First, I want to say that my wife and I hope the coronavirus pandemic can be resolved soon. As many of you know, there are many effects of the Covid-19 pandemic, both good and bad.

Over two years have passed since the pandemic started, but our lives are still affected by it now.

In this article, I will share some positive and negative effects of the coronavirus pandemic. The effects I’ll review significantly impact our work environment, economy, investing opportunities, and more.

This post may contain affiliate links; please see our disclaimer for details.

The Good effects of Covid-19

Remote work opportunity

Investing opportunities (stock market and real estate)

Student loan interest pause

Better habits, less sickness

The Bad effects of Covid-19

Inventory and staffing shortages

Inflation

International shipping and flights

Positive Effects of Covid-19

Work Remote opportunity: Work-Life Balance

Here are some interesting work-from-home statistics according to Pew Research Center.

Around 20% of American employees regularly worked remotely BEFORE the COVID-19 outbreaks.

Around 71% of Americans work remotely or most of the time AFTER the COVID-19 outbreaks.

Around 54% of American employees want to keep working remotely after COVID-19.

Both my wife and I started to work from home after the COVID-19 pandemic broke out. My wife works from home, and I am on a hybrid schedule where I work in the office Monday-Friday but can work from home on Thursday and Friday.

Being able to work remotely has benefited us in many ways. It has given us an excellent work-life balance and made our life happier and more enjoyable.

During COVID-19 breakout, my wife was pregnant with our first son. Many changes and uncomfortable times accompany pregnant women (hats off to all the to-be mothers out there).

One big change was how my wife became hungry almost all the time. Working remotely allowed her to be in a more comfortable environment where she had easier access to food. 🙂

Our baby boy was born during the pandemic and working from home allowed us greater flexibility when caring for his needs. I could also help more around the home while my wife was recovering.

Other benefits include saving resources such as time and money. We didn’t need much time driving to work and getting stuck in traffic. Because of that, we can enjoy a nice breakfast together and help cook a yummy dinner.

We have saved a lot of money that would have otherwise been used on filling up gas. We also spend less money on buying professional clothes, don’t you feel nice wearing your pajamas when you work from home? LOL

Investing opportunity (stock market and real estate )

1. Stock Market

“Fearful when others are greedy, and greedy when others are fearful.”

