This post may contain affiliate links; please see our disclaimer for details.

According to PolicyGenius, 52% of Americans have life insurance. Learning the difference between term and whole life insurance is a great place to start!

When it comes to life insurance, there are two main types: term and whole life. But what’s the difference? And which one is right for you?

This blog post will summarize everything you need to know about term and whole life insurance, including cost comparisons and pros and cons.

By the end, you can decide which type of life insurance is best for you!

What is Term Life Insurance?

Term life insurance is the most basic and straightforward type of life insurance.

It is also the most affordable. You are insured for a period, typically 20 or 30 years, with term life insurance.

If you die during that time, your beneficiaries will receive a death benefit.

If you live past the term of your policy, your coverage will end, and you will not receive a death benefit.

For this reason, term life insurance is often called “temporary” or “non-permanent” insurance.

What is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance that covers you for your entire life.

Unlike term life insurance, whole life does not have a set term. As long as you pay your premiums, your coverage will continue.

Whole life insurance also has a cash value component. This means that a portion of your premiums goes into a savings account that grows over time.

You can borrow against this cash value or even surrender the policy for its cash value if you no longer need life insurance.

Whole Life and Term Life Insurance Differences

The main difference between whole life and term life insurance is that whole life insurance provides lifelong coverage. In contrast, term life insurance only covers you for a specific period.

Whole life also has an investment component, which allows you to grow your money over time.

Term life insurance is generally less expensive than whole life insurance but does not offer the same financial security.

Another difference is that whole life insurance has a cash value you can borrow against, while term life insurance does not.

Finally, whole life insurance typically requires a medical exam, while term life insurance does not.

Cost Comparison: Term vs. Whole Life Insurance

Whole life insurance is generally more expensive than term life insurance. This is because it provides lifelong coverage and has an investment component.

The cost of whole-life insurance also depends on your age, health, and the death benefit you choose.

Term life insurance, on the other hand, is less expensive because it only covers you for a specific period.

The cost of term life insurance depends on your age, health, and the length of the term.

When evaluating the cost of life insurance, it’s important to consider your needs and budget. For example, if you are young and healthy, you may be able to get by with a cheaper term life policy.

However, if you have a family or dependents, whole life insurance may be a better choice because it will provide financial security for your loved ones in the event of your death.

If you are young, healthy, and looking for a basic life insurance policy, term life insurance is typically the more affordable option.

You can find options for as little as $20-$50 per month.

If you are older, have health issues, or are looking for a more comprehensive life insurance policy, whole life insurance may be a better option.

In this demographic, you can expect to pay $100-$200 per month for a whole life insurance policy.

These two examples are on the opposite side of the spectrum. The cost can also vary depending on the company you choose, the coverage you need, and various other factors.

Both term and whole life insurance offer payment options, so you can choose what fits your budget.

However, it’s important to remember that whole life insurance policies are more expensive because they provide lifelong coverage. This can add up if you need coverage for 20, 30, or even 40 years.

On the other hand, term life insurance policies are less expensive because they only cover you for a specific time.

If you need coverage for only a few years, such as when your children are young, term life insurance may be a more affordable option.

Choosing this option can save you a lot of money in the long run.

Some industry secrets on why a life insurance policy costs and what it does:

When you apply for a life insurance policy, the company will look at various factors to determine your rates.

As mentioned earlier, the most important factors include your age, health, lifestyle, and the death benefit you choose.

However, the company will also look at your medical history and any pre-existing conditions you have. You can expect to pay higher premiums if you have a history of health problems.

Finally, the company will also consider your family history. If you have a family history of health problems, you may be considered a higher risk and pay higher premiums.

There are pros and cons to both term and whole life insurance. It’s important to weigh these carefully before deciding which policy is right for you.

Pros of term life insurance include:

It is more affordable than whole life insurance.

It is easier to qualify for.

You can choose the length of the term, which gives you flexibility.

Cons of term life insurance include:

It only covers you for a specific period.

Your beneficiaries will not receive a death benefit if you live past the term of your policy.

Pros of whole life insurance include:

It covers you for your entire life.

Your beneficiaries will always receive a death benefit, no matter when you die.

It has a cash value component that allows you to grow your money over time.

Cons of whole life insurance include:

It is more expensive than term life insurance.

You will need to undergo a medical exam to qualify.

How to choose between term and whole life insurance

The best policy for you will depend on your individual needs and circumstances.

Be sure to compare different types of policies before making a decision. This will help you find the coverage that best meets your needs at the most affordable price.

