specific period.

Make sure to have life insurance figured out before quitting your job.

Don’t forget to keep investing in your tax-advantaged retirement accounts to prepare for a long & happy retirement.

NerdWallet explains there are “five main choices for the self-employed or small-business owners: an IRA (traditional or Roth), a Solo 401(k), a SEP IRA, a SIMPLE IRA or a defined benefit plan”.

Make sure to look through each option and find which choice works best for you.

The Bottom Line

That’s it! These are the fourteen things you should do before quitting your job.

Following these steps ensures that leaving your job goes as smoothly and stress-free as possible.

Quitting your job can be a big decision, but it doesn’t have to be the world’s end.

If you take the time to prepare for it properly, you can set yourself up for success – even after you’re gone.

So if you’re thinking about quitting your job, be sure to keep these things in mind!

Disclaimer:

We hope the information shared in this post provides valuable insights to every reader but we are not financial advisors. When making your personal finance decisions, we recommend researching multiple sources and/or receiving advice from a licensed professional.

This post may contain affiliate links; please see our disclaimer for details.

Couple enjoying financial minimalism 🙂

Financial minimalism is a growing trend in the world of personal finance.

The idea is to enjoy life more by removing unnecessary financial clutter and simplifying your money choices.

In this article, we will discuss what financial minimalism is exactly, the benefits you can experience, and how you can achieve it!

We will also provide fourteen tips to help get you started!

What is Financial Minimalism?

Financial minimalism is living with less financial clutter by consciously deciding to spend less and save more. They believe in living a simple life free of debt and other financial burdens. Financial minimalists focus on quality over quantity.

The main reason why many people are drawn to financial minimalism is that it emphasizes living a simple life.

It’s about being intentional with your money and only buying things that add lasting value to your life.

Give it a try; you might enjoy decluttering your life and living with less spending or only spending on things you need.

For some, it may be a way to save money and become debt-free. Others may want to downsize and live a more sustainable lifestyle. Financial minimalism can help you achieve these things!

It differs from traditional minimalism because it focuses on reducing expenses and debt rather than just on physical belongings.

For example, a physical minimum might live in a small house or apartment and own only a few items of clothing.

A financial minimalist may have a similar lifestyle, but their focus would be reducing expenses and debt instead of physical belongings. It’s all about living within your means and not getting too complicated with spending, saving, and investing.

Financial minimalists are typically practiced by people looking to save money, become debt-free, remove financial clutter, or downsize their lifestyle.

Practitioners must also learn to be disciplined. A lack of focus can easily lead to overspending.

Benefits of Financial Minimalism

The main benefit of financial minimalism is that it can help you save money. It can also lead to a simpler and more sustainable lifestyle.

In other words, it’s a pathway to a sustainable life because if you over-consume financially, you will always be in debt or working to pay off debt.

Eventually, when it is time to retire, you will not have the funds to do so. Being unable to work and still having to pay off debt is an unhealthy way to live.

Financial minimalism can help you avoid that lifestyle and reach financial freedom sooner!

Reduced stress is another major benefit of simplifying your spending and gaining control over your finances.

Financial troubles are often associated with high levels of stress. So, by decluttering your finances, you can reduce stress and live a more joyful life.

Financial minimalism is important because it can help you find joy while saving money.

If you can live with less, you’ll be able to put more money into savings and investments, leading you to a better and brighter financial future!

Sounds pretty amazing, right?

Now that you know what financial minimalism is, let’s learn more about how you can begin to practice this concept.

How to Practice Financial Minimalism? 14 Tips

One way to start practicing financial minimalism is to save up for big purchases instead of buying on credit.

Another great way is to create a budget and stick to it.

You can also declutter your home and eliminate anything you don’t need or use.

Start small and see how it feels to live with less money.

You may be surprised at how much simpler and happier your life becomes! So let’s look at 14 ways you can get started today.

1) Start by evaluating your current spending habits

Track where you are spending your money for 30 days.

Doing so will help you become aware of your spending patterns. By becoming aware of your spending, you can make changes where necessary.

Once you know your spending patterns, start setting aside monthly money for savings and investments.

Begin with $50, for example. Then, increase this amount each month as you become more comfortable.

2) Set meaningful goals for yourself

Ask yourself the following questions-

What do you want to achieve with your finances?

Do you want to be debt-free?

Do you want to save for a down payment on a house?

Next, write down some realistic goals with deadlines to help keep you accountable.

3) Unsubscribe from marketing emails and avoid impulse purchases

Dig deep to find out what your needs are and what really adds value to your life. Most likely, you don’t need that new shirt or those shoes.

Unsubscribe from marketing emails so you’re not constantly tempted to spend money.