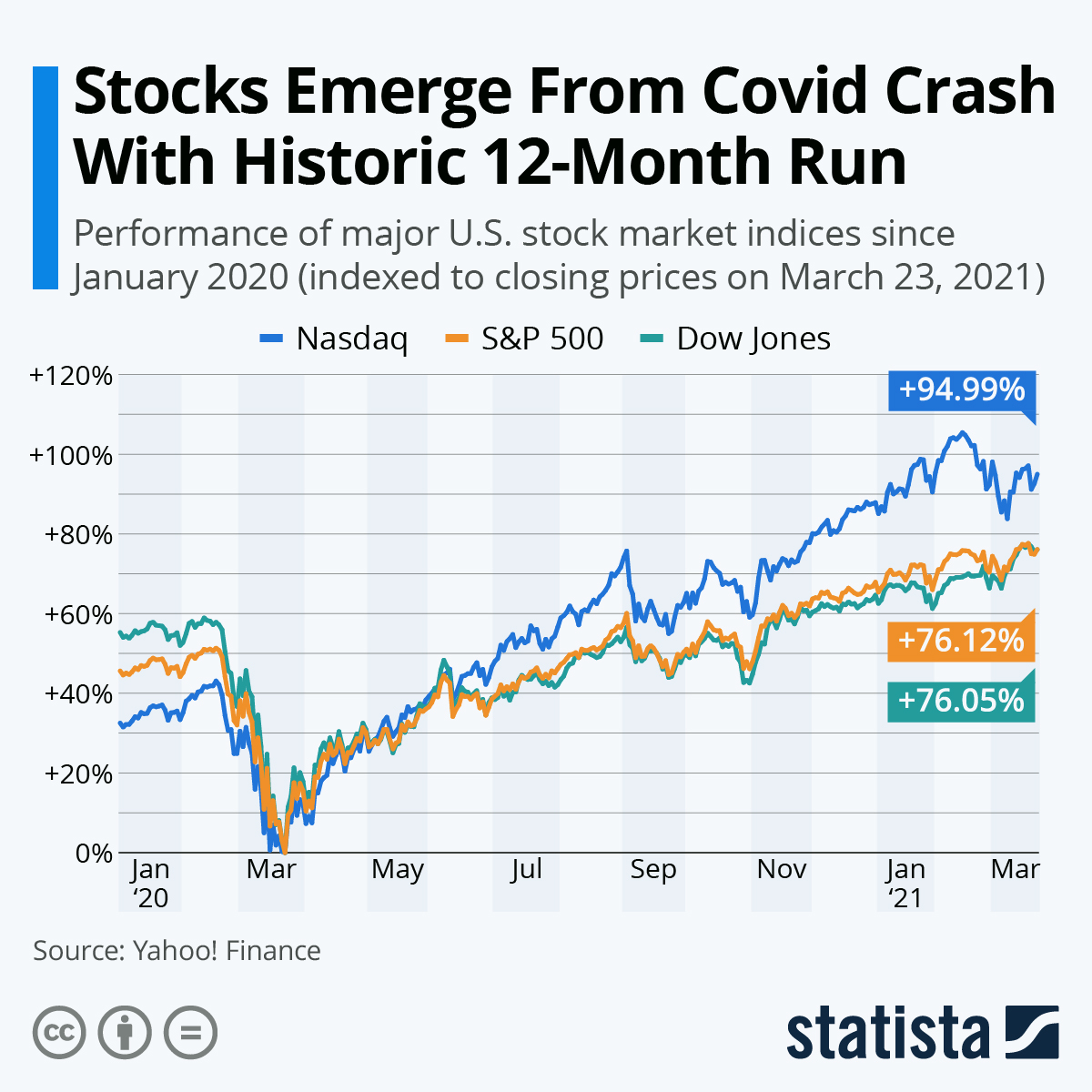

The COVID-19 pandemic led to a crazy 2020 stock market dip. The S&P 500 dropped to 66% from its peak by March 2020 and has rebounded 76% since its lowest point in the pandemic crash one year later.

Many people were scared about the crazy Covid-19 dip in the stock market, but my wife and I thought it was an excellent investment opportunity. See the chart above to see how our choice was a good one.

Regarding funds, we love the Total Stock Market Fund and S&P 500. If you don’t know what to invest in, they both can be a good starting point!

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

Gambling can become a scary addiction. We recently know how cryptocurrency, Game Stop stock, and other things have been high rewards but extremely high risks.

For us, this type of investing is more like gambling. Someone with extra money could invest in these things but must be willing to lose it all.

90% of our stock market investments are in a regular mutual fund, index fund, or ETF. 9% of our investments are in single stocks. Less than 1% is in cryptocurrency.

2. Real Estate

When COVID-19 happened, the interest rates for home mortgages dropped significantly. Many people started to purchase real estate or refinance their homes. We noticed these amazing interest rates and decided to refinance our 2nd property!

First, let’s talk about our refinance experience. We felt so blessed after finishing the refinancing process, knowing it would be worth it in the long run.

Our interest rate dropped from around 5% to 3%, down two percent! Our monthly mortgage payment used to be approximately $1200 but went down to around $1000 (with HOA fees), saving us around $200 a month!

We paid nothing at closing. The refinance closing costs were added to our loan, and our total loan amount became about $161,000. Below is a chart to put sum things up.

We decided to build a brand-new house nearby my parents’ place in July 2020. The building process was very interesting and took about ten months to finish.

We officially closed on the house in May 2021!

Initially, we were not planning to buy our 3rd property anytime soon in Utah. The plan was to wait until I graduated with my MBA first.

We started looking around for fun at different builders, and one builder’s sales agent wrote down our contact information. Within one week, he told us new lots were being released soon.

Since the location was close to my parents’ house, only a 3-minute drive away, we decided to go and look but still just for fun.

