Are you looking for a rule of thumb to help you figure out how much money you need to be saved for retirement? If so, you may have heard of the 25x Rule.

This rule states that you should aim to have 25 times your annual living expenses saved by the time you retire. While there are no guarantees regarding retirement planning, the rule of 25 is a good starting point for most people.

This article will discuss the rule, how it works, and why it can be a helpful guideline for retirement savings. So, if you’re curious about the rule of 25, read on!

This post may contain affiliate links; please see our disclaimer for details.

What Is the 25x Rule for Retirement?

The 25x rule for retirement is a guideline that suggests you should aim to have 25 times your annual cost of living saved. This method is from the financial planning community and is based on the idea that you will need to have enough money saved to withdraw approximately four percent of your nest egg each year.

The rule provides a general guideline for how much you should have saved. It is not meant to be an exact formula but a starting point for your retirement planning.

The number 25 is used because it is believed to be a safe withdrawal rate at 4%. This should leave you with 30 years’ worth of income to cover your costs in retirement.

This percentage is based on historical data and research on retirement planning. The average annual return from the stock market is around 10.5%, but this number can fluctuate.

So, with a 4% withdrawal rate, you would have a greater chance of not running out of money in retirement. That’s even factoring in the possibility of the stock market taking a downturn.

Withdrawing four percent of your nest egg each year should give you enough money to cover your living costs. It also allows your savings to last for at least 25 years in retirement; pretty cool right?

Most people retire at 65, so the 25x Rule is meant to make your money last throughout your retirement.

How Does The Rule of 25 Work?

The way the rule of 25 works is pretty simple. You take the age you plan to retire and multiply it by your current annual salary.

Let’s say you want to retire at 65 and make $50,000 per year. To live comfortably, you will need 25 x $50,000 = $1,250,000 annually.

The rule of 25 is a guideline to help you know how much money you should have saved for retirement by the time you reach a certain age. This would give you 40 years to save for retirement if you started saving at 25.

However, this rule of thumb doesn’t work for everyone. Several factors can affect how much money you will need in retirement. Some examples are lifestyle, health, and whether you plan to retire early.

If you want to retire at 55 instead of 65, you will need to save more money. You would have a shorter time frame to save for retirement. Thus, you would also need to account that you may live longer in retirement than someone who retires at 65.

You may also need to save more money if you have a more lavish lifestyle. A giant nest egg is needed to cover your costs in retirement.

Health is another factor to consider. If you have good health, you may need less money in retirement than someone with health issues. You would have more money to cover other costs with fewer medical bills.

The rule of 25 is a helpful guideline, but it’s essential to remember your circumstances. Having this clear picture of your situation will affect how much money you need to save.

It works (most of the time), but some variables can change the amount of money you need to save.

Why the 25x Rule Works (Most of the Time)

The main reason why the 25x rule works is that it’s based on a very solid foundation: the basic principles of saving and investing.

When you save money, you’re essentially putting your money into a “pot” that you can use later down the road.

The same principle applies to investing. When you invest your money, you’re essentially putting your money into a “pot” that will grow over time.

The goal of saving and investing is to grow your pot of money so you can eventually use it for something important, like retirement. We personally love index funds since they minimize risk and, historically speaking, have performed well with an average increase.

Now, the reason why the 25x rule works most of the time is that it takes into account two very important factors: inflation and investment returns.

Inflation is the natural tendency for prices to go up over time. This is why groceries and gas cost a little bit more each year.

Investment returns are the money that you earn from investing your money.

For example, if you invest $100 in stock and it goes up by $20, your investment return would be 20%. The 25x rule considers both of these factors when calculating how much money you need to save for retirement.

It doesn’t sometimes work because the inflation rate can increase or decrease over time, and the same goes for investment returns.

If inflation increases faster than expected or investment returns are lower than expected, you may need to save more than 25x your annual expenses.

It can be challenging to predict what inflation and investment returns will be like in the future, which is why the 25x rule is just a guideline and not an exact science.

As we mentioned earlier, other factors such as your lifestyle, health, and retirement age can also affect how much money you need to save.

It’s always important to remember that your circumstances will ultimately determine how much money you need to save for retirement. That’s why the 25x rule is just a guideline, not a hard-and-fast rule.