Term life insurance has its pros and mainly its affordability, while whole life offers lifelong protection and has an investment element that builds cash value over time that can be borrowed against it if needed.

If you don’t have any other assets you can borrow against, a whole-life policy can take that position and provide you with a financial safety net.

It depends on your needs as to which policy is better for you.

However, if you are unsure of your future income potential, term insurance may be better. This is because it is more flexible regarding how long you are covered and how much you pay each month.

Both term and whole life insurance have pros and cons, so it’s important to weigh these carefully before deciding which type of policy is right for you.

Consider your needs and budget when making your decision. If you are on a budget, term life insurance is generally more affordable.

If you are looking for lifelong coverage and the peace of mind that comes with it, whole life insurance may be worth the extra cost.

No matter what policy you choose, be sure to compare different policies before making a decision.

This will help you find the coverage that best meets your needs at the most affordable price.

Some factors to consider when choosing between term and whole life insurance include:

Your age

Your health

Your budget

The death benefit you need

How long do you need coverage for

Whether or not you want an investment component in your policy.

If you answer ‘yes’ to any of the following questions, a whole life insurance policy might be a better option for you:

Do I want coverage for my entire life?

Do I want to build cash value that I can borrow against if needed?

Am I looking for an investment opportunity?

If you answer ‘yes’ to any of the following questions, a term life insurance policy might be a better option for you:

Am I on a tight budget?

Do I only need coverage for a specific period?

Is my main goal to provide my beneficiaries with a death benefit?

No matter what policy you choose, be sure to compare different policies before making a decision.

Doing so will help you find the coverage that best meets your needs at the most affordable price.

Questions to ask yourself to help you decide on a specific policy:

How much can I afford to pay in premiums?

What are my long-term financial goals?

What is the most important thing I want my life insurance to do for my beneficiaries?

Answering these questions will help you narrow your options and choose the best policy.

As a reminder, always shop around and compare policies before making a decision. This will help you find the coverage that best meets your needs at the most affordable price.

You can also try negotiating with life insurance companies to get a lower rate.

Remember, the best life insurance policy is the one that meets your unique needs and circumstances. There is no “one size fits all” in life insurance, so be sure to research before making a decision.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you’re looking to save money, you’ve come to the right place! This article will discuss 15 frugal living tips that implement today to save more money.

This post may contain affiliate links; please see our disclaimer for details.

Frugal living can provide several benefits, including increased financial security and peace of mind.

Making small changes today can help you get started on the path to financial independence.

So let’s dive in further, shall we?!

What does frugal living mean?

Frugal living means finding ways to save money with a focus on achieving financial minimalism. It’s about being mindful of your spending and making conscious decisions about where you spend your money.

Frugal living doesn’t mean going without or depriving yourself – it simply means being more mindful of your spending and making choices that align with your values.

For example, you may choose to spend less on clothes so that you can afford to travel more. Or, you may choose to cook at home more often so that you can eat out less.

Ultimately, frugal living is about balancing saving money and enjoying life. It’s about making choices that allow you to live well within your means.

What Benefits Come from Frugal Living?

Unfortunately, many associate frugal living with a negative connotation.

Some assume that those who live frugally are cheap, always looking for ways to save money, and never have any fun.

In reality, there are a plethora of benefits that come from living a frugal lifestyle!

Content with what you have

You stop comparing your life to others and learn to appreciate the things you do have.

This also helps to increase your self-worth because rather than depending on material possessions to make you feel good, you are relying on yourself.

Focus on the things that are truly important to you

You aren’t wasting your money on unnecessary items, so you can put your time and energy into the things that matter most to you.

Learn to be more resourceful

When you have less money to spend, you have to get creative about how you use the resources you do have. Doing so can lead to some great invention and problem-solving skills.

Very good at budgeting and managing finances

Frugality leads to better financial habits and can help you save money in the long run.

It can be financially beneficial because you are less likely to overspend and get into debt.

Overall, many benefits come from living a frugal lifestyle. If you’re considering making changes and want to save money, consider giving frugal living a try.

You might be surprised by how much you enjoy it!

Without further ado, let’s jump into the 15 frugal living tips I’ve prepared to get you started!

1) Evaluating your spending habits

Track where you are spending your money for a month or two to get an idea of where you can cut back. This is the most important step in living a more frugal lifestyle.

The key is ensuring you don’t modify your spending habits during the evaluation period.

You will want to get an accurate idea of where your money is going exactly.