Two days later the agent told us their builder decided to increase all new homes by $5,000 (which will happen shortly). Any contract signed before that will keep the price and not be increased.

This news made us go under contract because we knew if we kept following our original plans, the house would become more and more expensive.

It turned out we were right, and our house increased in value by about $100,000 within a year, no kidding! That’s why real estate is impressive, and anyone can start now.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

In my previous post, “How I Graduated Debt Free with one kid,” I explained how we saved up and paid for my MBA tuition. I still needed to pay off the student loans left from my bachelor’s degree.

We used the debt snow method to do this. We listed out all the outstanding balances and then paid them off from small to big, ignoring the interest rate.

Using this method gave us much motivation and a positive feeling whenever we paid off a loan balance!

Also, during that time frame, the COVID student loan relief plan was put in place where the interest rate was zero during a specific period.

The relief plan allowed us to save a lot of money that would have been spent on interest.

Better habits, less sickness

We both feel like we have better habits due to COIVD-19, like washing our hands more often.

For example, using hand sanitizer after going to the store or other public places. I think it is good and protects our kids and us from not just covid but also other sicknesses.

Negative Effects of Covid-19

Inventory and staffing shortage

Shortages seemed to be happening everywhere in stores. Many grocery stores started limiting how many items you could buy, especially for items like paper towels, water bottles, oil, rice, and more! Even now, the inventory shortage still hasn’t been fully resolved but it is getting better.

The inventory shortage is super-inconvenient, especially when we need something.

A phenomenon that happened recently is the staffing shortage. After COVID-19, many people lost their jobs, but right now, most everywhere is hiring but still are having difficulty finding employees.

This staffing shortage causes us to wait longer to get food, and employees are overworked and exhausted. We even saw some restaurants sign saying, “please be patient with our employees; they chose to work today and serve you.” One of our favorite authentic Chinese restaurants closed because of these issues.

We hope both the inventory and employee shortage problems can be resolved soon. No matter what, we should be understanding and patient with workers. They are trying their best to help us out.

Simply put, Inflation is a consistent increase in the price of goods and services in our economy.

How does inflation affect our daily lives?

Your standard of living is mainly based on two factors: your income and expenses. Inflation will reduce the purchasing power of income while increasing daily expenses, harming your living standard.

Because your income does not increase or only increases a little and your expenses suddenly increase. This creates a significant negative impact on life.

Our family expenses increased by at least $100 monthly for our cost of living. I currently have a little Toyota corolla, and this car model has incredible gas mileage. In the past, the cost to fill up the entire tank was $25, but now it’s $45!!

I am still shocked to see how much it costs me each time I fill up. Not just gas, but when you go to a grocery store, you can tell the price of food and many other items have increased significantly.

Although many factors go into inflation, two leading causes of this surge are the sudden increase in spending/demand and low-interest rates FORBES.

International shipping and flights

My wife is from China, so sometimes she will buy something from China or my parents-in-law will ship some gifts to us. Whenever we want to ship something from China, the international shipping costs are more expensive each time.

The international shipping cost has increased, and the timeliness has also become slower, especially for shipping by boat.

here are more than a hundred loaded freighters anchored off the coast. Recently President Joe Biden announced a deal to have the Los Angles Port Open 24/7 to help solve the logjam of ships waiting to unload.

Another problem is with international flights! It is so hard to fly internationally, and flight tickets are so expensive to go to China or some other countries due to the COVID-19 restrictions.

My parents-in-law are located in China and planned to come to the USA to help us with our first baby. My wife is their only child, so our son is their first and only grandkid. It is so sad they still have not been able to come over and see their daughter and grandson.

My wife is pregnant now, and our daughter’s due date will be around February 2022. Looks like they won’t be able to come too. My wife misses her parents a lot, and it is very hard when parents are not there when something big and new happens in your life.

I hope one day everything will be back to more normal circumstances, and my wife can see her family, and my parents-in-law can meet their grandkids.