The Rule of 25 vs. the 4% Rule: What’s the Difference?

The 4% rule indicates that you can withdraw 4% from your retirement and expect that the returns from your investment will surpass the withdrawal rate.

The problem is that with inflation added to this equation, the purchasing power of your money will decrease over time. This means that if you withdraw 4% and the inflation rate was at 8% last year, you’re withdrawing 12% in purchasing power.

If the growth of your investment were less than 12% last year, then you would have to begin dipping into your principle, which is not ideal. This is where the multiply-by-25 rule comes in.

The rule of 25, on the other hand, is a general guideline that suggests you multiply your total salary by 25 to determine how much money you need to save for retirement.

This rule of thumb assumes that you will want to replace your current income via investments during retirement.

It also factors in an estimated annual return of around 10.5% but is used for calculating how much total principle you’d need for retirement. It helps to build a mental framework for those pursuing financial freedom.

The 4% rule calculates how much you can withdraw from your principal after the 25x rule is put into place.

For example, first, you would use the 25 rule to calculate how much you need to have saved. Then, the four percent rule would tell you how much you can withdraw from that savings account each year. The 25x rule is a good starting point, but the 4% helps ensure you don’t outlive your money.

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

The rule of 25 can be a helpful way to estimate how much money you need to save for retirement. Remember it is a guideline and to be flexible when creating your own financial plan.

Everyone’s retirement savings needs are different and will depend on factors such as your desired lifestyle in retirement and how long you expect to live.

If you’re unsure how much money you’ll need in retirement, several online calculators can help you estimate your specific retirement savings needs.

When saving for retirement, the earlier you start, the better. So, if you haven’t started saving, now is the time!

The sooner you start saving, the more time your money will have to grow, and the less you’ll have to save each month.

If you’re already saving for retirement, stay on track to reach your goals by regularly reviewing your savings plan. This will help you ensure you’re still on track and make any necessary adjustments to ensure you have enough money saved when it’s time to retire.\

As always, thank you so much for reading. We’d love to hear your thoughts in the comments section below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Do you want to retire early? The 4% rule is a common guideline that can help you achieve this goal.

The 4% rule states that you should withdraw no more than 4% of your retirement savings (nest egg) each year to ensure that it lasts throughout your retirement.

This article will explain the 4% rule in more detail and discuss some pros and cons of using this guideline.

This post may contain affiliate links; please see our disclaimer for details.

What Is The 4% Rule?

The 4% rule is a guideline that suggests that you withdraw no more than four percent of your portfolio value each year during retirement. The money you take out can go towards living expenses or other things, such as travel or gifts. The rule is meant to help ensure your retirement funds last without having to go back to work.

Some experts suggest using a slightly lower withdrawal rate, such as three percent or even two and a half percent, especially if you’re retired for 20 years or more.

Regardless of your withdrawal rate, it’s important to remember that the 4% rule is just a guideline.

It’s not set in stone, and there will be years when you may need to adjust your withdrawals up or down based on market conditions and circumstances.

This leads to the importance of having a 2-year emergency fund that can cover all expenses if there is a large drop in the market.

What is the Purpose of the 4% Rule?

Simply put, the purpose of the 4% rule is to help ensure that your money lasts throughout retirement.

This is especially important if you plan to retire for 20 years or longer.

The 4% rule is based on the work of William Bengen, a financial planner who wrote a paper in 1994 about safe withdrawal rates from retirement portfolios.

Bengen looked at historical data to see how different portfolio types and withdrawal rates would have fared over time.

He concluded that a portfolio consisting of 50% stocks and 50% bonds would have had a 95% chance of lasting 30 years if the investor withdrew no more than four percent per year.

How Does The 4% Rule Work?

The rule is simple:

You can only withdraw 4% of your retirement account per year.

If your retirement account is $100,000, you can withdraw $4000 per year.

Now you might be thinking, that’s not a lot of money. And you’re right, it’s not.

But the goal of the 4% rule is to make sure your money lasts throughout retirement, even if you live for 30 years or more.

The rule is based on the idea that your portfolio will grow over time and that the money you don’t withdraw will continue to grow and provide for you in retirement.

There are a few things to remember with the four percent rule.

First, it’s based on historical data and may not hold in the future.