2) Create a budget and stick to it

Determine what expenses are essential and what can be cut back or eliminated. This is one of the most important frugal living tips you can implement now!

Having a written budget and detailed plan will make you more likely to stick to your frugal goals.

3) Shop at thrift stores and garage sales

You can find some great deals on secondhand items that are still in good condition.

This is a great way to save money on clothing, household items, and more. It can also be a fun hobby!

4) Cut back on your cable bill or eliminate it

There are many ways to watch TV and movies without paying for a cable subscription.

You can use an antenna, stream content online, or rent movies from Redbox or similar services.

5) Reduce your energy consumption

You can save money on your utility bills by making simple changes like turning off lights when you leave a room and unplugging appliances when they’re not in use.

Remember, this is important because these costs can add up very fast.

6) Make your cleaning products

There are many recipes available online for DIY cleaning products. This is a great way to save money and avoid using harmful chemicals in your home.

Common DIY cleaning products include all-purpose, glass, and carpet cleaners.

One simple recipe is this all-purpose cleaner: mix water, baking soda, and white vinegar in a spray bottle.

You can clean surfaces like countertops, appliances, and floors.

7) Use discounts and coupons

When trying to save money, it’s important to take advantage of discounts and coupons whenever possible.

Whether you’re buying groceries or clothes, there are usually ways to get a better deal.

For example, you can often find grocery coupons online or in the Sunday paper.

Plus, many stores offer discounts if you sign up for their email list.

So if you’re looking to save money, keep an eye out for discounts and coupons. It can make a big difference in your budget!

Do you want to get paid for shopping online? If so, we highly recommend checking out MyPoints, where you can earn money by shopping online, taking surveys, or playing games.

There are also opportunities to get special deals and FREE access to the best coupon codes. See how you can start making and saving money with MyPoints.

8) Don’t buy premium brands

Another frugal living tip is to try generic brands. Generic brands are often just as good as name-brand products but cost a lot less.

So if you’re looking to save money on groceries, check out the generic brands. You might be surprised at how much you can save!

9) Buy in bulk

One way to save money is to buy in bulk!

This can be done at a Costco, Sam’s Club, or Amazon Prime store. You can save money on groceries and household items when you buy in bulk.

Plus, you’ll have fewer trips to the store, which will save you time and money.

10) Reuse and upcycle

One of the best ways to save money is to reuse and upcycle items instead of buying new ones.

Things that fit into this category can be anything from clothes to furniture to home decor. Not only will you save money, but you’ll also be doing your part to reduce waste and help the environment.

This includes investing in glass water bottles, handkerchiefs (instead of Kleenex), and rags (instead of paper towels).

You can also save money by mending clothes instead of buying new ones.

11) Hang dry your laundry

Hang-drying your laundry is a great way to save money on your energy bill.

It takes a little bit longer than using a dryer, but it’s worth it in the long run.

Plus, your clothes will last longer if you hang them to dry instead of putting them in the dryer.

12) Cook at home

One of the best ways to save money is to cook at home instead of eating out.

We understand it can be challenging if you’re used to eating out all the time, but it’s worth it in the long run.

Not only will you save money, but you’ll also be able to control what goes into your food.

13) Make a home gym

If you’re looking for ways to save money, one area you can focus on is your health and fitness.

A gym membership can be expensive, and if you don’t live close to a gym, it can also be time-consuming to drive there and back.

Instead of spending money on a gym membership, why not create your home gym?

You don’t need a lot of equipment to get started – a few basic weights, an exercise mat, and some resistance bands can go a long way.

And if you don’t have room for bulky equipment, you can do plenty of bodyweight exercises to stay fit.

Creating your home gym can be a great way to save money and time, and it’s a great way to get in shape.

So if you’re looking for ways to be more frugal, this is one tip you should consider.

This seems like a no-brainer, but it’s important to remember. Just because something is on sale doesn’t mean you need to buy it.

If you can live without it, then don’t spend the money. This is one of the most important frugal living tips!

To Wrap Things Up

Frugal living is about making small changes that can save you money in the long run.

By following these frugal living tips, you’ll be on your way to a minimal and happy lifestyle!

Just remember to take things slowly and focus on what’s important.

With a little effort, you can save a lot of money! Please share how you live a frugal life in the comment section below! 🙂

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Lower Your Heating Bill

Don’t become a financial victim of cold weather! If you’re looking for ways to save money on your heating bill, you’ve come to the right place.

According to Reuters, the average cost of using natural gas for heating in the US was expected to rise 30% this last winter.