Best wishes to those individuals and families who have a similar situation to us. I hope you can also see your family as soon as possible!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

An IRA is a fantastic tax advantage retirement saving and investing tool. When you open an IRA (Individual Retirement Account), you will face two choices: Roth IRA or Traditional IRA.

This post may contain affiliate links, please see our disclaimer for details.

We come from different walks of life and are in different financial situations. It’s essential to know the differences between both Roth IRAs and Traditional IRAs before choosing one (or both)!

My wife and I chose the Roth IRA because we don’t want to worry about tax when we retire. The thought of being a tax-free millionaire in the future is exciting.

The deadline to max out an IRA each year is typically the same as the filing tax return deadline –April 15.

For example, you can still contribute to your 2021 IRA up until April 15, 2022.

Both the Roth and Traditional IRAs provide generous tax breaks. But which one should you choose?

In this article, I will discuss the 5 key differences between Roth and Traditional IRAs. We hope this information can help you make a more informed choice. 🙂

YouTube Video Going Over The Topic

The 5 Key Differences between Roth and Traditional:

Tax Benefits

Limited Income

Withdrawals

Early-withdrawal penalties

Distribution Rules (RMDs)

1. Tax Benefits

Both Roth and Traditional IRAs provide generous tax breaks. If you expect to be in a higher tax bracket when you retire or retire without needing to worry about tax, the Roth IRA will probably be better suited for you.

But if you expect to be in the same or lower tax bracket when you retire, then Traditional IRA probably will be a better suit for you. Why? See below:

Roth IRA: You can make an after-tax contribution and the money will grow tax-free.

Traditional IRA: You can make pre-tax contributions if you meet income eligibility (check below for point 2 – limited income). Your contribution growth will be tax-deferred.

2. Limited Income

The 2020 and 2021 contributions limit for Roth and traditional IRAs is $6,000 or $7,000 if you’re age 50 and older. You must have enough earned income to cover the contribution.

For Example: If you only made $1000 in 2020, you can only contribute up to $1000 to your IRA in 2020.

Roth IRA: In 2022, the annual income limit is $144,000 for single and $214,000 for married filing jointly. This means if you are above that income, you will not be able to contribute to the IRA.

Traditional IRA: There are specific income (AGI, adjusted gross income) limits that impact much you can contribute in pre-tax dollars. This is divided into two situations: you have a retirement plan at work, or you DON’T have a retirement plan at work.

Roth IRA: Earnings from a Roth IRA can be withdrawn tax-free and penalty-free when you are 59½, and the Roth IRA must have been open for at least five years. However, withdrawals of your contributions can be taken out at any time without a penalty.

Traditional IRA: Earning withdrawals can happen penalty-free after age 59½ but will be taxed at your income tax rate. Contribution withdrawals after 59½ are also subject to tax unless you’ve made nondeductible contributions; in that case, only part of your withdrawal will be tax-free.

4. Early-withdrawal penalty

For both Roth and Traditional IRAs, If you withdraw money before age 59½, you might have to pay taxes on your earnings, plus a 10% early withdrawal penalty.

4. Distribution Rules (RMDs)

Roth IRA: You are not required to withdraw any minimum money at any age.

Traditional IRA: Generally, you will be required to make a taxable withdrawal for a minimum amount of money at age 72.

Traditions Vs. Roth IRA: Conclusion

The Roth IRA and Traditional IRA are excellent tax advantage retirement accounts and will help in pursuing financial freedom.

Different people have different fiance situations. Make sure to understand the differences between Roth IRA and Traditional IRA before you make your own decision.

My wife holds her IRA at Vanguard and mine is with Fidelity. Both investment companies have been great to work with!

The most important thing is to start investing early and start now.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

Compound interest is the most beautiful thing in the world. You will see how miraculous it is and how it grows like crazy over time!

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

Albert Einstein

We’d love to hear which type of IRA you are interested in or using! Drop a comment in the box below. 🙂

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Getting out of debt and knowing how to deal with debt collectors is essential to gaining control over your finances. This article aims to help you successfully negotiate and deal with debt collectors.

Did you know that every 1 out of 3 US adults has a debt collection account(s)?

