Are you considering the idea of quitting your job?

You’ve probably heard of the great resignation by now. Many people are looking to leave their current workplace to find more flexible employment, pursue working for themselves, or retire early.

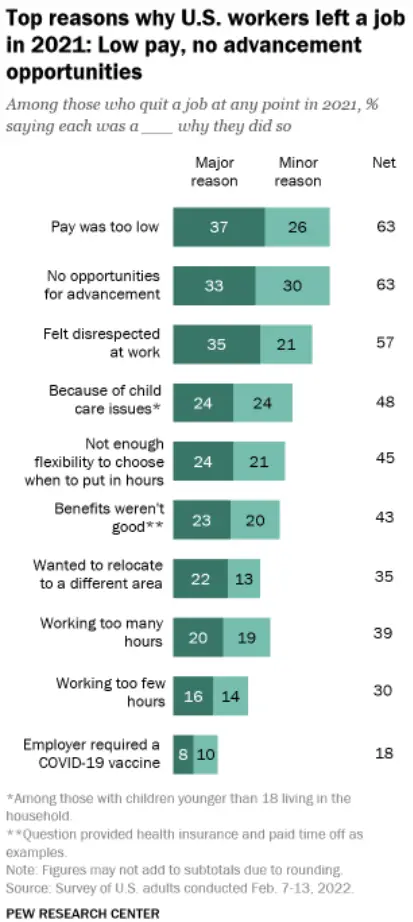

Here are the reasons for the great resignation, according to Pew Research Center:

“Majorities of workers who quit a job in 2021 say low pay (63%), no opportunities for advancement (63%), and feeling disrespected at work (57%) were reasons why they quit, according to the Feb. 7-13 survey. At least a third say each of these were major reasons why they left.”

Roughly half say childcare issues were a reason they quit a job (48% among those with a child younger than 18 in the household).

A similar share point to a lack of flexibility to choose when they put in their hours (45%) or not having good benefits such as health insurance and paid time off (43%). Roughly a quarter say each of these was a major reason”.

It’s crucial to make sure that you do everything possible to prepare for the transition of quitting your job.

Quitting a job can be scary, but if you plan ahead and take the time to do things correctly, it can be a much smoother process.

This article will discuss fourteen things you must do before quitting your job.

By following these tips, you’ll be able to make the transition as smooth as possible!

This post may contain affiliate links; please see our disclaimer for details.

The Benefits of a Smooth Departure

When you leave a job on good terms, it can benefit you in several ways.

For one, getting a positive reference from your former employer will be much easier.

Additionally, if you ever need to return to that company later down the road, they will be more likely to welcome you back with open arms.

Finally, quitting your job on good terms is simply the right thing to do – it’s respectful and professional.

What Should You do Before Quitting Your Job

There are a few key things you should do before quitting your job. Make sure you do these if you wish to leave on good terms. He

Buckle up because here are fourteen things you should do before you quit your job:

1) Give Enough Time Notice

One of the most important things you can do before quitting your job is to give your employer two weeks’ notice. Although this is standard protocol, giving your employer time to find a replacement for you.

Additionally, by giving two weeks’ notice, you’re showing that you respect your employer and the company.

They will be much more likely to give you a positive reference if you give them this courtesy.

Schedule a meeting with your boss to deliver the news in person.

This way, they can ask any questions, and you can explain your decision further.

Giving two weeks’ notice is one of the most important things you can do when quitting your job – make sure not to forget it!

2) Clean Up Your Work Area

Another thing you should do before leaving is to clean out your desk.

Doing so shows that you respect your employer and their property and makes the transition easier for your successor.

Plus, once you’ve cleaned your desk, you won’t have to worry about returning to retrieve any personal belongings – they’ll all be gone!

To clean your desk, start by going through all your drawers and removing any personal items.

Next, review your files and remove anything specific to you or your work. Finally, wipe down your surfaces and vacuum the floor around your desk.

By taking the time to clean out your desk before quitting, you’re making things much easier for everyone involved.

3) Tie Up Loose Ends

Before quitting your job, you should also take the time to tie up loose ends.

Make sure to finish any projects you’re working on, wrap up any open tasks, and ensure that everything is organized and in its proper place.