The time is now to find ways to lower your heating bill this year and for years.

This article will discuss ten tricks that will help keep you warm and comfortable all winter long without breaking the bank.

So put on a sweater and get ready to learn how to save some money!

My Video Sharing How To Save Money on Heating Bill

1) Use a Programmable Thermostat

If you don’t already have a programmable thermostat, now is the time to invest in one.

A programmable thermostat will allow you to set different temperatures for different times of the day and night.

For example, you can set the temperature lower when you’re asleep or away from home.

Often people will leave their heating on all day long, even when they’re not home, but this is a huge waste of energy and money.

A programmable thermostat can save you significant money on your heating bill over time.

Below is a very popular choice, the Nest Thermostat which uses a sensor and GSP from your phone to know whenever you are leaving the home.

2) Weatherproof Your Home

One way to keep your home warm is to ensure it is well insulated.

Check for drafts around doors and windows and seal them with weatherstripping or caulking.

You can also add insulation to your attic or walls if needed!

Even a small draft can let in a lot of cold air, so it’s important to ensure your home is well-sealed.

These simple steps can significantly affect how warm your home is and how much money you spend on heating it.

3) Use Your Fireplace More Efficiently

Assuming you have a fireplace, using it more efficiently can help to lower your heating bill.

Make sure to open the flue when lighting a fire and close it when the fire dies down. This will help to prevent heat from escaping up the chimney.

In addition, using a glass fireplace door can help to keep heat in the room and lower your heating bill.

4) Dress Warmly

One simple way to lower your heating bill is to dress warmly.

Wear socks, slippers, and layers of clothing around the house. This will help you to feel comfortable at a lower temperature and save you money on your heating bill.

Dressing warmly is the best way to save money on your heating bill. So put on a sweater and get cozy!

5) Use More Bed Coverings

In addition to dressing warmly, you can also use blankets and throws around the house.

Blankets can help to keep you warm without cranking up the heat. Just be sure not to leave them on the bed when you’re not using them so they don’t get wrinkled.

6) Use Space Heaters

If you have a large home, it may not make sense to heat the entire house to one temperature. Instead, you can use space heaters to heat individual rooms as needed.

Doing this can save you money on your heating bill by only heating the rooms you’re using.

Just be sure to turn off the space heater when you leave the room, and always keep an eye on them.

Space heaters are a great way to save money on your heating bill, but they can be dangerous if misused.

Always turn them off when you leave the room, and never leave them unattended.

7) Negotiate With Your Utilities Company

If you struggle to pay your heating bill, reach out to your utility company. Many companies have programs to help low-income customers with their energy bills.

In addition, many companies will work with you to create a payment plan that works for your budget.

Don’t be afraid to reach out and ask for help if you’re struggling to pay your heating bill. Some programs and people can help you through this tough time.

Research what other companies offer to negotiate effectively and use that to your advantage.

Utility companies understand that many people struggle to pay their bills during tough economic times.

Don’t feel bad about asking for help. 🙂

8) Use Curtains or Blinds

Another way to keep your home warm is to use curtains or blinds. During the day, open them up to let in the sunlight.

The sun can help to warm your home and lower your heating bill. Just be sure to close them at night to keep the heat in.

You can also use heavy curtains or blinds to block out drafts from windows. This will help keep your home warmer and save money on your heating bill.

9) Use a Humidifier

If your home is dry, it can make you feel colder. Using a humidifier can help to add moisture to the air and make your home feel warmer.

Using a humidifier can save money on your heating bill because you can lower the temperature of your thermostat and still feel comfortable.

Just clean your humidifier regularly to prevent mold and bacteria from growing in it. The air will also be hot and moist, so it can help warm you up directly.

10) Don’t Heat Unused Rooms

One of the best ways to save money on your heating bill is to heat the rooms you’re using.

If you have unused rooms, close the vents or doors to those rooms, so you’re not wasting heat.

You can also close off unused rooms to save money on your heating bill.

You may feel cold if you close off unused rooms, but you can always open the door or vent if you need to.

Just be sure to close them back up when you’re done so you don’t waste heat.

The Bottom Line

Saving money on your heating bill is important, especially during winter.

No matter your situation, there are ways to lower your heating bill.

Following these tips, you can stay warm and comfortable all season long without breaking the bank.

So put on a sweater and get ready to save some money!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Couple enjoying financial minimalism 🙂

Financial minimalism is a growing trend in the world of personal finance.