Looking for an easy way to manage subscriptions? Look no further than ROCKET MONEY. We love how they provide you with the tools to track spending, lower bills, and track your net worth!

4) Unsubscribe from paid memberships and unused services

Do you need that gym membership? If you’re not using it, take the time to cancel it.

The subscriptions you don’t use or don’t add value to can clutter your credit card statements and add up over time.

5) Create a capsule wardrobe

A capsule wardrobe is a small collection of clothes that can be mixed and matched to create multiple outfits.

This is a great way to save money and declutter your closet!

By having less selection of clothes to wear, you’ll also be able to spend less time deciding what to wear.

Having a capsule wardrobe is a tactic for many physical minimalists but can also be a mindset reminder for financial minimalists!

6) Sell items you no longer need or use

Have a garage sale, sell items online, or donate them to a local thrift store.

By letting go of old items, you make room for new experiences. 🙂

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

7) Start cooking at home more

Eating out is expensive! Save money by cooking meals at home. You can also save money by batch cooking and meal planning.

Batch cooking is when you cook multiple meals at once and then freeze them for later. Meal planning is when you plan out your meals for the week in advance. Some meal-planning services may be worth using, too.

If you’re busy and want a custom meal plan, I recommend trying out NutriSystem! You can start by taking an easy survey. Then they will send you balanced and nutritious meals and snacks!

You can now buy a month and get an entire month free! – Check it out today at NutriSystem! 🙂

8) Live below your means

Spend less than you earn and invest the rest. This will help you build wealth over time.

This tip may seem common sense, but it is one of the most important!

9) Be content with what you have

Be grateful for what you have and learn to live with less. This doesn’t mean you can’t have nice things, but don’t let your possessions own you.

You’ll be much happier when you learn how to appreciate the simple things in life.

10) Invest in experiences, not things

Instead of buying material possessions, invest in experiences. This could include travel, going to concerts, or taking cooking classes.

These experiences may seem like they cost more money, but they will result in more happiness and greater memories than any material possession.

11) Be patient

Financial success takes time and patience. Don’t expect to become a millionaire overnight.

The concept of delayed gratification and actively practicing it can be the difference between financial success and failure.

Delayed gratification is the ability to resist the temptation of an immediate reward and wait for a later, possibly greater, reward.

When it comes to your finances, think long-term.

12) Downsizing your home or getting rid of unnecessary expenses

If you have a lot of stuff, consider downsizing your home. This will save you money on rent or a mortgage.

This step can be difficult when pursuing financial minimalism, but it is worth considering.

An investment approach would be to rent out your current residence and then buy a new property while still living within your means.

13) Don’t compare your financial situation to others

Everyone’s circumstances are different. Focus on your own journey, and don’t compare yourself to others.

Don’t compare your spending to others. For example, if your friends just bought a new car, don’t feel you need to do the same.

People who struggle with financial minimalism cannot get past their insecurities of FOMO (fear of missing out).

14) Automate your finances

Automating your finances is a great way to stay on top of your budget and avoid late fees.

You can set up automatic payments for your bills and have a certain amount of money automatically deposited into savings each month.

By automating your finances, you will stay disciplined with your spending and reach your financial goals.

Conclusion

There are a few different ways to achieve financial minimalism. The most important aspect is to be intentional with your money.

You need to be aware of your spending habits and make changes where necessary.

In addition, try to live below your means. Spend less than you earn and invest the rest. This will help you build wealth over time.

Finally, don’t compare your financial situation to others. Everyone’s circumstances are different.

Focus on your journey, and don’t compare yourself to others.

There’s no one way to achieve financial minimalism. It’s a personal journey that looks different for everyone.

It’s important for those pursuing financial freedom to find what works best for them.

Financial minimalism may not be the right fit for everyone. But if you’re looking to declutter your life and finances, it’s worth giving it a try!

Please comment below with your thoughts and experiences on practicing financial minimalism!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Do you want to retire early? The 4% rule is a common guideline that can help you achieve this goal.

The 4% rule states that you should withdraw no more than 4% of your retirement savings (nest egg) each year to ensure that it lasts throughout your retirement.

This article will explain the 4% rule in more detail and discuss some pros and cons of using this guideline.

This post may contain affiliate links; please see our disclaimer for details.

What Is The 4% Rule?

The 4% rule is a guideline that suggests that you withdraw no more than four percent of your portfolio value each year during retirement. The money you take out can go towards living expenses or other things, such as travel or gifts. The rule is meant to help ensure your retirement funds last without having to go back to work.

Some experts suggest using a slightly lower withdrawal rate, such as three percent or even two and a half percent, especially if you’re retired for 20 years or more.

Regardless of your withdrawal rate, it’s important to remember that the 4% rule is just a guideline.