In this article, I share our story dealing with debt collectors including 4 tips to help you when dealing with debt collectors.

This post may contain affiliate links; please see our disclaimer for details.

My collection account came as a big surprise, it was from past college tuition that was never paid off.

I transferred to a new college in Hawaii and thought I had successfully received the student loan for the semester.

Turns out I was wrong.

One document needed to be signed before the tuition/loan could be dispersed, but I completely missed it.

Since the document wasn’t signed, I never received the student loan. Unfortunately, the entire amount was sent to collections.

After one semester of school in Hawaii, I transferred back to my school in Utah. One year later, I started getting calls from a debt collector.

They told me that I had a collection account because I didn’t pay my tuition.

Both my wife and I didn’t believe it at all and thought it was a scam at first. We thought there was no way I didn’t pay my tuition, so we just ignored it.

Our Story Continued…

We discovered the collection account was real when applying for our second property loan. It turns out it was not a scam, hurting my credit score!

Fortunately, my wife’s credit score was still excellent, so our combined score wasn’t too bad. My wife’s credit score was terrific. Together our score was still around 700.

Unfortunately, we could still not get the best interest rate for our second property loan. The interest rate on the mortgage ended up being almost 5%, ouch!

We learned a valuable lesson and became much more aware and careful of our credit scores.

We started saving like crazy after we closed on the loan. Our total debt collection account was $6,000, but we successfully negotiated with the debt collector.

For the final settlement, we only needed to pay $3,500 in total as a one-time payment. After paying, the collection account would be removed entirely from our credit history.

Our credit score shot up a lot after that, YES!

Now let’s look at the reasons for how we successfully dealt with debt collectors.

How to Successfully Deal with Debt Collectors

1. Verify Your Debt, Avoid Scams!

First, you must ensure the collection account is yours, including all information regarding the debt. There are real scammers out there trying to collect personal information.

Don’t give away your trust or your personally identifiable information too easily. Remember it is best to be careful.

We requested the debt collector send us everything in writing through the mail. We also called my school in Hawaii to verify the debt account was real.

Don’t just negotiate regarding your monthly payments or lower your total debt. Request they remove the collection account from your credit account/history.

Removing the lousy credit account from your credit score sooner will be well worth it.

After finding out the total collection amount was around $6000, we calculated our monthly budget to see how much we could afford for a monthly payment.

We worked hard to save up a big lump sum of money to pay off the account with a one-time payment, even though it was less than the collector was asking for.

We talked with the debt collector, and they agreed on a very minimal amount for the monthly payment plan.

You can always explain your financial situation to the debt collectors. It’s okay to say you don’t have much money or cash flow and propose the only amount that works for you.

Saving Up Money & Negotiating to Pay Off With One Lump Sum

After that phone call, we worked our butts off and saved $3,500!

We felt we could try to negotiate again with the debt collectors by proposing to pay off all debt with a lump sum of money.

We didn’t think our negotiations would be successful because it was almost half of our original collection amount, from $6,000 to $3,500. It never hurts to try!

We called our debt collector and discussed what was possible if we made a one-time payment. Next, we requested debt account be removed from my credit report.

The debt collector listened as we explained we didn’t have a lot of money and worked our butts off to save this $3,500. Having him agree to a one-time payment would help us a lot.

We also told him how the collection account happened and how we didn’t know if the collection account typically takes full responsibility for our bills.

As mentioned at the beginning of this post, it just happened by mistake.

The debt collectors told us he needed to talk with our original debt owner, my school back in Hawaii.

We told him to please tell my school our situation. We emphasized it would be a big blessing for our young family if they agreed to our plan.

Luckily just a few days later, we received a miracle call from the debt collector who told us my college agreed with the $3,500 settlement PLUS the collection account could be removed from my credit history!

We feel this is such a massive blessing that everything worked out great.

4. Have Everything In Writing.

After receiving the news of being able to make a one-time payment and have the account removed from our credit, we requested a settlement agreement showing we paid the total collection amount in full and that it would be removed from my credit history.