The idea is to enjoy life more by removing unnecessary financial clutter and simplifying your money choices.

In this article, we will discuss what financial minimalism is exactly, the benefits you can experience, and how you can achieve it!

We will also provide fourteen tips to help get you started!

What is Financial Minimalism?

Financial minimalism is living with less financial clutter by consciously deciding to spend less and save more. They believe in living a simple life free of debt and other financial burdens. Financial minimalists focus on quality over quantity.

The main reason why many people are drawn to financial minimalism is that it emphasizes living a simple life.

It’s about being intentional with your money and only buying things that add lasting value to your life.

Give it a try; you might enjoy decluttering your life and living with less spending or only spending on things you need.

For some, it may be a way to save money and become debt-free. Others may want to downsize and live a more sustainable lifestyle. Financial minimalism can help you achieve these things!

It differs from traditional minimalism because it focuses on reducing expenses and debt rather than just on physical belongings.

For example, a physical minimum might live in a small house or apartment and own only a few items of clothing.

A financial minimalist may have a similar lifestyle, but their focus would be reducing expenses and debt instead of physical belongings. It’s all about living within your means and not getting too complicated with spending, saving, and investing.

Financial minimalists are typically practiced by people looking to save money, become debt-free, remove financial clutter, or downsize their lifestyle.

Practitioners must also learn to be disciplined. A lack of focus can easily lead to overspending.

Benefits of Financial Minimalism

The main benefit of financial minimalism is that it can help you save money. It can also lead to a simpler and more sustainable lifestyle.

In other words, it’s a pathway to a sustainable life because if you over-consume financially, you will always be in debt or working to pay off debt.

Eventually, when it is time to retire, you will not have the funds to do so. Being unable to work and still having to pay off debt is an unhealthy way to live.

Financial minimalism can help you avoid that lifestyle and reach financial freedom sooner!

Reduced stress is another major benefit of simplifying your spending and gaining control over your finances.

Financial troubles are often associated with high levels of stress. So, by decluttering your finances, you can reduce stress and live a more joyful life.

Financial minimalism is important because it can help you find joy while saving money.

If you can live with less, you’ll be able to put more money into savings and investments, leading you to a better and brighter financial future!

Sounds pretty amazing, right?

Now that you know what financial minimalism is, let’s learn more about how you can begin to practice this concept.

How to Practice Financial Minimalism? 14 Tips

One way to start practicing financial minimalism is to save up for big purchases instead of buying on credit.

Another great way is to create a budget and stick to it.

You can also declutter your home and eliminate anything you don’t need or use.

Start small and see how it feels to live with less money.

You may be surprised at how much simpler and happier your life becomes! So let’s look at 14 ways you can get started today.

1) Start by evaluating your current spending habits

Track where you are spending your money for 30 days.

Doing so will help you become aware of your spending patterns. By becoming aware of your spending, you can make changes where necessary.

Once you know your spending patterns, start setting aside monthly money for savings and investments.

Begin with $50, for example. Then, increase this amount each month as you become more comfortable.

2) Set meaningful goals for yourself

Ask yourself the following questions-

What do you want to achieve with your finances?

Do you want to be debt-free?

Do you want to save for a down payment on a house?

Next, write down some realistic goals with deadlines to help keep you accountable.

3) Unsubscribe from marketing emails and avoid impulse purchases

Dig deep to find out what your needs are and what really adds value to your life. Most likely, you don’t need that new shirt or those shoes.

Unsubscribe from marketing emails so you’re not constantly tempted to spend money.

Looking for an easy way to manage subscriptions? Look no further than ROCKET MONEY. We love how they provide you with the tools to track spending, lower bills, and track your net worth!

4) Unsubscribe from paid memberships and unused services

Do you need that gym membership? If you’re not using it, take the time to cancel it.

The subscriptions you don’t use or don’t add value to can clutter your credit card statements and add up over time.

5) Create a capsule wardrobe

A capsule wardrobe is a small collection of clothes that can be mixed and matched to create multiple outfits.

This is a great way to save money and declutter your closet!

By having less selection of clothes to wear, you’ll also be able to spend less time deciding what to wear.

Having a capsule wardrobe is a tactic for many physical minimalists but can also be a mindset reminder for financial minimalists!

6) Sell items you no longer need or use

Have a garage sale, sell items online, or donate them to a local thrift store.

