If you have wondered what the term “lifestyle creep” means, you are not alone. This is a term that is often used but not always fully understood.

Lifestyle creep can be very dangerous for your finances and quickly lead to debt if not careful.

In this blog post, I will define lifestyle creep, discuss some warning signs, and provide some insights on how to avoid it.

This post may contain affiliate links; please see our disclaimer for details.

What is Lifestyle Creep?

Lifestyle creep is defined as “a gradual increase in spending that occurs when income increases or lifestyle changes.” It’s that tendency to spend more money as your income goes up. This can be a hazardous trap because it can quickly lead to debt.

It feels great to get a pay raise or bonus at work, but oftentimes it leads to more spending or even living outside of our means.

Let’s say someone starts with a salary of $40,000. After working very hard over the years with regular salary increases, and they are now making $70,000.

If not careful, too much money could be spent on wants such as clothes, eating out, or buying new things. Many of us enter this way of thinking and unfortunately end up in debt, regardless of having more income.

Rather than saving or investing the extra money, too many of us go out and spend it all, which can quickly lead to a worse financial position.

Another thing to keep in mind is to calculate your net income. A $2,000 raise will be taxed so it’s important to know exactly how much extra money you have each month and not miscalculate.

There are several warning signs that we should all keep in mind that can lead to lifestyle creep. If you notice any of the following, it may be time to reevaluate your spending habits.

Buying new clothes more often: If you find yourself shopping for new clothes more frequently, it may be a sign that you are spending too much money. Try sticking to a budget and only buying clothes when needed.

Eating out at restaurants more often: Going out to eat to celebrate your new raise once or twice is fine, but if you are doing it all the time, it may be a sign of lifestyle creep. Try to cook at home more often and only eat out on special occasions.

Taking more vacations: If you are planning more and more vacations, it may be a sign that you are spending too much money. Try to take one or two vacations per year and stick to a budget while you are on vacation.

Upgrading your car or home: This is commonly known as “keeping up with the Joneses.” Just because your neighbor gets a new car or house does not mean that you need to as well. It can be difficult at first, but resisting the urge to keep up with the people around you will provide you with many benefits.

Credit card debt is increasing: With a new raise, you may be tempted to use your credit card more often. However, this can lead to debt and financial problems down the road. Try to pay off credit card balances each month and only use it for emergencies.

No any extra funds to save or invest: After a raise, you should hopefully be able to save or invest at least some of the extra money. If not, it may be a sign that your spending is out of control. Try to automate your savings and investments so that you are not tempted to spend the extra money.

If you notice any of these signs, it is important to take action immediately. Lifestyle creep can quickly lead to debt and ruin your finances if you do not catch it early on.

How to Avoid Lifestyle Creep

If you believe you may have become a victim of lifestyle creep, don’t worry! There are ways to switch your spending habits and get back on track.

Here are a few tips:

Prioritize Your Money: This can be done in different ways. There is zero-based budgeting for example where you track every dollar coming in each month and every dollar spent.

No matter the method you choose, the goal of prioritizing your money is to control where it goes each month by sending your income to the most important categories first such as bills, savings, paying off debt, and investing.

A great way to create a budget without lifestyle creep is to use percentages rather than dollar amounts. As your income increases, your budget should automatically adjust without you needing to make any changes.

For example, if you want to save 20% of your monthly income, you would put $400 into savings if you make $2000 per month. If you get a raise and start making $3000 per month, you would then put $600 into savings.

The percentage-based budget saves you more money as your income increases automatically. Additionally, you don’t have to make any changes to your budget.

Save first, spend later: A great way to avoid lifestyle creep is to save your money and spend what is left over. Although this seems common sense, it can be easy to forget when you have extra money in your account.

Try setting up a direct deposit from your paycheck into your savings account. This way, you will never see the money and will be less tempted to spend it.

Invest in yourself: One of the best investments you can make is in yourself. Try to invest in your education or career to earn more money down the road. This will help you keep up with inflation and avoid lifestyle creep.

Be mindful of your spending: It is important to be aware of spending habits. If you are always buying new clothes or going out to eat, try to cut back in other areas.

There is nothing wrong with treating yourself occasionally, but let’s try not to get out of control here. 🙂

Talk to a financial advisor: A financial advisor can help you create a budget, save for retirement, and invest in yourself.

They can also help you stay on track if you have already started to creep into lifestyle inflation.

Live below your means: It is important to live below your means, even if you are making a good income. This means spending less than you earn and saving and investing the rest.

How to manage your money to live below your means can be daunting, but it doesn’t have to be. There are some simple rules that you can follow to help make managing your finances easier.

The method states that you should allocate 50% of your income toward essentials, 30% towards wants, and 20% towards savings.

Invest in cash-flow-producing assets before you buy liabilities: It is important to invest in assets that will produce income. This may include investing in real estate, stocks, or bonds.

Investing in these assets can create a passive income stream that can help cover your expenses.