Tying up loose ends before you leave shows your employer that you’re a responsible and reliable employee. Additionally, it will make the transition smoother for whoever takes over your role.

So take time to finish up anything incomplete – it will benefit everyone involved!

4) Train a Backup or Replacement

If possible, you should also try to train your replacement before leaving your job.

This is a great way to show that you’re committed to the company and want to see it succeed – even after you’re gone.

Training your replacement can be as simple as showing them how to do your job, answering any questions they may have, and providing helpful feedback.

Of course, not everyone will be able to train their replacement, but if you can, it’s worth doing!

5) Save For a Rainy Day

Before quitting your job, you should also save up some money.

This way, you’ll have a cushion in case you need it – whether for unexpected expenses or to tide you over.

Most experts recommend saving up to three to six months’ worth of living expenses, but depending on your situation, you may want to save more.

Ideally, it would help if you aimed to save enough money to cover your living expenses for at least three months. This may seem like a lot, but it’s better to be safe than sorry!

Another important thing to do before quitting your job is to create at least one source of passive income. This will help you keep financial stability even when you’re not working a traditional job.

There are many ways to create passive income, but some of the most popular methods include investing in real estate or stocks.

You can even create a passive income source such as a blog, youtube channel, or online business.

Creating a source of passive income is a great way to prepare for quitting your job – it’ll help ensure that you’re still able to support yourself financially even when you’re not working!

If you are transitioning to another job, having a source of passive income can still be a helpful safety net.

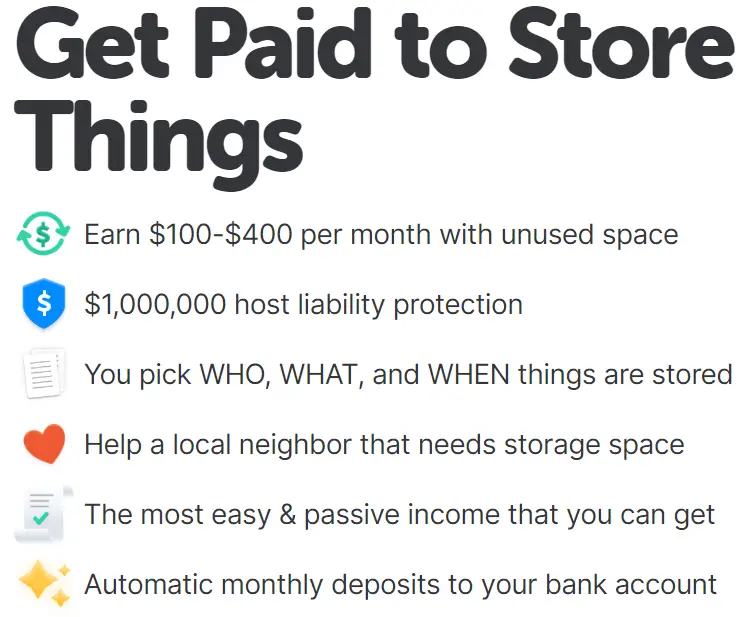

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

7) Have a Plan B

In addition to saving money and creating a source of passive income, you should also have a Plan B in case quitting your job doesn’t work out.

Your Plan B could be anything from finding another job to moving in with family or friends. The important thing is that you have a backup plan in case things don’t go as planned!

Having a Plan B is always a good idea – you never know what might happen, so it’s better to be prepared!

When we quit

8) Continue Your Relationship with Co-Workers

Just because you’re quitting your job doesn’t mean you have to say goodbye to your co-workers!

If you have a good relationship with them, there’s no reason why you can’t stay in touch after you leave the company.

You can stay in touch with your co-workers by connecting on social media, meeting up for coffee or lunch, or simply sending them an email now and then.

Staying in touch with your co-workers is a great way to maintain relationships and keep networking – even after you’ve left your job!

If you are quitting your job to enter a new career that provides a stable income, this is the time to pay off your debts.

By doing so, you can start your next adventure with a clean slate and without the stress of debt hanging over your head.

If you are quitting your job to pursue a more risky career with an unstable income, it is even more important to get out of debt before making the switch.

This will provide a safety net if your new career doesn’t work out as planned.