After the debt collector agreed to send over everything in writing, we made the one-time $3,500 payment.

My credit score shot up a few months later, and the collection account was gone!

In Conclusion

Life is a journey of learning lessons, and we have learned a lot about dealing with debt collectors. It’s important to learn quickly from mistakes and face life with an optimistic viewpoint.

Paraphrasing what Kevin Hart has said –

“It’s okay to make mistakes, we just need to learn how to fail better each time”

Due to this experience dealing with debt collectors, we have become more concerned about our credit scores.

Including more frequently checking our email and mail to see if there are any unpaid bills.

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you read How We Became Landlord At Age 22 As College Student, you will see that had a high and scary interest rate for our 2nd property/condo. The reason for this was that I had some surprising credit issues.

When COVID-19 happened, interest rates dropped significantly. Many people started to buy real estate and/or refinance their homes.

We noticed these fantastic interest rates and decided to refinance our condo! (We were also fortunate to buy and build our third property during the low-interest rate time).

Compelling advantages/reasons to refinance your home

Lower interest rate.

Pay off the home mortgage faster.

Get rid of home mortgage insurance (PMI).

Lower monthly payment.

Can take cash out to pay off high-interest debt, use for a new property down payment, etc.

Pay off loan faster (IE – change from a 30-year to 15-year term).

Switch from an adjustable mortgage rate to a fixed rate.

We chose to refinance primarily to obtain a lower interest rate, lower monthly payment, and wipe out mortgage insurance. We did not pull any cash out for our refinance.

I would like to share our refinance experience for our second property/condo. Side note: we refinanced while still living there, so it was our primary residence.

Our refinance process was easy! We shopped around and found three different lenders to give us a quote. Next, we would review and go with the best quote.

We highly recommend finding at least three different lenders to compare and negotiate with to get the best deal. One of the lenders told us, “ I would be willing to cut my commission to give you the best deal.”

After choosing the one we liked best, we started submitting documents. Below are the most common required documents when applying for a home loan or refinance.

Most common documents required for underwriting:

2-year tax returns

Pay stubs, W-2s, or other proof of income

Bank statements and other assets

All of your debt monthly payment history

Credit score, credit history

Gift letters (if someone helps you with down payment etc.)

Photo ID, SSN

Rent history if you are renting, mortgage/HOA history if you are a house owner

House insurance company if you have a preference, usually it will cheaper when you bundle with car insurance.

If you have tenants, include rent payment history & current lease agreement.

Back to our refinance process, the lender next sent out an appraiser to check our property and give an estimated value based on house conditions and the market.

Because the value of the home increased, we could avoid mortgage insurance when refinancing by having 20% equity in our condo.

We could have pulled out equity but decided to leave it all in there. Our mortgage insurance, or PMI, went from around 100 dollars to 0 dollars a month!

The interest rate dropped from around 5% to 3%, down 2%! Our monthly mortgage payment used to be approximately $1200 but went down to around $1000 (with HOA fees), saving us around $200 a month!

We paid nothing at closing. The refinance closing costs were added to our loan, and our total loan amount became about $161,000.

In Conclusion

Below is a chart to sum up our refinance experience with numbers.

Before Refinance

After Refinance

PMI

$100

$0

Interest Rate

5%

3%

Total Monthly Payment (with HOA)

$1,200

$1,000

Before and after refinancing our condo

We felt so blessed after finishing the refinancing process and know it will be worth it in the long run. Our next step was purchasing our third property and renting out our condo.

We leased it out for $1,300, giving us around $300 monthly in cash flow! Having that type of investment property has been an enormous blessing.

We hope that our refinance story can help you better understand the process a little better and the benefits that can arise by doing a refinance.

Feel free to share other benefits or stories you have doing a refinance in the comment box below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

The Squid Game TV show has recently become the number one television show on Netflix in over 90 countries! The hype made its way to us, and we ended up watching the entire series. While watching Squid Game, we realized there are many important lessons to be learned on personal finance.

This post may contain affiliate links; please see our disclaimer for details.