It’s not set in stone, and there will be years when you may need to adjust your withdrawals up or down based on market conditions and circumstances.

This leads to the importance of having a 2-year emergency fund that can cover all expenses if there is a large drop in the market.

What is the Purpose of the 4% Rule?

Simply put, the purpose of the 4% rule is to help ensure that your money lasts throughout retirement.

This is especially important if you plan to retire for 20 years or longer.

The 4% rule is based on the work of William Bengen, a financial planner who wrote a paper in 1994 about safe withdrawal rates from retirement portfolios.

Bengen looked at historical data to see how different portfolio types and withdrawal rates would have fared over time.

He concluded that a portfolio consisting of 50% stocks and 50% bonds would have had a 95% chance of lasting 30 years if the investor withdrew no more than four percent per year.

How Does The 4% Rule Work?

The rule is simple:

You can only withdraw 4% of your retirement account per year.

If your retirement account is $100,000, you can withdraw $4000 per year.

Now you might be thinking, that’s not a lot of money. And you’re right, it’s not.

But the goal of the 4% rule is to make sure your money lasts throughout retirement, even if you live for 30 years or more.

The rule is based on the idea that your portfolio will grow over time and that the money you don’t withdraw will continue to grow and provide for you in retirement.

There are a few things to remember with the four percent rule.

First, it’s based on historical data and may not hold in the future.

Second, it’s a guideline, not a guarantee – you may need to save more or less depending on your individual circumstances.

For example, if you’d like a more comfortable retirement, you can set a goal of $1,000,000 in your retirement account. With the 4% rule, you could withdraw $40,000 per year!

Finally, it assumes that you will withdraw 4% of your savings each year in retirement, which may not be the case.

Despite these caveats, the 4% rule is a helpful way to estimate how much you need to save for retirement.

By following this rule, you can ensure that you are on track to reach your retirement savings goal.

Using The 4% Rule With An Investment Portfolio

To successfully use the 4% rule, it would need to be in an investment portfolio.

This is because the rule is based on the idea that your portfolio will grow over time, and you can withdraw four percent of the value each year without depleting your savings.

For example, if you’re 30 years away from retirement, the fund may be 90% stocks and just 10% bonds. But if you’re only five years away from retirement, it might be 50% stocks and 50% bonds.

This gradual shift helps to protect your savings while still allowing you to grow your money over time.

The most effective fund for the 4% rule is the S&P 500 Index Fund. On average, the S&P 500 grows at 11.5% per year.

Here is an example of calculating how much you’d need to retire comfortably using the 4% rule with the S&P 500.

The first step would be to decide how much income you’d need to live a financially free life.

The average cost of living for a U.S. citizen is approximately $1100 per month but let’s go with $2000 to be conservative and plan for a great retirement!

To receive a retirement income of $2000 per month ($24,000 per year), you’d need $600,000 invested into your S&P 500 account.

Now let’s see how long it would take to reach our goal of $600,000 using the historical growth rate of the S&P 500 at 11.5% annually.

$600,000 might seem like a lot, but with the power of compound interest and consistent monthly contributions, you can get there with just $121,000 as a total investment.

If you start with $1000 and invest $400 per month into an S&P 500 index fund, it would take 25 years to reach the goal of $600,000. But if you started investing at 25 years old, you could retire with an income of $24,000 at 55 years old!

If 25 years is too long, you can get there in only 15 years with monthly contributions of $1400. As you can see, there are many different variables that you can adjust to make the four percent rule work for you.

The Bottom Line: By calculating your desired income, you can find a retirement number that is comfortable for you.

The important thing to remember with the four percent rule is to start saving early and invest often!

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

What Are The Pros And Cons Of The Four Percent Rule?

There are pros and cons to using the four percent rule as a retirement guideline.

Some of the pros include:

It’s simple to understand and follow.

You can adjust your withdrawals up or down as needed based on market conditions and your circumstances.

It’s a helpful way to estimate how much you need to save for retirement.

It uses the stock market’s ability to grow to your advantage.

Some of the cons include:

It’s based on historical data and may not hold true in the future.

It’s a guideline, not a guarantee – you may need to save more or less depending on your circumstances.

It assumes that you will withdraw four percent of your savings each year in retirement, which may not be the case.

The large number needed can seem overwhelming.

Common Mistakes With The 4% Rule

Regarding retirement planning, the “four percent rule” is a guideline that’s often cited.

The rule of thumb goes like this: If you withdraw four percent of your nest egg each year during retirement, you’re unlikely to run out of money.

But as with any rule of thumb, there are exceptions – and the four percent rule is no exception.

People make several common mistakes when using the four percent rule. Here are eight of the most common:

Mistake #1 – Not Adjusting for Inflation: One mistake people often make with the four percent rule is not adjusting for inflation.