No matter your reason for quitting your job, it’s always a good idea to get out of debt before making the switch.

Then you can ensure the start of your new chapter in life happens on the right foot!

There are a few different ways to pay off debt, but the most important thing is to make a plan and stick to it!

You can also talk to a financial advisor to help create a debt payoff plan.

10) Have Life Insurance Figured Out

When it comes to life insurance, there are two main types: term and whole life.

The main difference between whole life and term life insurance is that whole life insurance provides lifelong coverage. In contrast, term life insurance only covers you for a specific period.

Make sure to have life insurance figured out before quitting your job.

Don’t forget to keep investing in your tax-advantaged retirement accounts to prepare for a long & happy retirement.

NerdWallet explains there are “five main choices for the self-employed or small-business owners: an IRA (traditional or Roth), a Solo 401(k), a SEP IRA, a SIMPLE IRA or a defined benefit plan”.

Make sure to look through each option and find which choice works best for you.

The Bottom Line

That’s it! These are the fourteen things you should do before quitting your job.

Following these steps ensures that leaving your job goes as smoothly and stress-free as possible.

Quitting your job can be a big decision, but it doesn’t have to be the world’s end.

If you take the time to prepare for it properly, you can set yourself up for success – even after you’re gone.

So if you’re thinking about quitting your job, be sure to keep these things in mind!

Disclaimer:

We hope the information shared in this post provides valuable insights to every reader but we are not financial advisors. When making your personal finance decisions, we recommend researching multiple sources and/or receiving advice from a licensed professional.

There are many investment options to choose from when it comes to making money. Two of the most popular choices are real estate and stocks.

Investing in the real estate market and investing in the stock market both have pros and cons, and it cannot be easy to decide which option is best for you.

In this article, we will compare and contrast real estate and stocks so that you can make an informed decision about the right investment for you!

Many may feel overwhelmed when deciding between stocks and real estate, as these two asset classes can differ.

However, some key similarities between the two should be taken into account. They are similar as they both have the potential for asset appreciation and passive cash flow.

Both real estate and stocks share similar investing principles, such as the time-tested adage “buy low and sell high.”

In other words, to make profits in either asset class, you must purchase an investment when prices are low and then sell when prices have increased.

Of course, there are also key differences between real estate and stocks that should be considered.

One major difference is the level of liquidity.

Stocks are much more liquid than real estate, meaning they can be sold quickly and with less hassle.

It’s important to consider this if you need to access your money quickly or if you are worried about being able to sell your investment promptly.

Another key difference is the level of risk involved.

Real estate is generally considered a more stable investment, while investing in individual stocks can be more volatile. Real estate may be a better option if you are risk-averse, while single stocks may be more suited for those comfortable with taking on a higher level of risk.

Now that we have explored some basic similarities and differences between the two asset classes, let’s go into more detail about the returns you can expect from each.

This post may contain affiliate links; please see our disclaimer for details.

Returns: Real Estate vs. Stocks

One of the most important things to consider is the returns you can expect from each investment.

Regarding real estate, the average return is around 9-12%. This number can fluctuate depending on various factors, such as location and the type of property you invest in.

However, over the long term, real estate has proven to be a relatively stable investment and can be a considerably higher return on investment.

When it comes to stocks, the average return is around 12%. Again, this number can fluctuate depending on various factors, such as the company you invest in and the overall market conditions.

However, stocks have the potential to generate higher returns, but they are also more volatile.

Real estate can generally yield higher rents than dividends from stocks. Real estate can be a great option if you are looking for income investments.

With that said, stocks have the potential for compounded capital appreciation, which can lead to higher returns in the long run.

Investing in real estate or stocks comes with its risks. With real estate, one of the biggest risks is the potential for a decrease in property values.

This can happen for various reasons, such as a recession or changes in the local market.

Another risk to consider is the possibility of vacancies, which can lead to a loss of income.

You can interview your tenants, but you can never be sure they will stay long.

Regarding stocks, one of the biggest risks is the potential for losses due to market volatility.

The value of your investments can go up and down rapidly, leading to losses if you are not careful.

Another risk to consider is the possibility of fraud or mismanagement by the company you invest in. This can lead to a loss of your investment entirely.