As for a rough summary of the TV show, a secret group of rich people invited 456 people to participate in a series of six deadly games.

Those selected had serious money problems and many other issues. The main character was in massive debt and could have used some personal finance wisdom!

Although the Squid Game story is fiction, we can all learn valuable lessons regarding debt and personal finance.

So let’s jump in!

YouTube Video Sharing The 6 Financial Lessons Learned from Squid Game

Here are the six key takeaways we would like to share with each of you.

Because when the next recession or stock market crash hits, there will be enough money in the emergency fund so that no money needs to be taken out of retirement investment accounts.

Instead, you will be able to wait until the stock market recovers. 🙂

My wife and I started our Emergency Fund and put it into a high-yield savings account to give us more peace of mind.

We recommend not putting your emergency fund into a high-yield savings account and NOT into the stock market since you will need quick access to the money.

A great place to get started with your savings account isCIT Bank. They offer very competitive saving rates with no monthly maintenance fees.

With their Saving Connect Account, you can earn 12x the national average! There are no ATM fees, and you have the convenience of online banking.

“ Every time you borrow money, you’re robbing your future self” –

Nathan Morris

An important financial lesson from the Squid Game show is to stay away from bad debt! Which to us means debt doesn’t make you money, don’t hold onto it.

We can proudly say: We are completely debt-free except for the mortgage. We feel the freedom! It’s so good for our mental health and relationship!

We are not trying to boast but want to share our process and hope everyone can feel the freedom that comes from becoming debt-free.

3. Live the Budget Life (it’s worth it)

Buying things in cash is worth it, even though it takes patience and time to save up the needed cash.

Make sure to know if the thing you are thinking about buying is truly a ‘need’ or just a ‘want’. Give yourself time to think it over or cool down before purchasing.

It’s also okay to use a credit card, but make sure to pay it off immediately.

Instead of eating out a lot, my wife and I would cook at home. We would meal plan for the week and put any leftovers in the freezer. Doing this is convenient, especially when you’re constantly on the go.

We buy a lot of things second-hand and save a lot of money by not buying something brand new.

There are many free things through the Facebook marketplace, such as baby items, household items, etc.!

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

4. Have Health Insurance

In the squid game series, the main character made a huge mistake- he canceled his mom’s health insurance plan. In the USA, hospital bills can be very expensive.

If we didn’t have health insurance, then the delivery cost for our baby would have been $12,000 out of pocket. If there would have been complications or other issues, then that bill would have been higher.

Health insurance is a big blessing for us; we cannot imagine without it!

5. Invest Smart, Avoid Gambling

In one of the Squid Game episodes, one guy taught the lesson to “don’t put all your eggs in one basket.” We agree! We need to invest more and invest more wisely.

Regarding funds, we love the Total Market Fund and S&P 500 fund. If you don’t know what to invest in, they both can be a good starting point!

Gambling can become a scary addiction. We know recently how cryptocurrency, Game Stop stock, and other things have been crazy.

For us, it is more like gambling. Someone with much extra money could invest in these things but must be willing to lose it all.

90% of our stock market investments are in a regular mutual fund, index fund, or ETF. 9% of our investments are in single stocks. Less than 1% is in cryptocurrency.

6. Spend Quality Time With Your Family.

We know how life can get busy. We need to work and make money for family needs. No matter how busy life gets, it’s important to remember FAMILY TIME.

Time needs to be spent building important relationships with family.

We enjoy going on dates and spending time with our little kiddo away from work and distractions. Relationships are the spice of life!

When I was doing work and school full time, my schedule was pretty crazy, but I always did my homework after my baby was sleeping because I wanted to help my wife and spend time with our baby.

I don’t want to miss any special moments of fatherhood and raising a kid.

For a recap, below are six finance and life lessons we took away from the squid game series.

Save up an emergency fund

Get off of debt fast

Live the budget life

Have health insurance

Invest smart: avoid gambling (don’t put one egg in one basket)

Spend quality time with your family

Thanks for reading! We’d love to hear your thoughts on the tv series and personal finance lessons; drop a comment below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.