Second, it’s a guideline, not a guarantee – you may need to save more or less depending on your individual circumstances.

For example, if you’d like a more comfortable retirement, you can set a goal of $1,000,000 in your retirement account. With the 4% rule, you could withdraw $40,000 per year!

Finally, it assumes that you will withdraw 4% of your savings each year in retirement, which may not be the case.

Despite these caveats, the 4% rule is a helpful way to estimate how much you need to save for retirement.

By following this rule, you can ensure that you are on track to reach your retirement savings goal.

Using The 4% Rule With An Investment Portfolio

To successfully use the 4% rule, it would need to be in an investment portfolio.

This is because the rule is based on the idea that your portfolio will grow over time, and you can withdraw four percent of the value each year without depleting your savings.

For example, if you’re 30 years away from retirement, the fund may be 90% stocks and just 10% bonds. But if you’re only five years away from retirement, it might be 50% stocks and 50% bonds.

This gradual shift helps to protect your savings while still allowing you to grow your money over time.

The most effective fund for the 4% rule is the S&P 500 Index Fund. On average, the S&P 500 grows at 11.5% per year.

Here is an example of calculating how much you’d need to retire comfortably using the 4% rule with the S&P 500.

The first step would be to decide how much income you’d need to live a financially free life.

The average cost of living for a U.S. citizen is approximately $1100 per month but let’s go with $2000 to be conservative and plan for a great retirement!

To receive a retirement income of $2000 per month ($24,000 per year), you’d need $600,000 invested into your S&P 500 account.

Now let’s see how long it would take to reach our goal of $600,000 using the historical growth rate of the S&P 500 at 11.5% annually.

$600,000 might seem like a lot, but with the power of compound interest and consistent monthly contributions, you can get there with just $121,000 as a total investment.

If you start with $1000 and invest $400 per month into an S&P 500 index fund, it would take 25 years to reach the goal of $600,000. But if you started investing at 25 years old, you could retire with an income of $24,000 at 55 years old!

If 25 years is too long, you can get there in only 15 years with monthly contributions of $1400. As you can see, there are many different variables that you can adjust to make the four percent rule work for you.

The Bottom Line: By calculating your desired income, you can find a retirement number that is comfortable for you.

The important thing to remember with the four percent rule is to start saving early and invest often!

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

What Are The Pros And Cons Of The Four Percent Rule?

There are pros and cons to using the four percent rule as a retirement guideline.

Some of the pros include:

It’s simple to understand and follow.

You can adjust your withdrawals up or down as needed based on market conditions and your circumstances.

It’s a helpful way to estimate how much you need to save for retirement.

It uses the stock market’s ability to grow to your advantage.

Some of the cons include:

It’s based on historical data and may not hold true in the future.

It’s a guideline, not a guarantee – you may need to save more or less depending on your circumstances.

It assumes that you will withdraw four percent of your savings each year in retirement, which may not be the case.

The large number needed can seem overwhelming.

Common Mistakes With The 4% Rule

Regarding retirement planning, the “four percent rule” is a guideline that’s often cited.

The rule of thumb goes like this: If you withdraw four percent of your nest egg each year during retirement, you’re unlikely to run out of money.

But as with any rule of thumb, there are exceptions – and the four percent rule is no exception.

People make several common mistakes when using the four percent rule. Here are eight of the most common:

Mistake #1 – Not Adjusting for Inflation: One mistake people often make with the four percent rule is not adjusting for inflation.

When you retire, your expenses will likely go up – not down. That’s why it’s important to factor in inflation when withdrawing money from your nest egg.

Mistake #2 – Not Taking Into Account Your Longevity: Another mistake people make is not considering their longevity.

Just because the average life expectancy is around 78 years doesn’t mean that’s how long you will live.

If you want to be safe, plan for a longer retirement.

Mistake #3 – Not Planning for Unexpected Expenses: People do not plan for unexpected expenses.

Retirement is often unpredictable, and you may need more money than you think.

Make sure to have a cushion in your nest egg so you can cover any unexpected costs that come up.

Mistake #4 – Failing to take into account your own individual circumstances: The four percent rule is a guideline, not a definite rule.

Your retirement plan should be unique to you and consider your circumstances.