There are ways to lower the risks of each investment type. Some ways to do this are by diversifying your portfolio, investing in quality assets, and working with experienced professionals.

Let’s explore some more ways to lower your risks.

Ways To Lower Your Risks When Investing

By keeping these investment principles in mind, you can lower the risks whether you want to become an investor in the stock markets or real estate.

Diversify: Don’t put all your eggs in one basket. This is key in any investment, whether buying stocks, picking a mutual fund, or investing in real estate.

Have a long-term outlook: Don’t get caught up in the market’s day-to-day fluctuations.

Be patient: Don’t expect to get rich quickly. Investments take time to grow.

Know your risks: don’t invest in something you don’t understand. Make sure you know the risks involved before you invest your hard-earned money.

Know the law: Some certain rules and regulations apply to different investments. Make sure you understand the laws before you make any decisions. By having insurance with a good law team, you can be sure you are covered in case any legal issues should arise.

Keep emotions out of it: Don’t let your emotions guide your investment decisions. This can be not easy, but it’s important to remember that investments are based on numbers, not feelings.

Do not over-leverage yourself: Don’t borrow too much money to finance your investments. This can lead to financial ruin if things go wrong.

Start small: Don’t go all-in on your first investment. Start small and gradually increase your investment over time.

Work with experienced professionals: Get help from those who know what they’re doing. This is especially important if you’re new to investing.

By following these principles, you can minimize your risk and maximize your chances for success, no matter your investment type.

Now that we have explored the risks and rewards of real estate and stocks let’s look at each investment’s pros and cons.

Pros and Cons: Real Estate

One of the biggest advantages of real estate is that it is a physical asset.

You can see and touch your investment, which can give you a sense of security.

Another advantage is the potential for high returns. As we mentioned earlier, real estate has the potential to generate higher income returns than stocks, although it is also riskier.

Real estate debt. It can be seen as a risk by some people. Others will perceive real estate as a great investment method without using much of your own money.

This is because you can often use leverage to purchase property, which means you can control a much larger asset for a smaller investment.

Real estate can also offer tax benefits. For example, you can deduct the interest you pay on your mortgage from your taxes.

You can also depreciate the value of your property, which can lead to significant tax savings.

The biggest disadvantage of real estate is the fact that it is illiquid. It can take longer to sell your property, and you may not be able to get your money out as quickly as you would like.

Another disadvantage is that maintaining and repairing your property can be expensive, which can affect your profits.

The most troublesome disadvantage of real estate is bad tenants. As a landlord, you may experience mistreatment of your property or be sued for eviction.

You may also have to deal with damage to your property that tenants cause. A solid screening process can help minimize the risk of bad tenants.

Pros and Cons: Stocks

One of the biggest advantages of stocks is that they are liquid, which means you can sell them relatively quickly if you need to.

Another advantage is the potential for high returns. As we mentioned earlier, stocks have the potential to generate higher compounded returns than real estate, although they are also riskier.

The biggest disadvantage of stocks is the fact that they are volatile. Their value can go up and down rapidly, leading to losses if you are not careful.

You may also experience negative tax consequences, such as capital gains taxes, if you sell your stocks for a profit.

If you plan to trade frequently, it’s important to consider this. To become a long-term investor, consider investing in tax-friendly accounts such as an IRA.

Another disadvantage of stocks is that they require ongoing maintenance. For example, you may need to pay fees to a financial advisor to help you manage your portfolio.

If you plan on picking stock individually on your own, it can be time-consuming and stressful. However, these disadvantages can be negated by investing in stocks through ETFs.

Another disadvantage is the possibility of price manipulation by whale investors. This is when a small group of investors buys or sells a large number of shares, which can cause the price to go up or down.

The most troublesome disadvantage of stocks is the potential for fraud. This can happen if a company misleads investors about its financial situation or commits accounting fraud, which can lead to losses for investors.

Stocks vs. Real Estate: Which is right for you?

Both real estate and stocks have the potential to generate high returns and create wealth over time.

However, they each come with their own set of risks and disadvantages.

So, which is the right investment for you?

The answer to this question depends on your circumstances. For example, stocks may be a better option than real estate if you are looking for an investment that you can sell quickly.