For example, if you want to improve your lifestyle by subscribing to a $100 monthly gym membership, you should invest in assets that produce at least $100 per month. By doing you are improving your lifestyle without putting yourself at financial risk.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

Focus on improving your skills rather than acquiring stuff: One of the best ways to improve your lifestyle is to improve your skills. This may include taking free online courses, reading library books, or training to fit better.

Finding hobbies and passions that do not require much financial investment can help you live a better lifestyle without spending more money.

Don’t get too excited about promotions and stick to your financial plan: It can be easy to get caught up in the excitement of a promotion or raise. However, it is important to stick to your financial plan. Work on saving extra money that you make so you do not start lifestyle creep.

Lifestyle creep is a real problem, but it is possible to avoid it.

Following these tips, you can keep your finances on track and live a comfortable life without lifestyle creep.

The Bottom Line

If you are always living paycheck to paycheck, even after a raise, it may be time to look at your spending habits. Lifestyle creep can be a dangerous trap to fall into, but there are ways to avoid it.

Try to stick to a budget, save or invest your extra money, and resist the urge to keep up with the people around you. These simple steps can help you avoid lifestyle creep and keep your finances on track.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Traveling is a great way to see the world and learn new things, but it can also be expensive! For example, the average cost of a domestic flight in the United States is around $260, and the average hotel room costs over $100 per night. Start using the 17 pro tips in this article to save money on travel expenses!

This post may contain affiliate links; please see our disclaimer for details.

How to Save Money While Traveling?

Traveling can be expensive. This is especially true if you are not used to living out of a suitcase and spending most of your time on the road.

Looking to save money while traveling? There are pro tips that can help you do just that!

1) Plan your trip in advance

This will allow you to find the best deals on flights and accommodation.

It’s also a good idea to have an idea of what you want to do and see while you’re on your trip, as this will help you budget accordingly.

2) Travel during the off-season

The prices of flights and accommodation are usually significantly lower during the off-season. This is because fewer people are traveling during this time.

The busiest seasons are usually summer and winter, so if you’re looking to save money on travel expenses, consider traveling during the spring or fall.

3) Choose your destination wisely

Some destinations are more expensive than others. If you’re on a tight budget, it’s a good idea to choose a destination that is known for being relatively affordable.

Some cheap destinations still offer a lot to see including Southeast Asia, Eastern Europe, and South America.

4) Stay in hostels or guesthouses

Hostels and guesthouses are usually much cheaper than hotels, and they can be a great way to meet new people. Luxury hotels can really add up.

Especially if you opt-in for additional amenities like a spa, room service, or a concierge.

5) Cook your own meals

Eating out can be expensive, so one way to save money while traveling is to cook your meals. This is especially easy if you’re staying in a hostel or guesthouse with a kitchen.

You can still have an adventurous experience by visiting the local farmer’s market and cooking with ingredients that you’re unfamiliar with.

5) Use public transportation

Taxis and rental cars can be expensive, so public transportation is a great way to save money while traveling. They can also be a great way to meet new people and explore without an exact destination.

Getting lost with a map can lead to some of the best traveling experiences.

7) Visit free attractions

There are often many free attractions in a city or town, so research before you visit somewhere new. For example, hiking trails, parks, and museums often have no entrance fee.

These activities will help you save money while allowing you to see and do new things.

8) Buy souvenirs wisely

Souvenirs can be a great way to remember your trip, but they can also add up quickly. If you’re on a budget, choosing souvenirs wisely is a good idea and only buying what you know you’ll use or display.

Try buying souvenirs from a local market instead of a souvenir shop to save money.

For example, rather than buying a $10 mug, find a local artist selling pottery for $8. Not only will you support a local business, but you’ll also end up with a one-of-a-kind souvenir.

9) Use your credit card points

If you have a credit card with rewards points, you can use these to save money on your travel expenses. By using your points to pay for flights, accommodation, or even souvenirs, you can significantly reduce the cost of your trip. Before going on the trip, make sure only to use the credit card that offers the best benefits for travel.

Travel points are often accumulated faster than you think, so this is a great way to save money if you plan to take multiple trips shortly. You might as well use the points, as you cannot exchange them for currencies.

10) Travel with a friend

Sharing expenses with a friend can help you save money while traveling. Plus, it’s always more fun to explore new places with someone else. Some expenses that you can share while traveling are accommodation and transportation.

Many travel agencies also offer bundled deals if you’re traveling with a group, so it’s worth investigating these options.

11) Fly economy class

It can be tempting to fly first or business class, but the economy is usually much cheaper. If you’re looking to save money on travel expenses, it’s a good idea to fly economy class.

12) Get travel insurance

This is one of the most important tips, especially traveling overseas. Travel insurance will cover you in case of an emergency, whether it’s a medical situation or if your luggage is lost or stolen.

Doing this can save you a lot of money in the long run, so it’s worth the investment.

13) Don’t exchange currency at the airport

Converting currency is often done at a poor exchange rate, so it’s best to avoid exchanging money at the airport. If you need cash, try using an ATM instead. This will give you a better exchange rate and save you money in the long run.

You can also try to use a credit card that doesn’t have foreign transaction fees to save money on currency conversion.