Mistake #5 – Assuming that you will have the same expenses in retirement as you do now: Retirement is often a time when people have time to spend money on things like travel and hobbies that they didn’t have time for while working.

As a result, your expenses in retirement may be different than they are now.

Mistake #6 – Not factoring in Social Security: If you’re eligible for Social Security, be sure to factor this into your retirement plan.

Social Security can provide you with a source of income in retirement, which can help reduce the amount you need to withdraw from your nest egg.

Mistake #7 – Withdrawing in tax-inefficient ways: People do not consider the taxes they’ll owe on their withdrawals.

If you’re not careful, you could owe more in taxes than you need to.

That’s why investing with a tax-efficient account is important from the start.

Mistake #8 – Not having a plan B: Another mistake people make is not having a backup plan. What if the market crashes and your nest egg takes a hit?

What if you live longer than expected and run out of money?

Having a plan B can help you weather any storms that come your way in retirement.

As mentioned previously, we highly recommend having a fully funded emergency fund that can cover all expenses in case of a market crash.

The Bottom Line:

If you avoid these mistakes, you’ll be well on your way to a successful retirement.

Just remember to factor in inflation, plan for long life, and have a cushion for unexpected expenses.

You can make the four percent rule work with those three things in mind.

The Rule of 25 vs. the 4% Rule: What’s the Difference?

The Rule of 25 vs. the 4% Rule

The 4% rule indicates that you can withdraw 4% from your retirement and expect that the returns from your investment will surpass the withdrawal rate.

The problem is that with inflation added to this equation, the purchasing power of your money will decrease over time. If you withdraw 4% and the inflation rate was at 8% last year, you’re withdrawing 12% in purchasing power.

If the growth of your investment were less than 12% last year, then you would have to begin dipping into your principal, which is not ideal. This is where the multiply-by-25 rule comes in.

The rule of 25, on the other hand, is a general guideline that suggests you multiply your total salary by 25 to determine how much money you need to save for retirement.

This rule of thumb assumes that you will want to replace your current income via investments during retirement.

It also factors in an estimated annual return of around 10.5% but is used to calculate the total principal you’d need for retirement. It helps to build a mental framework for those pursuing financial freedom.

The 4% rule calculates how much you can withdraw from your principal after the 25x rule is implemented.

For example, first, you would use the 25 rule to calculate how much you need to have saved. Then, the four percent rule would tell you how much you can withdraw from that savings account each year. The 25x rule is a good starting point, but the 4% helps ensure you don’t outlive your money.

Common Questions About The 4% Rule

Q: How long will it take to retire if I follow the rule?

A: This depends on how much money you have saved and how much you can save each year.

Use the example mentioned above and adjust the variables to your preference.

Q: What happens if my retirement lasts more than 30 years?

A: If you want to retire sooner than 30 years, you will need to invest more each month. This is because compound interest will build more reserves for retirement.

You can also consider withdrawing only 2% rather than 4% to allow your investments to keep growing beyond 30 years.

Q: What if I can’t save enough money to retire?

A: If you cannot save enough money to retire using the four percent rule, there are a few options you can consider.

One option is working part-time in retirement. This can help supplement your income and give you something to do in retirement.

Another option is to downsize your lifestyle. Doing so will reduce your expenses and free up extra cash to help fund your retirement.

Lastly, you can delay retirement. This may not be ideal, but it can give you more time to save money and prepare for retirement.

Q: Is the four percent rule a guaranteed way to retire?

A: No, the four percent rule is not a guaranteed way to retire. It is simply a guideline that many people with success have used.

There are no guarantees in life, so it is important to remember that anything can happen when following this rule.

In Summary

The four percent rule is a simple estimate of your retirement savings needs.

Remember to take into account your circumstances when using this guideline.

With careful planning and consistent investing, you can ensure a comfortable retirement for yourself down the road.

Thanks for reading!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

As with this image, you will need to tear back certain parts of your life or make changes to find Financial Freedom.

What does financial freedom mean to you? Is it being able to afford whatever you want without having to worry about money? Or is it something else entirely?

In reality, financial freedom is different for everyone. For some, it might mean living a comfortable life without any debt. For others, it might mean being able to retire early and travel the world.

The important thing is that financial freedom means something different to each individual and everyone can achieve it.