When you retire, your expenses will likely go up – not down. That’s why it’s important to factor in inflation when withdrawing money from your nest egg.

Mistake #2 – Not Taking Into Account Your Longevity: Another mistake people make is not considering their longevity.

Just because the average life expectancy is around 78 years doesn’t mean that’s how long you will live.

If you want to be safe, plan for a longer retirement.

Mistake #3 – Not Planning for Unexpected Expenses: People do not plan for unexpected expenses.

Retirement is often unpredictable, and you may need more money than you think.

Make sure to have a cushion in your nest egg so you can cover any unexpected costs that come up.

Mistake #4 – Failing to take into account your own individual circumstances: The four percent rule is a guideline, not a definite rule.

Your retirement plan should be unique to you and consider your circumstances.

Mistake #5 – Assuming that you will have the same expenses in retirement as you do now: Retirement is often a time when people have time to spend money on things like travel and hobbies that they didn’t have time for while working.

As a result, your expenses in retirement may be different than they are now.

Mistake #6 – Not factoring in Social Security: If you’re eligible for Social Security, be sure to factor this into your retirement plan.

Social Security can provide you with a source of income in retirement, which can help reduce the amount you need to withdraw from your nest egg.

Mistake #7 – Withdrawing in tax-inefficient ways: People do not consider the taxes they’ll owe on their withdrawals.

If you’re not careful, you could owe more in taxes than you need to.

That’s why investing with a tax-efficient account is important from the start.

Mistake #8 – Not having a plan B: Another mistake people make is not having a backup plan. What if the market crashes and your nest egg takes a hit?

What if you live longer than expected and run out of money?

Having a plan B can help you weather any storms that come your way in retirement.

As mentioned previously, we highly recommend having a fully funded emergency fund that can cover all expenses in case of a market crash.

The Bottom Line:

If you avoid these mistakes, you’ll be well on your way to a successful retirement.

Just remember to factor in inflation, plan for long life, and have a cushion for unexpected expenses.

You can make the four percent rule work with those three things in mind.

The Rule of 25 vs. the 4% Rule: What’s the Difference?

The Rule of 25 vs. the 4% Rule

The 4% rule indicates that you can withdraw 4% from your retirement and expect that the returns from your investment will surpass the withdrawal rate.

The problem is that with inflation added to this equation, the purchasing power of your money will decrease over time. If you withdraw 4% and the inflation rate was at 8% last year, you’re withdrawing 12% in purchasing power.

If the growth of your investment were less than 12% last year, then you would have to begin dipping into your principal, which is not ideal. This is where the multiply-by-25 rule comes in.

The rule of 25, on the other hand, is a general guideline that suggests you multiply your total salary by 25 to determine how much money you need to save for retirement.

This rule of thumb assumes that you will want to replace your current income via investments during retirement.

It also factors in an estimated annual return of around 10.5% but is used to calculate the total principal you’d need for retirement. It helps to build a mental framework for those pursuing financial freedom.

The 4% rule calculates how much you can withdraw from your principal after the 25x rule is implemented.

For example, first, you would use the 25 rule to calculate how much you need to have saved. Then, the four percent rule would tell you how much you can withdraw from that savings account each year. The 25x rule is a good starting point, but the 4% helps ensure you don’t outlive your money.

Common Questions About The 4% Rule

Q: How long will it take to retire if I follow the rule?

A: This depends on how much money you have saved and how much you can save each year.

Use the example mentioned above and adjust the variables to your preference.

Q: What happens if my retirement lasts more than 30 years?

A: If you want to retire sooner than 30 years, you will need to invest more each month. This is because compound interest will build more reserves for retirement.

You can also consider withdrawing only 2% rather than 4% to allow your investments to keep growing beyond 30 years.

Q: What if I can’t save enough money to retire?

A: If you cannot save enough money to retire using the four percent rule, there are a few options you can consider.

One option is working part-time in retirement. This can help supplement your income and give you something to do in retirement.

Another option is to downsize your lifestyle. Doing so will reduce your expenses and free up extra cash to help fund your retirement.

Lastly, you can delay retirement. This may not be ideal, but it can give you more time to save money and prepare for retirement.

Q: Is the four percent rule a guaranteed way to retire?

A: No, the four percent rule is not a guaranteed way to retire. It is simply a guideline that many people with success have used.

There are no guarantees in life, so it is important to remember that anything can happen when following this rule.

In Summary

The four percent rule is a simple estimate of your retirement savings needs.

Remember to take into account your circumstances when using this guideline.

With careful planning and consistent investing, you can ensure a comfortable retirement for yourself down the road.

Thanks for reading!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.