14) Use apps to save money

Many apps can help you save money while traveling. Use apps that book flights and accommodation at the best prices. Some apps help you find discounts on activities, food, and transportation. Using these apps saves you a significant amount of money on your trip.

For example, the app Hopper can help you find the best deals on flights. If you are looking for the best hotel discounts, the app HotelTonight can help you find discounts on hotel rooms.

GasBuddy is a great app that can help you find the cheapest gas prices in your area. If you are traveling to a city, ParkWhiz can help you find discounts on parking. Using these apps can save money while still having a great time on your trip.

16) Bring your own food

If you’re going on a road trip or taking a long flight, it’s a good idea to bring your own food. This will save you money on food expenses, and you’ll also be able to control your eating.

Of course, if you are traveling far, it’s not realistic to bring all your food with you. In this case, try to buy groceries from the local market and cook your meals. This is a great way to save money and eat healthily while traveling.

Eating out all the time can be expensive, so it’s worth it to cook your meals when possible. When traveling, it can be common to overindulge, but by cooking your own meals, you can dine out occasionally rather than every meal.

16) Avoid shopping for designer

When on vacation, we can sometimes be tempted to go shopping. This is because we see all the beautiful things we can’t find at home. However, it’s important to resist the temptation and stick to your budget.

Overspending can quickly add up and blow your budget. If you want to save money while traveling, avoid shopping for designer clothes and other items that do not fit your budget.

17) Negotiate Effectively

For each purchase you make while on vacation, always remember to negotiate the price. This will help you save money on your purchases, and it’s a great skill to have. To be a good negotiator, you need to be confident and assertive.

You also need to know your limits. Once you’ve reached your limit, be willing to walk away from the deal.

For example, spending an hour negotiating for 10 cents off with a street vendor may not be worth it. However, it doesn’t hurt to try negotiating with a travel agency for at least 5-10 minutes.

By doing so, you may be able to save a significant amount of money on your trip.

Saving money while traveling doesn’t have to be difficult. By following these pro tips, you can save money and still have a great time on your trip.

Bookmark this page so you can reference it the next time you travel. And feel free to share this with your favorite traveling buddies!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Inflation can have a significant impact on your budget, so it’s vital to adjust for it each year.

According to the NYPost, a study was conducted with results showing that “Inflation is now costing average US household an extra $296 each month”!

This blog post will go over what inflation is and how it affects each of us with eight tips on how to budget for it!

Adjust Your Budget For Inflation YouTube Video

This post may contain affiliate links; please see our disclaimer for details.

What is Inflation?

Inflation in short refers to the increase in the prices of goods and services. It measures how much the price has risen over time and tracks how the value of the currency falls due to the price increase.

The truth is that inflation is nothing new, it is around us every single day.

It’s just that recently inflation has become crazy. This has made us pay more attention to its presence.

Normally inflation increases by about 2.5% every 30 years.

But the “annual inflation rate in the US accelerated to 6.8% in November of 2021, the highest since June of 1982”. – Trading Economics

What Causes Inflation?

There are generally two causes of inflation: the first one is Demand-Pull Inflation, and the other one is Cost-Push Inflation.

Let’s walk through each one.

Demand-Pull Inflation

Demand-pull inflation can be caused when the demand for goods increases, but the supply stays the same.

When there’s a surge in demand and sellers can’t keep up with the supply, their prices will increase. The result is called demand-pull inflation.

Cost-Push Inflation

Cost-push inflation occurs when the supply of goods is low, but the demand for goods is unchanged. As a result, the prices are pushed up.

For example: when COVID-19 broke out, the global supply chain had major disruptions. Because of the lack of supply issues like computer chips, caused the car market to become very hot. The lack of lumber caused the cost of building a house to become more expensive.

How inflation affects us?

Our standard of living is mainly based on two factors: your income and expenses.

Inflation will reduce the purchasing power of income while increasing daily expenses, harming living standards.

Salaried income will only increase a little each year, but expenses will suddenly increase a lot. This creates a major negative impact on life.

Our family’s expenses increased by at least $100 monthly for our cost of living.

I currently own a little Toyota Corolla, and it has awesome gas mileage. The cost to fill up the entire tank used to be $25 but now it’s $45!! My heart reaches out to all the SUV and Truck owners out there; gas has become a major expense!

I am still shocked to see how much it costs me each time to fill up. Also, when going to the grocery store, we can tell the food price and many other items have increased significantly.

How to Adjust Your Budget for Inflation?

Budgeting is an important part of finances. It is vital for periods of high inflation.

Here are eight tips for budgeting effectively for this economic occurrence.

1) Keep Track of Inflation

The first step to budgeting for inflation is to track it. You’ll have a better idea of how much your costs are rising and can adjust your budget accordingly.

There are a few different ways to track inflation…

The Consumer Price Index (CPI) is the most common, which measures the prices of a basket of goods and services.

You can also look carefully at specific items you spend a lot of money on, like gasoline or groceries, to get an idea of how their prices have changed over time.

2) Make More Money

To keep up with inflation, you need to make more money. This could be getting a raise at work or finding a better-paying job.