So, how do you go about achieving financial freedom? Read on to find out!

There are many different paths to financial freedom. Some people achieve it through hard work and disciplined saving, while others come into money through investing or inheritances. No matter how you reach financial freedom, the important thing is that you have a plan and you stick to it.

Can you achieve financial freedom?

The short answer is yes! Financial freedom is possible for almost everyone, no matter your current situation.

So whether you’re struggling to make ends meet or already comfortable, you can always make changes to improve your financial situation. It might not be easy, but it is possible.

The key to achieving financial freedom is to have a plan and to be disciplined. You need to know your goals and what you’re willing to sacrifice to reach them.

For some people, that might mean cutting back on unnecessary expenses and saving as much money as possible. For others, it might mean taking on additional work or investing in high-yield investments.

For us, the Biesingers, Financial Freedom is living on our terms. Having enough money in savings and investments that we can pivot or change what we do for work or stop working entirely. We believe that flexibility allows us more opportunities to feel peace and happiness.

Let’s turn our attention to how you can obtain financial independence:

Understand your current financial situation

When it comes to financial freedom, the first step is always the hardest. But the journey becomes much easier once you take that first step.

The first step is to take stock of your financial situation. This means listing all of your debts and savings.

Once you have a clear picture of what you owe and have saved up, you can develop a plan to pay off your debts and grow your savings.

One strategy for reducing debt is first to pay the debt with the highest interest rate or try the Debt Snowball Method. Another method for growing your savings is setting up automatic transfers from your checking account to your monthly savings account.

Have clear goals that you can achieve

The second step to achieving financial freedom is to set clear goals. This means knowing what you want to achieve and when you want to achieve it.

For example, do you want to be debt-free in five years? Do you want to retire at age 60?

Perhaps what you what to achieve is financial independence and retire early. Whatever your goals may be, make sure that they are realistic and that you have a plan for achieving them.

To help you understand how much you may need for retirement, you can check out our other blog posts about the 4% rule or the 25x rule.

Be disciplined with your spending

The third step to achieving financial freedom is to be disciplined with your spending. This means knowing what you can and cannot afford and sticking to a budget.

It can be challenging to stick to a budget, but it is possible.

Many helpful resources are available, such as online budget calculators and financial planning apps.

You can’t just be disciplined regarding spending; you need to track every cent you spend. This means knowing where your money is going and ensuring you are not spending more than you can afford.

You can’t get a good picture of your financial situation if you don’t know where your money is going.

Spend far less money than you earn

The goal is to spend far less than you earn to save as much money as possible. This can be difficult, but it is possible.

There are many ways to save money, such as couponing, setting a budget, and cooking at home.

You also need to ensure you are not spending money on unnecessary things. For example, don’t buy anything on credit that you don’t have to.

The interest on credit card debt can quickly add up and make it difficult to get out of debt.

Have an emergency fund

Life can always throw you a curveball, no matter how well you plan. That’s why it’s crucial to have an emergency fund to cover unexpected expenses. This fund should be used for medical bills, car repairs, or job loss.

Your emergency fund is there to protect you from financial ruin, so don’t dip into it unless it is necessary.

I created another article sharing on everything you need to know about Emergency Funds.

Invest in yourself to become financially independent

It can’t be stressed enough that you must invest in yourself if you want to become financially independent. You should consider investing in college or learning a trade to earn more money.

You’ll never succeed in becoming financially independent or retiring early if you don’t have a skill that enables you to earn more money than the average person.