By letting go of old items, you make room for new experiences. 🙂

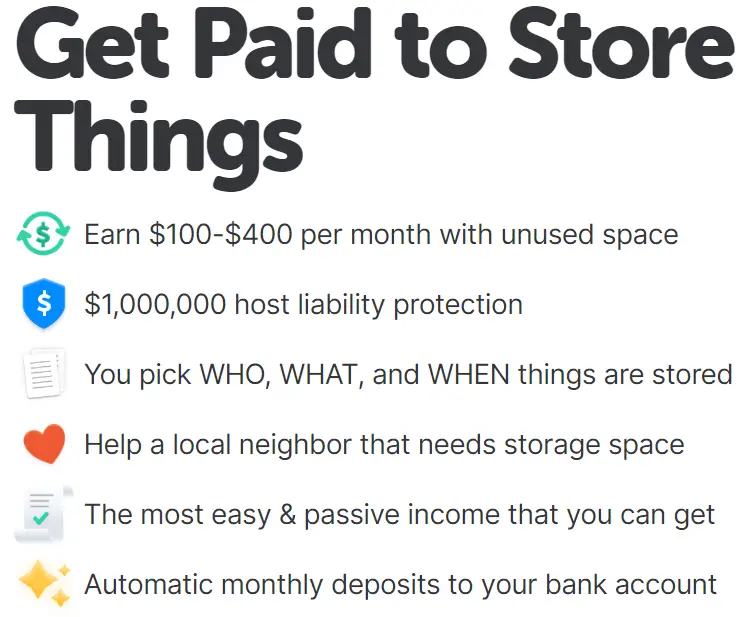

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

7) Start cooking at home more

Eating out is expensive! Save money by cooking meals at home. You can also save money by batch cooking and meal planning.

Batch cooking is when you cook multiple meals at once and then freeze them for later. Meal planning is when you plan out your meals for the week in advance. Some meal-planning services may be worth using, too.

If you’re busy and want a custom meal plan, I recommend trying out NutriSystem! You can start by taking an easy survey. Then they will send you balanced and nutritious meals and snacks!

You can now buy a month and get an entire month free! – Check it out today at NutriSystem! 🙂

8) Live below your means

Spend less than you earn and invest the rest. This will help you build wealth over time.

This tip may seem common sense, but it is one of the most important!

9) Be content with what you have

Be grateful for what you have and learn to live with less. This doesn’t mean you can’t have nice things, but don’t let your possessions own you.

You’ll be much happier when you learn how to appreciate the simple things in life.

10) Invest in experiences, not things

Instead of buying material possessions, invest in experiences. This could include travel, going to concerts, or taking cooking classes.

These experiences may seem like they cost more money, but they will result in more happiness and greater memories than any material possession.

11) Be patient

Financial success takes time and patience. Don’t expect to become a millionaire overnight.

The concept of delayed gratification and actively practicing it can be the difference between financial success and failure.

Delayed gratification is the ability to resist the temptation of an immediate reward and wait for a later, possibly greater, reward.

When it comes to your finances, think long-term.

12) Downsizing your home or getting rid of unnecessary expenses

If you have a lot of stuff, consider downsizing your home. This will save you money on rent or a mortgage.

This step can be difficult when pursuing financial minimalism, but it is worth considering.

An investment approach would be to rent out your current residence and then buy a new property while still living within your means.

13) Don’t compare your financial situation to others

Everyone’s circumstances are different. Focus on your own journey, and don’t compare yourself to others.

Don’t compare your spending to others. For example, if your friends just bought a new car, don’t feel you need to do the same.

People who struggle with financial minimalism cannot get past their insecurities of FOMO (fear of missing out).

14) Automate your finances

Automating your finances is a great way to stay on top of your budget and avoid late fees.

You can set up automatic payments for your bills and have a certain amount of money automatically deposited into savings each month.

By automating your finances, you will stay disciplined with your spending and reach your financial goals.

Conclusion

There are a few different ways to achieve financial minimalism. The most important aspect is to be intentional with your money.

You need to be aware of your spending habits and make changes where necessary.

In addition, try to live below your means. Spend less than you earn and invest the rest. This will help you build wealth over time.

Finally, don’t compare your financial situation to others. Everyone’s circumstances are different.

Focus on your journey, and don’t compare yourself to others.

There’s no one way to achieve financial minimalism. It’s a personal journey that looks different for everyone.

It’s important for those pursuing financial freedom to find what works best for them.

Financial minimalism may not be the right fit for everyone. But if you’re looking to declutter your life and finances, it’s worth giving it a try!