It could also mean finding extra income outside your regular job, such as freelancing or investing in real estate.

By increasing your income, you are planning for a budget surplus. To thrive in finances, it’s important to have a budget surplus. This gives you the ability to save and invest in the future.

3) Cut Back on Spending

If your income isn’t keeping up with inflation, you’ll need to cut back on spending. You may need to make lifestyle changes, such as eating out less or eliminating unnecessary expenses.

Sometimes it is necessary to make tough choices, like giving up your cable TV subscription or selling your car.

4) Find Cheaper Alternatives

Even if you can’t reduce your overall spending, you may be able to find cheaper alternatives for certain items or services.

For example, if you’re paying for a gym membership that you never use, it may be cheaper to cancel it and start working out at home. Or if you’re buying lunch daily, it could be cheaper to pack a lunch from home.

There are countless to save money, so take a close look at your budget, get creative, and see where you can cut back.

5) Invest in Inflation-Proof Assets

One way to protect yourself from inflation is to invest in assets that are not affected by it. This includes things like precious metals, real estate, and collectibles.

These assets can act as a hedge against inflation, meaning they will increase in value as prices rise.

The most important thing to remember when budgeting for inflation is to stay disciplined, and calm. This means following your budget and not letting your spending get out of control.

It can be difficult to stick to a budget, but it’s important to remember that discipline now will pay off in the long run.

Inflationary environments are not the time to go on a spending spree. Because prices rise doesn’t mean you have more money to spend.

Stay disciplined and stick to your budget; you’ll be in good shape when inflation slows down.

7) Create Cash Flow Producing Assets

One of the best ways to keep up with inflation is to create assets that will produce cash flow. This could be in the form of blogs, online business or YouTube channels.

The key is ensuring that your assets produce more income than the rate of inflation. By doing this, you’ll be able to keep up with the rising cost of living and potentially even grow your wealth over time.

While there’s no guarantee that your investments will always outperform inflation, it’s still one of the best strategies for protecting your purchasing power.

So if you’re looking for ways to adjust your budget for inflation, consider creating cash flow-producing assets.

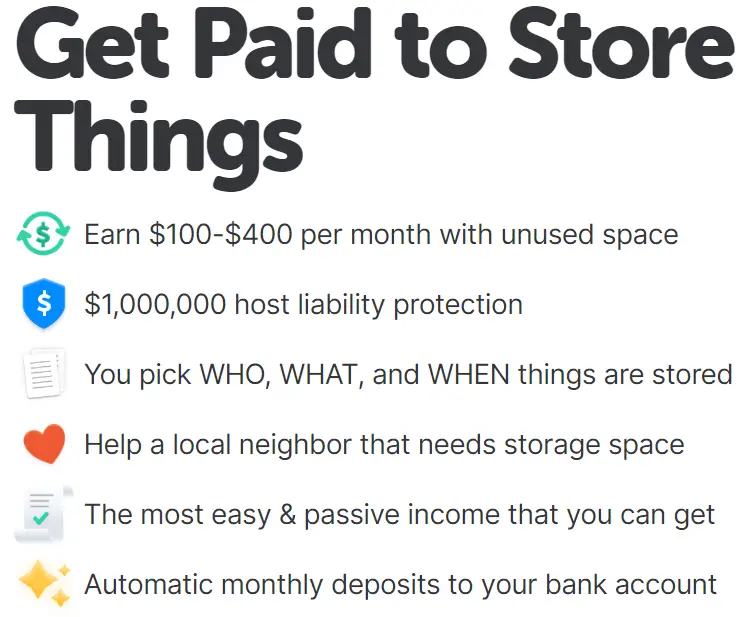

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

8) Review Your Budget Regularly

Last but not least, review your budget regularly. This will help ensure you’re on track and adjust your spending as necessary.

Reviewing your budget allows you to reflect on your progress and set new goals.

Remember that inflation can continue to rise, so it’s important to be prepared. If you take the time to adjust your budget now, you’ll be in a much better position to weather the storm.

Final Thoughts

Inflation can majorly impact your finances, but by following these tips, you can adjust your budget and protect yourself from its effects.

Stay disciplined, track inflation, and ensure you’re earning enough money to keep up with rising prices.

With a little planning, you can safeguard your finances against inflation.

For example, if the annual inflation rate were 10%, you would need to increase your income by at least 10% to keep up with inflation. You can also adjust your budget to reduce expenses by 10%.

You can also find a balance of both worlds by looking for ways to cut your expenses and increase your income.

It might seem daunting, but if you split it between increasing income and lowering expenses, you can divide the inflation burden.

It is also important to remove liabilities from your life. Some examples of this are paying off debt and unsubscribing from services that do not bring you value.

I hope this article has helped give you some ideas on adjusting your budget for inflation. Make sure to share this article with your friends and family so they can also prepare for inflation.

Make sure to share with us ways you’ve been able to budget for inflation in the comments section below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

We have all been there – a sudden desire for something that we hadn’t planned on buying, and before we know it, the item is in our shopping cart! How does this happen? Why did it happen so quickly? We are all too familiar with this type of purchase, known as an impulse buy.