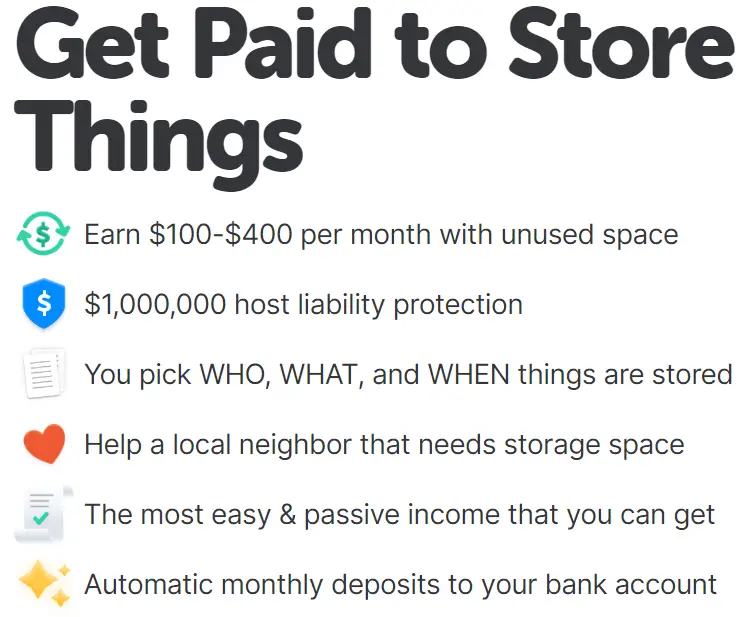

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

Start your own business

One of the best ways to achieve financial freedom is to start your own business. This can be a difficult and risky endeavor, but it can also be very rewarding.

When you own your own business, you control your financial destiny. This means you can earn a lot of money if your business succeeds.

Of course, starting your own business could be something you do on the side. It takes a lot of hard work, dedication, and some risk-taking. But if you are up for the challenge, it can be a great way to achieve financial freedom.

One of the most crucial steps: Paying off debt

Carrying around debt is like having a weight tied around your neck. It can be incredibly stressful and difficult to achieve your financial goals.

That’s why paying off your debt is one of the most important steps to becoming financially free.

There are a few different ways to pay off debt, such as using a debt consolidation loan or making extra payments on your debts.

Whichever method you choose, ensure you are dedicated to getting out of debt as quickly as possible.

Every person reading this can become financially independent

It’s true; every single person reading this can become financially independent. Of course, it will take work, dedication, and discipline, but it isn’t as complicated as you think.

If you are willing to put in the effort, you can achieve financial freedom. It is not an impossible dream; it is within your reach.

The difference between those who achieve financial independence and those who don’t is simply a matter of choice. You’ve got this; we’re rooting for you!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Anyone seeking financial freedom to retire early or FIRE knows that many options exist to save and invest money. Today I’m excited to share with you 16 ways to help you reach FIRE faster!

The question is, what’s the best way to go about it? The problem is that there’s no one-size-fits-all answer, as the best method depends on each person’s unique circumstances.

That said, there are still some critical steps that can help anyone on the path to FIRE.

This post may contain affiliate links; please see our disclaimer for details.

1. Decide how early you want to retire

At what age do you want to be financially independent? Are you talking about retiring at 40 or maybe 60? The answer to this question will play a big role in determining how much you need to save and invest.

This is the first question you must ask yourself, as it will shape the rest of your FIRE journey.

There are different ways to calculate how much you will need for retirement. You can check out the other articles I’ve written describing the 4% rule and the 25x rule when considering retirement.

2. Take into account your cash flow and how much you owe

Cash Flow is Key

FIRE isn’t just about saving money – it’s also about ensuring your cash flow is positive. That means you need to consider how much you earn, how much you spend, and how much debt you have.

For example, if you’re earning a high salary but have a lot of debt, it will take longer to reach financial independence. The problem with debt is that it can be like a weight around your neck, dragging you down and preventing you from making progress.

Once you have a handle on your cash flow and debt situation, it’s time to start thinking about investing. Investing allows your money to work for you and grow over time.

There are many different options, so it’s important to research and find the right ones.

If you’re young, don’t be afraid to take some calculated risks. My wife and I purchased our first real estate property in our early 20s while still attending college. We learned many valuable lessons and were able to later turn it into an investment property that brought in passive income.

You might want to focus on more stable investments if you’re older. Adjust your investment strategy to your age and willingness to take on risk.

4. Automate your finances

One of the best things you can do to reach FIRE faster is to automate your finances. Set up automatic transfers from your paycheck into your savings and investment accounts.

This will help you make headway on your goals without even thinking about it. Automation is key to achieving financial independence because it takes the emotion out of decision-making.

You also want to ensure that you automatically invest your money in the right places. You can do this by using a service like Betterment or Wealthfront.

5. Live below your means

One of the most important things to remember to make the path to FIRE faster is that you must live way below your means. This doesn’t mean that you have to live like a monk – but it does mean that you need to be mindful of your spending.