Please comment below with your thoughts and experiences on practicing financial minimalism!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

There are many investment options to choose from when it comes to making money. Two of the most popular choices are real estate and stocks.

Investing in the real estate market and investing in the stock market both have pros and cons, and it cannot be easy to decide which option is best for you.

In this article, we will compare and contrast real estate and stocks so that you can make an informed decision about the right investment for you!

Many may feel overwhelmed when deciding between stocks and real estate, as these two asset classes can differ.

However, some key similarities between the two should be taken into account. They are similar as they both have the potential for asset appreciation and passive cash flow.

Both real estate and stocks share similar investing principles, such as the time-tested adage “buy low and sell high.”

In other words, to make profits in either asset class, you must purchase an investment when prices are low and then sell when prices have increased.

Of course, there are also key differences between real estate and stocks that should be considered.

One major difference is the level of liquidity.

Stocks are much more liquid than real estate, meaning they can be sold quickly and with less hassle.

It’s important to consider this if you need to access your money quickly or if you are worried about being able to sell your investment promptly.

Another key difference is the level of risk involved.

Real estate is generally considered a more stable investment, while investing in individual stocks can be more volatile. Real estate may be a better option if you are risk-averse, while single stocks may be more suited for those comfortable with taking on a higher level of risk.

Now that we have explored some basic similarities and differences between the two asset classes, let’s go into more detail about the returns you can expect from each.

This post may contain affiliate links; please see our disclaimer for details.

Returns: Real Estate vs. Stocks

One of the most important things to consider is the returns you can expect from each investment.

Regarding real estate, the average return is around 9-12%. This number can fluctuate depending on various factors, such as location and the type of property you invest in.

However, over the long term, real estate has proven to be a relatively stable investment and can be a considerably higher return on investment.

When it comes to stocks, the average return is around 12%. Again, this number can fluctuate depending on various factors, such as the company you invest in and the overall market conditions.

However, stocks have the potential to generate higher returns, but they are also more volatile.

Real estate can generally yield higher rents than dividends from stocks. Real estate can be a great option if you are looking for income investments.

With that said, stocks have the potential for compounded capital appreciation, which can lead to higher returns in the long run.

Investing in real estate or stocks comes with its risks. With real estate, one of the biggest risks is the potential for a decrease in property values.

This can happen for various reasons, such as a recession or changes in the local market.

Another risk to consider is the possibility of vacancies, which can lead to a loss of income.

You can interview your tenants, but you can never be sure they will stay long.

Regarding stocks, one of the biggest risks is the potential for losses due to market volatility.

The value of your investments can go up and down rapidly, leading to losses if you are not careful.

Another risk to consider is the possibility of fraud or mismanagement by the company you invest in. This can lead to a loss of your investment entirely.

There are ways to lower the risks of each investment type. Some ways to do this are by diversifying your portfolio, investing in quality assets, and working with experienced professionals.

Let’s explore some more ways to lower your risks.

Ways To Lower Your Risks When Investing

By keeping these investment principles in mind, you can lower the risks whether you want to become an investor in the stock markets or real estate.

Diversify: Don’t put all your eggs in one basket. This is key in any investment, whether buying stocks, picking a mutual fund, or investing in real estate.

Have a long-term outlook: Don’t get caught up in the market’s day-to-day fluctuations.

Be patient: Don’t expect to get rich quickly. Investments take time to grow.

Know your risks: don’t invest in something you don’t understand. Make sure you know the risks involved before you invest your hard-earned money.

Know the law: Some certain rules and regulations apply to different investments. Make sure you understand the laws before you make any decisions. By having insurance with a good law team, you can be sure you are covered in case any legal issues should arise.

Keep emotions out of it: Don’t let your emotions guide your investment decisions. This can be not easy, but it’s important to remember that investments are based on numbers, not feelings.

Do not over-leverage yourself: Don’t borrow too much money to finance your investments. This can lead to financial ruin if things go wrong.

Start small: Don’t go all-in on your first investment. Start small and gradually increase your investment over time.

Work with experienced professionals: Get help from those who know what they’re doing. This is especially important if you’re new to investing.

By following these principles, you can minimize your risk and maximize your chances for success, no matter your investment type.

Now that we have explored the risks and rewards of real estate and stocks let’s look at each investment’s pros and cons.

Pros and Cons: Real Estate

One of the biggest advantages of real estate is that it is a physical asset.

You can see and touch your investment, which can give you a sense of security.

Another advantage is the potential for high returns. As we mentioned earlier, real estate has the potential to generate higher income returns than stocks, although it is also riskier.