On the other hand, if you are looking for a more stable investment that offers tax benefits, then real estate may be a better option.

If you only have a few thousand dollars to invest, it may be better to invest in the stock market as a down payment for a house may require more than what you have.

As your income increases, it wouldn’t hurt to compound small amounts in the markets. During this period, you should also ensure that your credit score is in good standing, as this will be a factor when you’re ready to purchase the property.

Once your income has increased and you can save money faster, you can consider looking into investment properties or following a similar strategy to us where we buy a residential property, fix the property up, rent it out, then refinance.

If you don’t want to own real estate yourself but still want exposure to the real estate market, try investing in REITs or with property crowdfunding. These investments require a lower barrier of entry, but you will not receive the same tax benefits of leverage potential as if you owned the property.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

No matter what route you decide to take, remember that you are on the right track for wanting to learn about these two investment assets.

Before making a decision, remember your investment goals, risk tolerance, and time horizon.

Real estate may be a better option if you want an investment that will generate passive income through rental properties. But stocks may be a better choice if you want an investment that will appreciate without much maintenance.

You may want to consider both options and hold both long-term.

As someone that is thinking about their financial future, you are already ahead of most people!

Sometimes we can become biased toward one option or the other. It is important to remember that you should diversify your portfolio and not put all of your eggs in one basket.

Doing this can minimize your risk and maximize your potential for returns.

The bottom line is that there is no right or wrong answer regarding real estate vs. stocks.

The answer depends on your individual circumstances and investment goals. So, take the time to research and make an informed decision about which option is right for you.

In pursuing financial freedom, never forget that you can benefit from both asset classes.

Real Estate vs. Stocks: Which is the Better Investment?

So, which is the better investment? Real estate or stocks? The answer depends on your circumstances.

Real estate may be a better choice if you are looking for stability. However, stocks may be a better option if you are looking for quick, high returns.

Ultimately, the best decision is to diversify your investment portfolio and not put all of your eggs in one basket. Also, consider index funds or ETFs that allow you to invest in hundreds of companies at once. This way, you can minimize your risk and maximize your potential for returns.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

We should all be familiar with personal finance and financial literacy. Managing your money efficiently becomes very difficult without proper knowledge of personal finance, and overspending becomes easier.

There are many things to be aware of and practice regarding personal finance. Retirement planning, investing, budgeting, insurance planning… and so on.

Becoming a financially literate person cannot happen overnight! It takes years of practice and continuous learning to become an expert in financial management.

What better way to learn these essential skills than to read the best personal finance books!

In this article, I will share the top 5 personal finance books you should read in 2022. By reading these books, my knowledge of personal finance and financial literacy has been elevated to a new level.

Rich Dad Poor Dad – Robert Kiyosaki

Total Money Makeover – Dave Ramsey

The Simple Path to Wealth – JL Collins

Why Didn’t They Teach Me This In School? – Cary Siegel

The intelligent investor – Benjamin Graham

What Will You Learn From These Books?

The books in this article are written by some of the world’s top financial experts, businessmen, and investors. They are simple with concepts that are easy to comprehend. You will learn about the following –

1. How to manage your money: Including the rules of money management. You will know how to use your credit card correctly, the difference between an asset and a liability, when to buy or when to sell, etc.

2. How saving and investing work: Most people don’t know this but saving and investing are somewhat related. You will also learn about the different types of investments and other important concepts.

3. Tips and tricks: These books offer money-saving and making techniques and certain hacks to help you save more and spend less!

4. How to make your money work for you: This is the part where you will learn about the difference between passive and active income, how compound interest works, mutual funds, etc. You will also know what financial independence means and how it can help you retire earlier than everyone else!

5. Retirement planning: You will learn about retirement planning, including why you should invest for your future, choosing the best mutual funds, and how much money you need to retire.

Why Read These Top 5 Personal Finance Books?

First, they are written by some of the best financial experts in the world with real-world experience. Also, they appeal to people of different ages and backgrounds, regardless of whether you’re 18 or 60 years old.

You can be a college student or someone who just entered your first job… These books will still teach you all the essentials of personal finance!