Seriously consider your every purchase and ask yourself if it’s something that you need. A lot of people find that they can save a ton of money just by making small changes to their spending habits.

If you don’t need it, don’t buy it. Of course, that’s easier said than done if you have kids or other financial responsibilities, but it’s still something to keep in mind.

How is this different than living below your means?

Well, living below your means is more of a general principle. Keeping your expenses low is specifically about finding ways to reduce the amount of money you spend each month.

There are many ways to do this, but one of the most popular is downsizing your home. Moving into a smaller house or apartment can save you a ton of money monthly on rent or mortgage payments, utilities, and more.

7. Make extra money

Of course, saving money isn’t the only way to reach FIRE faster. You can also make extra money to help you reach your goals faster.

There are many different ways to do this, but one popular option is to start a side hustle. This could be anything from driving for Uber to starting a blog to selling products on Etsy.

The key is finding something you’re passionate about and can do in your spare time. Making a few extra hundred dollars each month can significantly affect how long you reach FIRE.

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

8. Go back to school and further your education

No matter where you are in life, there’s always room for further education. Returning to school or picking up a new skill can help you get a better job and make more money.

This doesn’t mean that you need to get a Ph.D. – but taking some classes or getting a certification in something can really pay off.

The goal is to make yourself more marketable and increase your earnings potential. If you can do that, you’ll be well on your way to reaching FIRE faster.

You need to make yourself irresistible to potential employers. Plus, your current job might pay you more if you have more education.

9. Get rid of your debt

To retire early, you must get rid of your debt. We’re talking every last penny – credit cards, student loans, mortgages, car payments, everything.

The reason for this is twofold. First, debt is a massive weight around your neck. It’s emotionally and psychologically draining.

Second, debt costs you money. The interest payments on your debt could go toward your retirement.

The more money you spend on interest, the longer it will take you to reach FIRE. So, if you’re serious about retiring early, you need to get rid of your debt and begin living a debt-free life.

You can always try out the debt snowball method. We used this debt payoff strategy to repay 56,000 in student loans quickly.

10. Put as much money as you can in your retirement accounts

Of course, you want to do this after paying off your debts!

There are tax benefits to doing this, which we’ll discuss briefly. But the most important thing is that you’re putting your money towards your future.

The more money you can put into your retirement accounts, the better. This will ensure you have enough money to live comfortably when you retire.

The best retirement accounts are 401(k)s and IRAs. If you can, you should max out your contributions to both of these every year.

By maxing out your 401(k), you’re putting $18,000 away each year. And if you have a company match, that’s even more money you’re getting for free.

With an IRA, you can contribute $5,500 each year. And if you’re over 50, you can contribute an extra $1,000.

If you can swing it, maxing out these accounts each year is a great way to reach FIRE faster.

11. Reduce your tax burden as much as possible

You’ll need to hire a good accountant to do this. But there are a lot of different ways to reduce your tax burden.

This could be anything from taking advantage of tax breaks, setting up a home office, and deducting your business expenses.

The goal is to keep as much of your money as possible and to have less of it go towards taxes. The less you’re paying in taxes, the more money you’ll have to save for retirement.

You don’t want to cheat on your taxes, of course. But there are legal ways to reduce your tax burden. And you should take advantage of them if you can.

If you do your taxes, ensure you take advantage of all the deductions and credits you’re entitled to.

12. Consider relocating to a cheaper area

This isn’t for everyone. But if you’re serious about retiring early, you might want to consider relocating to a cheaper area.

Moving to a cheaper area will reduce your cost of living and free up more money that you can put toward retirement. We’re talking about lower mortgage payments, cheaper groceries, and lower utility bills.

If you work remotely, this is an especially good option. You can live anywhere in the world and still work from your laptop. The only downside is that you might have to say goodbye to your current lifestyle and social circle.

13. Take good care of your health

Your health is one of your most important assets. The healthier you are, the less money you’ll have to spend on medical bills.

You’ll earn more money now if you’re healthy and can work longer hours. And you’ll have more money in retirement if you don’t need to spend it on medical bills.

If you can be healthy when you’re young, you’ll be more likely to stay healthy in retirement. So, take good care of your health now, and you’ll reap the rewards later.