Real estate debt. It can be seen as a risk by some people. Others will perceive real estate as a great investment method without using much of your own money.

This is because you can often use leverage to purchase property, which means you can control a much larger asset for a smaller investment.

Real estate can also offer tax benefits. For example, you can deduct the interest you pay on your mortgage from your taxes.

You can also depreciate the value of your property, which can lead to significant tax savings.

The biggest disadvantage of real estate is the fact that it is illiquid. It can take longer to sell your property, and you may not be able to get your money out as quickly as you would like.

Another disadvantage is that maintaining and repairing your property can be expensive, which can affect your profits.

The most troublesome disadvantage of real estate is bad tenants. As a landlord, you may experience mistreatment of your property or be sued for eviction.

You may also have to deal with damage to your property that tenants cause. A solid screening process can help minimize the risk of bad tenants.

Pros and Cons: Stocks

One of the biggest advantages of stocks is that they are liquid, which means you can sell them relatively quickly if you need to.

Another advantage is the potential for high returns. As we mentioned earlier, stocks have the potential to generate higher compounded returns than real estate, although they are also riskier.

The biggest disadvantage of stocks is the fact that they are volatile. Their value can go up and down rapidly, leading to losses if you are not careful.

You may also experience negative tax consequences, such as capital gains taxes, if you sell your stocks for a profit.

If you plan to trade frequently, it’s important to consider this. To become a long-term investor, consider investing in tax-friendly accounts such as an IRA.

Another disadvantage of stocks is that they require ongoing maintenance. For example, you may need to pay fees to a financial advisor to help you manage your portfolio.

If you plan on picking stock individually on your own, it can be time-consuming and stressful. However, these disadvantages can be negated by investing in stocks through ETFs.

Another disadvantage is the possibility of price manipulation by whale investors. This is when a small group of investors buys or sells a large number of shares, which can cause the price to go up or down.

The most troublesome disadvantage of stocks is the potential for fraud. This can happen if a company misleads investors about its financial situation or commits accounting fraud, which can lead to losses for investors.

Stocks vs. Real Estate: Which is right for you?

Both real estate and stocks have the potential to generate high returns and create wealth over time.

However, they each come with their own set of risks and disadvantages.

So, which is the right investment for you?

The answer to this question depends on your circumstances. For example, stocks may be a better option than real estate if you are looking for an investment that you can sell quickly.

On the other hand, if you are looking for a more stable investment that offers tax benefits, then real estate may be a better option.

If you only have a few thousand dollars to invest, it may be better to invest in the stock market as a down payment for a house may require more than what you have.

As your income increases, it wouldn’t hurt to compound small amounts in the markets. During this period, you should also ensure that your credit score is in good standing, as this will be a factor when you’re ready to purchase the property.

Once your income has increased and you can save money faster, you can consider looking into investment properties or following a similar strategy to us where we buy a residential property, fix the property up, rent it out, then refinance.

If you don’t want to own real estate yourself but still want exposure to the real estate market, try investing in REITs or with property crowdfunding. These investments require a lower barrier of entry, but you will not receive the same tax benefits of leverage potential as if you owned the property.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

No matter what route you decide to take, remember that you are on the right track for wanting to learn about these two investment assets.

Before making a decision, remember your investment goals, risk tolerance, and time horizon.

Real estate may be a better option if you want an investment that will generate passive income through rental properties. But stocks may be a better choice if you want an investment that will appreciate without much maintenance.

You may want to consider both options and hold both long-term.

As someone that is thinking about their financial future, you are already ahead of most people!

Sometimes we can become biased toward one option or the other. It is important to remember that you should diversify your portfolio and not put all of your eggs in one basket.

Doing this can minimize your risk and maximize your potential for returns.

The bottom line is that there is no right or wrong answer regarding real estate vs. stocks.

The answer depends on your individual circumstances and investment goals. So, take the time to research and make an informed decision about which option is right for you.

In pursuing financial freedom, never forget that you can benefit from both asset classes.

Real Estate vs. Stocks: Which is the Better Investment?

So, which is the better investment? Real estate or stocks? The answer depends on your circumstances.

Real estate may be a better choice if you are looking for stability. However, stocks may be a better option if you are looking for quick, high returns.

Ultimately, the best decision is to diversify your investment portfolio and not put all of your eggs in one basket. Also, consider index funds or ETFs that allow you to invest in hundreds of companies at once. This way, you can minimize your risk and maximize your potential for returns.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.