A word of caution upfront is that it can be a dangerous habit to get into, but don’t fret, this article will explore the psychology behind impulse buying and provide strategies for stopping it.

This post may contain affiliate links; please see our disclaimer for details.

What is an Impulse Buy?

An impulse buy is an unplanned purchase usually made in response to a strong emotional trigger, such as excitement, happiness, or stress.

This type of buying behavior often results in regret afterward, as the buyer may not have really wanted or needed the item they purchased.

Most often, the money going to that impulse purchase is not part of a planned budget and therefore increases your overall expenses each month – yikes!

Why Do You Keep Impulse Buying?

There are several reasons why people engage in impulse buying even though they want to stop.

For some, it may be a way to cope with negative emotions like sadness or anxiety. Buying something new triggers the release of dopamine, a neurotransmitter that helps to create feelings of pleasure and satisfaction.

Additionally, people may also impulse buy as a way to celebrate or reward themselves. They may use shopping as a way to cope with boredom or relieve stress.

Others may do it for the thrill of making a spontaneous purchase. Being impulsive can be exciting and make people feel more alive. It can also be a way to stand out from the crowd or assert independence.

And still, others may feel like they need to keep up with their friends or peers who are constantly buying new things. Often referred to as “keeping up with the Joneses,” you may feel you are not good enough or do not have enough.

This type of social pressure can cause people to spend money they may not have. Marketers address this tactic as ‘Social Proof.’

Scarcity is another reason people impulse buy. The feeling of scarcity is that you need to buy something new because it may not be available later.

This type of thinking often leads to regretful purchases, as people may buy something they don’t really want or need just because they are afraid it will be gone.

Finally, a lack of delayed gratification can also lead to impulse buying. This is when people have difficulty waiting to get what they want and instead give in to the temptation of buying something immediately.

Whatever the reason, impulse buying can be detrimental to your financial health if you’re not careful.

So remember to be aware of your triggers and to have a plan in place to avoid making impulse purchases.

Why is Impulse Spending so Bad?

For one, it can put a serious dent in your budget.

If you’re not careful, you can easily spend more money than you have, which can lead to debt. Consumer debt can easily snowball into a larger problem; before you know it, you’re in over your head.

Additionally, impulse buying can be a form of compulsive spending, an unhealthy coping mechanism that can lead to financial problems.

Instead of addressing the underlying issues, compulsive spending provides a temporary fix that can ultimately make things worse.

Impulse spending can also be detrimental to your long-term financial goals. Every dollar counts if you’re trying to save up for a down payment on a house or retirement. Every time you make an impulse purchase, you risk your financial goals.

Another reason impulse spending is bad is that it can often lead to buyer’s remorse. This is when you make a purchase and then immediately regret it.

You may feel guilty, anxious, or even ashamed of your purchase. This can lead to sadness or depression, an unfortunate reality for many people today.

The final reason why impulse spending is so bad is that it can be addictive. Like anything else, the more you do it, the easier it becomes.

Once you start down the path of impulse spending, it can be hard to stop.

How to Stop Impulse Buying?

You might be admitting to yourself that you do occasionally impulse buy. First off, be proud of yourself for being honest and willing to change.

Many marketers know how to take advantage of human nature to get us to spend more money.

They use sneaky techniques like scarcity, social proof, and dopamine triggers to get us to impulse buy.

You can be better equipped to resist sales tactics by simply being aware of them.

Here are a few additional tips to help you stop impulse buying:

1) Identify Your Triggers

Pay attention to the emotions, situations, or people that lead you to make impulse purchases. You’ll become more aware of when you are most likely to spend money impulsively.

Ask yourself the following questions:

Are you someone that needs social validation?

Does scarcity cause you to fear missing out?

Do you tend to make impulse purchases when you’re bored or feeling down?

Once you know your triggers, you can be more mindful of them and take steps to avoid them.

2) Get Ahead of the Temptation

If you know you will be in a situation where you may be tempted to spend money, plan ahead. You could bring a set amount of cash or leave your credit cards at home.

Credit cards are often used for impulse buying because they do not cause the same pain receptors to go off as paying with cash.

You do not physically see the money leaving your hands when you use a credit card.

Unless you have great self-control, maybe stick to cash until you can handle your finances better.

4) Budget for Things that Matter Most

Having a budget will help you become more aware of your spending and make it easier to stick to your financial goals. It’s okay to enjoy yourself and have an expense category for that, but make sure what you buy will add lasting value to your life.

When you have a budget, you can allocate funds for specific purposes and know how much you have available.

I wrote another article sharing How The 50/30/20 Rule Works (With Examples). This is another common budgeting technique to help you better know which categories your mone is landing in.

4) Prepare a List Before Shopping

When you go shopping, bring a list of the items you need. This will help you stay focused on your purchases and avoid buying things you don’t really need.

Stick to the list! Do your best not to add anything unessential.

5) Avoid Sales and Discounts for Wants

Sales and discounts can be tempting but can lead to overspending. If you try to stick to a budget, it’s best to avoid sales and discounts altogether. This means unsubscribing from promotional emails and ignoring in-store sales.