If you want to learn more about personal finance and how to become financially literate, then definitely read these books!

So now let’s begin with the top 5 personal finance books that you should read in 2022!

1. Rich Dad Poor Dad – Robert Kiyosaki

The first book on our list is not a usual finance book. It was written by Robert Kiyosaki and it is about personal finance from a rich dad and poor dad’s perspective.

It teaches the difference between the two dads’ financial literacy and how it affects them even today!

What Will You Learn?

There are multiple ways to make money, not only by working a job.

There are clear differences between assets and liabilities. You’ll learn methods to becoming financially free by investing your money in assets instead of liabilities.

You will understand the types of investments that are necessary to becoming rich. You’ll also learn to assess risk and fix your finances by hearing personal stories!

2. Total Money Makeover – Dave Ramsey

The next book on our list is not a usual finance book as well. This money-saving and making guide will teach you the basics of saving, spending less, and avoiding debt!

The book also talks about many surprising money facts about American culture and how people of America view money. The main goal of this book is to teach about making sacrifices now and living a frugal life to secure your future and be financially stable!

What Will You Learn?

You will learn what true wealth is and why it’s more important than the number in your bank account. You’ll also learn how you can take control of your financial life.

Moreover, you will discover money-saving tricks inspired by the author’s personal story about becoming financially independent!

This book also touches on the basics of investments like mutual funds and stocks, so you can learn more about them! Dave Ramsey also writes about 7 baby steps to help people get out of debt and build real wealth!

3. The Simple Path to Wealth – JL Collins

JL Collins covers all the basics of personal finance, such as how to get rid of bad debt and keep investments simple. This book is ideal for people who want to start investing and learn how to grow their money.

It is a great starting point for people who want to know the basics of wealth management. The book also talks about different types of investment vehicles and how they can help you in your journey to financial independence!

What Will You Learn?

You will learn the power of long-term investments and how to utilize every opportunity that comes your way! The path to wealth doesn’t have to be complicated, and JL Collins does a great job of making investing an easy journey.

The author uses their experience to teach different types of assets and money management.

He talks about what true wealth and financial independence are! It will give you insights into research studies about spending habits and how they can affect your investments.

You’ll also learn why passive incomes are bad for you! If you are a beginner, this book is the best thing that will teach you all about personal finance!

4. Why Didn’t They Teach Me This In School? – Cary Siegel

Cary Siegel is a recognized financial expert who has appeared on numerous television shows, including ABC’s 20/20. The book is great for young people and couples! It teaches young investors about the money management BASICS that should have been taught in school.

He also talks about the importance of budgeting, saving, and staying out of debt. This book is ideal for people of ALL AGES on their journey to understanding how money works and how to manage it!

What Will You Learn?

You will learn how to create financial habits that are the building blocks of success. You’ll also discover secrets about financial markets and how they can help you become wealthy.

You’ll also get insights into why some things should be avoided while others can benefit your personal finance. The book is very famous for its 99 personal money management tips and why it is important to have good financial habits

5. The Intelligent Investor – Benjamin Graham

Last but not least, The Intelligent Investor, written by Benjamin Graham. As the name goes, it teaches how to be intelligent when investing.

Graham was one of the greatest finance experts, known for his teachings on value investing strategies, and was Warren Buffett’s mentor and friend.

The book focuses more on the philosophy of investing rather than looking at individual options and opportunities in the market. It talks about broad and general principles for investing and those who want to make wise choices when it comes to their investments.

What Will You Learn?

You’ll learn how to use your money as a tool, not as an object of desire. You’ll also realize why you should invest in stocks and avoid savings accounts and FDs.

This book is about becoming a wise investor and making the best of your money by understanding karma exists.

The author talks about how famous investors like Warren Buffet made a huge fortune with smart and long-term investments. The book is ideal for people who want to jump into the world of inventing and learn how to make smart decisions for long-term investments.

Conclusion

So there you have it! If you are trying to start on your journey of financial independence, these books are the perfect place to begin!

Make sure you do not invest in things you don’t understand. Have a long-term mindset and learn how to be smart about your money.

Make sure that you also keep track of your budgeting and spending carefully. Take what you need and start investing in your future now! Thanks for reading!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.