Looking for an easy way to manage subscriptions? Look no further than ROCKET MONEY. We love how they provide you with the tools to track spending, lower bills, and track your net worth!

Remember that when you buy a $100 item for 50% off, you do not save $50. You still spent $50. This could harm your finances if you do not need that item.

6) Take a Break

If you feel like you are about to make an impulse purchase, take a step back and give yourself some time to think.

Sometimes, all you need is a few minutes to cool down before you make a decision.

The 30-day rule is a good guideline to follow. If you can wait 30 days to make a purchase, chances are you don’t really need it.

7) Avoid Shopping When Unhappy

If you are feeling sad, angry, or stressed, avoid shopping. These emotions can lead to impulsive spending. If you need to shop for something, wait until you are in a better mind.

Advertisers can also use emotion through ads that trigger feelings of inadequacy, sadness, or insecurity.

8) Avoid Shopping When Tired

There is a reason why infomercials often air late at night. When we are tired, we are more likely to make bad decisions. Shopping when you are exhausted is a recipe for disaster.

If you feel sleepy while shopping, put down your credit card and go home. You will thank yourself in the morning. If you watch a late-night TV infomercial, turn it off and get some rest!

9) Talk with Someone, Set Goals Together

If you are struggling with impulse buying, contact a friend or family member for support.

Ask them what they think of the purchase. It can be beneficial to ask them to play devil’s advocate and argue why you should not make the purchase.

Talking to someone can help you gain perspective and make a more informed decision.

All in All

Making impulse purchases can harm your financial health, but it doesn’t have to be this way. If you are aware of your triggers and have a plan in place, you can avoid making these purchases.

You can stay on track with your financial goals with effort and self-control. And if you have friends or family that impulse buy, share this article with them!

Making impulse purchases is something that we have all done at one point or another. Whether it’s buying that new dress we saw in the store window or picking up a new gadget that we have to have, we’ve all been there.

But there are ways to combat this psychological pull. If you impulse buy, bookmark this article to review if you need a refresher on avoiding future purchases.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

It’s happened to all of us at some point. You purchase something then a few days or weeks later; you start to regret it. Maybe the item wasn’t what you expected, or maybe the price was too high. This feeling is known as buyer’s remorse and can be pretty darn unpleasant.

In this blog post, we will discuss buyer’s remorse, how to avoid it, and some tips for making sure you don’t regret your purchases.

This post may contain affiliate links; please see our disclaimer for details.

What Is Buyer’s Remorse?

Buyer’s remorse is defined as “the sense of regret after having made a purchase”. It’s that sinking feeling you get when you think about how much money you just spent – and whether or not it was worth it.

According to Finder.com, 64% of adults who purchased during black Friday sales experience buyer’s remorse.

Most companies will not offer returns or refunds on items that have been used, so it’s important to be 100% sure about your purchase before you make it.

What does buyer’s remorse feel like?

For some people, buyer’s remorse can be a mild feeling of regret or disappointment. For others, it can be an all-consuming feeling of anxiety and dread.

If you’ve ever made a major purchase – like a car or a house – and felt sick to your stomach afterward, you know what we’re talking about.

Ten tips to Prevent Buyer’s Remorse

Experiencing buyer’s remorse does not feel good; in many cases, it is already too late to receive a refund. Even small purchases can cause buyer’s remorse if you’re not careful.

So prevention is key!

Here are our top tips on how to avoid buyer’s remorse:

1) Take the time to research

When it comes to making any purchase, research is essential. You should know exactly what you want and your options before entering a store or browsing online.

If you’re unsure whether to buy something, take the time to do your research first.

Read online reviews, talk to friends or family members who may have purchased the same item, and get as much information as possible. Doing this will help you make an informed decision and avoid buyer’s remorse later.

You should also research their business practices. Buyer’s remorse can often occur due to a depreciation of initial perceived value, but it can also arise if you find out that the company has unethical business practices.

2) Set a budget and stick to it

Before you start shopping, set a budget and make sure you stick to it. It’s easy to get caught up in the moment and spend more than you intended, so having a spending limit will help keep you in check.

You can also use various budgeting methods such as the envelope system to help you stay on track.

3) Consider the long-term cost

When making a purchase, it’s important to consider the long-term cost, not just the upfront price.

For example, factor in fuel costs, insurance, and maintenance if you’re buying a car. These purchases can become long-term liabilities rather than one-time expenses.

The same goes for big-ticket items like appliances and electronics – think about how much it will cost to use and maintain them over time.

However, if an item service will save you time and energy or give you peace of mind, it can be a good investment. This is because your time is also valuable and has a cost.

If something only brings you joy for a few minutes, it may not be worth it. Some examples may be an item that is popular but not long-lasting, such as fast fashion, fast food, and short-term gym memberships.

However, this is just a guideline and not a rigid expectation. For example, a two-hour movie and ice cream may not seem like it’s worth it. However, if you are experiencing it with someone you love, it can be worth it.

Some memories are priceless. This is also true for a two-hour networking event. If you meet someone that could lead to your dream job, it would be worth the investment.

4) Wait 24 hours before finalizing your purchase

First, wait 24 hours before finalizing your purchase. This will give you time to consider whether you need the item and whether it’s worth the price.

If you’re still thinking about it after 24 hours, that’s a good sign that you should buy it. But if you’ve changed your mind, it’s probably not worth your money.

5) Use cash instead of credit

If you have difficulty with self-control, use cash instead of credit when making a purchase. Doing so will help you stay within your budget and avoid debt.

Plus, studies have shown that people are more likely to experience buyer’s remorse when they use credit cards because they don’t “feel” the pain of paying with cash.

6) Avoid impulse buys

An impulse buy can be defined as “a spontaneous decision to buy something, without any prior thought or planning.” In other words, you buy something on a whim without giving it much thought.

Impulse buys are often driven by emotions like excitement, happiness, or even sadness. And while they can be satisfying at the moment, they usually lead to regret later.

To avoid impulse buying, take a step back and ask yourself if you need the item. If you can wait 24 hours to buy it, that’s usually a good sign that it’s not an essential purchase.

By combining these tips on this list, you are better equipped to fight off buyer’s remorse!

7) Compare prices before you buy

Before you make a purchase, take some time to compare prices from different stores or websites. You might be surprised at how much you can save by researching.

8) Read the return policy

Before you buy anything, make sure you read the store’s return policy. This will help you know what your options are if you end up regretting your purchase.

Some stores have a no-returns policy, so it’s important to be aware of this before you make a purchase. Being aware that you won’t be able to return it can make you think twice about creating an experience of buyer’s remorse.

9) Shop for quality, not appearance

When you’re out shopping, buying something solely because it looks good can be tempting. But before you make a purchase, always ask yourself if the item is well-made and will last.

Instead, spend a little more on something that will stand the test of time than to have to replace it every few months. Quality should always be your top priority.

For example, if you wish to save money on your appearance, focus on exercise, nutritious eating, and stress management. These practices are often much less expensive than plastic surgery, tons of makeup, and expensive jewelry.

By becoming a higher quality person through character traits and values, your appearance will increase without the high costs.

Quality can also help prevent wear and tear and allow for prolonged use. For example, a $500 designer t-shirt may look great, but they usually last just as long as a nice fitting $5 t-shirt.

Unfortunately, many people feel buyer’s remorse once they realize that their desire to appear of high status has cost them more money than necessary.

By reading articles on this website, you are investing your time in quality, and it is free of cost. Your quality will increase, and it won’t be just for appearance. This is an excellent way to save money and increase your quality of life!

Salespeople are trained to use certain techniques to get you to buy something on the spot. They may try to create a sense of urgency by saying that the sale ends today, or they may offer a discount if you buy now.

If you feel like you’re being pressured into buying something, take a step back and ask yourself if it’s something you need or want.

You can always come back later – the “sale” will still be going on.

All in All

Buyer’s remorse is not a fun experience. Your hard-earned money is suddenly gone, and you are left with regret.

Hopefully, by following the tips on this list, you can start to avoid buyer’s remorse in the future.

Remember to take your time, research, and always think twice before making a purchase.

Make sure to share this article with your friends and family to help them avoid feeling buyer’s remorse!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Zero-based budgeting has been around for a long time, but it has become increasingly popular in recent years.

The concept is quite simple: every dollar of revenue must be justified by a dollar of expense.

Using this approach can be used in businesses of all sizes, and it can help you find ways to save money and improve your bottom line.

It can also be used for personal finances.

If you are looking to get your finances in order, a zero-based budget can be a helpful tool.

This article will discuss zero-based budgeting, including how it is and how to make one, the pros and cons of this approach, and the bottom line.

This post may contain affiliate links; please see our disclaimer for details.

So What is Zero-Based Budgeting?

Zero-based budgeting (ZBB) is an approach to budgeting in which all expenses must be justified for each new period.

In other words, it’s a “fresh start” approach that requires every expense to be approved anew rather than simply carrying over previous budget amounts.

Zero-based budgeting aims to ensure that every dollar in the budget is allocated toward achieving specific objectives.

Implementing this type of budgeting can benefit businesses or organizations seeking to optimize their spending and get the most out of their resources.

If you have a surplus of income, you should have a plan ready for how you will allocate that money.

Let’s illustrate with an example, if your income is $4000 and your expenses are $2000, then you have a surplus of $2000.

You can direct $1000 to your savings account and $1000 to your investment accounts.

The key takeaway is that you have an exact plan for how every single dollar will be used to improve your financial future.

Zero-Based Budget Example

To better understand how zero-based budgeting works, let’s explore an example.

Let’s say you have a monthly budget of $500 for groceries.

In a zero-based budget, you would start with that $500 and allocate every dollar to specific items based on your needs and wants.

So, you might break down your budget like this:

$200 for essentials like food, toiletries, etc.

$100 for eating out

$50 for coffee

$50 for snacks

$100 for household supplies.

Here’s what it would look like for a business with a marketing budget of $4500:

$2000 for website design

$1000 for print ads

$500 for online ads

$250 for signage

$250 for public relations

$500 for miscellaneous expenses.

These are just two examples of how a zero-based budget can be applied.

Let’s explore ways to make a zero-based budget and dive deeper into the pros and cons of this budgeting system.

How to Make a Zero-Based Budget

The first step in making a zero-based budget is to track your spending for some time so that you have a clear idea of where your money goes each month.

You can do this by looking at your bank and credit card statements or using a budgeting app like Mint or YNAB.

Once you know your spending patterns, you need to set some goals for your zero-based budget.

Do you want to save more money? Pay off debt? Spend less on non-essentials?

After you’ve set your goals, it’s time to start allocating your incometo different categories. Here’s an example:

Transportation: $200 (car payment, gas, public transportation)

Food: $500 (groceries, eating out)

Debt payments: $400 (student loans, credit cards)

Savings & Investing: $200

Personal spending: $200 (clothes, entertainment, etc.)

As you can see, in this example, every dollar of the monthly income has been allocated to a specific category. This is what a zero-based budget looks like.

It can be helpful to use a budgeting app or spreadsheet to track your income and expenses to see how much money you have left in each category after you’ve paid your bills. This will help you stay on track with your zero-based budget.

Another important tip to keep in mind is that a zero-based budget is not static. Just like any other type of budget, it will need to be adjusted from time to time as your income and expenses change.

Finally, don’t forget to give yourself some wiggle room in your budget.

No one is perfect, and there will be months when you overspend in one category or another.

Just make sure that you adjust your budget for the following month to stay on track overall.

Pros of Zero-Based Budgeting

There are many benefits to using a zero-based budget.

First, it forces you to think about every expense and whether or not it is vital. This can help you cut down on unnecessary spending and save money.

Second, it helps you align your spending with your goals and priorities. When you know your goals, it is easier to choose where to allocate your resources.

Another benefit of zero-based budgeting is that it can help you pay off debt faster. You can get out of debt sooner by allocating more of your income to debt payments.

This budgeting strategy will also help you build up your savings so that you have a cushion to fall back on in an emergency. By consistently directing money into savings, you can grow your account quickly.

Zero-based budgeting can also help simplify your finances. When everything is mapped out and you have a plan for your money, it is easier to stay on top of your finances and avoid financial stress.

Finally, zero-based budgeting can help you save money by forcing you to plan for future expenses.

When you know exactly what bills are coming up and how much money you need to save, it is easier to stay on track.

By thinking about your future, you are developing delayed gratification. This can be a difficult concept for some people, but it is important if you want to be successful with money.

If you struggle to stick to a budget, zero-based budgeting may be a good option.

It can help you become more mindful of your spending and make better choices about where to allocate your money.

While there are many advantages to using a zero-based budget, there are also some challenges that you should be aware of.

First, it can be time-consuming to track every single expense and ensure that it is accounted for in your budget. This is especially true with inflation and rising consumer goods costs.

Second, it can be difficult to stick to a zero-based budget if you have irregular income or expenses. This is because a zero-based budget works best when you know how much money you have to work with.

Without this information, it can be easy to overspend or underspend in certain categories.

The cost of groceries may be the same for months, but some economic factors may cause several rising costs over a series of months.

For example, a war may cause gas prices to rise suddenly, or a supply chain issue can increase grocery bills.

If every dollar was assigned to a fixed expense, this could be a problem when unexpected price increases occur.

Another downside to zero-based budgeting is that it can be difficult to stick to in the long run.

This is because it requires a lot of discipline and self-control. If you are not used to tracking your spending, it can be easy to let your budget slip.

Finally, if you are not careful, you may cut out necessary expenses to save money.

Budgeting is essential, but by budgeting too tightly, you risk being rigid and uncreative with wealth-building strategies.

Being disciplined is important, but remember to have some flexibility in your budget.

Zero-based budgeting may not be the best choice for everyone.

But if you are willing to put in the time and effort, it can be a helpful tool for managing your finances.

The Bottom Line

Zero-based budgeting is a powerful tool to help you save money and reach your financial goals.

However, it is important to be aware of the challenges that you may face when using this budgeting method.

If you are willing to put in the time and effort, a zero-based budget can greatly improve your financial situation.

Start by evaluating your spending habits and see where you can cut back.

Then, create a plan for using the extra money in your budget to reach your financial goals.

With careful planning and execution, zero-based budgeting can be a helpful tool on your journey to financial success.

If you struggle to make ends meet or have no idea where your currency is flowing, a zero-based budget will give you a much-needed wake-up call.

Following these steps may be difficult at first, but once you get used to it, zero-based budgeting can help you take control of your finances and reach your financial goals.

Looking for an easy way to manage subscriptions? Look no further than ROCKET MONEY. We love how they provide you with the tools to track spending, lower bills, and track your net worth!

If you know anyone struggling with their finances, feel free to share this article with them.

Bookmark this page to refer back to when creating your zero-based budget.

Remember that this website is filled with wealth-building information, so explore other articles for enjoyment and education!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.