You’ll also save money once you retire if you’re in good health. That’s because you won’t need to buy as much insurance.

14. Invest every cent that you don’t spend

Any money left over at the end of each month should be invested. Let’s say that you budget yourself $300 a month for entertainment.

But at the end of the month, you only spent $200 on entertainment. That extra $100 should be invested. You might think the $100 is meaningless, and you can let it sit in your checking account.

But that’s not true. That $100 can grow into a lot of money if you invest it. Toss that $100 in a rising tech stock and let it sit for a few years. You’ll probably get a better return on your investment than letting the money sit in your savings account.

One way you can increase your savings and investments is by mico-investing.

ACORNS is a popular platform that can round up money from purchases and automatically allocate those funds to diversified investments.

If you’re unhappy with how things are going, don’t be afraid to make changes. That’s true in both your personal life and your financial life.

If you don’t like your job, quit and find something else. End it if you’re in a relationship that’s not working out.

If you’re not happy with your current financial situation, make changes. That could mean getting a better-paying job, finding a cheaper place to live, or investing more money.

Whatever it is, don’t be afraid to make changes. Life is too short to be unhappy. And you’re in control of your own happiness.

Although easier said than done, you can start making baby steps today toward meaningful change.

16. Don’t let your emotions get the best of you

Your emotions can lead you astray, especially when it comes to money.

Don’t make financial decisions based on your emotions. That’s a surefire way to lose money.

For example, don’t sell all of your stocks when the market is crashing. And don’t buy stocks just because everyone else is buying them.

Investing is a long-term game. You need to take a long-term view if you want to be successful.

You’ve Got This!

So, by now you should know how to retire early. It’s not easy, but it’s possible. You need to be disciplined with your money and make smart financial decisions. Try focusing on one or a few tips in this article to help you reach FIRE faster.

You begin by assessing your current financial situation and setting some goals. Then you need to create a budget and start investing your money.

You should also make sure that you’re taking good care of your health. That way, you can stay healthy and work harder. The harder you work now, the faster you’ll get to enjoy FIRE.

Please comment below with ways you’ve been able to gain control over your finances and speed up your financial freedom journey!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you’re coming up upon retirement and considering moving to Utah, you may wonder how much money you’ll need to have saved up. This article will look at how much money you need to retire in Utah!

The good news is that Utah is a very affordable state, and your retirement income will go a long way.

This post may contain affiliate links; please see our disclaimer for details.

How much money do you need to retire in Utah?

Utah Map

If you’re moving to Utah to retire, you’ll need to have saved up at least $1,000,000. This number may seem high, but it’s achievable if you start saving early and investing wisely.

Your million dollars are needed to cover your living expenses, which we’ll discuss in the next section.

However, everything you will pay will come from your savings, so it’s essential to have a plan and know exactly how much you need.

Your living expenses in retirement will be similar to what they are now, but there are a few key areas that you should budget for.

First, you’ll need to account for housing costs. In Utah, the median home price is over $400,000, depending on location. If you plan on buying a home, you’ll need a down payment and money for repairs and maintenance.

You can expect to pay about $1,500 monthly for a one-bedroom apartment if you’re renting.

Next, you’ll need to budget for healthcare costs. Healthcare is always a big expense in retirement, but it’s essential to plan for in Utah.

Utah has a large population of retirees and a limited number of healthcare providers. This combination can lead to higher prices and longer wait times for medical care.

You could budget about $5,000 per year for healthcare costs in Utah. This number will cover your basic needs like doctor’s visits and prescription drugs.

Your costs will be higher if you have a chronic illness or require regular specialist care.

Things that you shouldn’t overlook when budgeting for retirement

1. Don’t forget to account for inflation.

As we’ve recently seen, inflation can significantly impact your retirement savings. No one can predict what inflation will do, but you should plan for at least a 7% annual increase in your cost of living.

2. Don’t underestimate your housing costs.

Housing is one of the most significant expenses in retirement, and it’s essential to factor in things like repairs, maintenance, and property taxes.

3. Don’t forget to budget for travel.

One of the best parts about retirement is that you finally have the time to travel. However, travel can be expensive. Make sure to set aside money in your budget for trips that you want to take.

4. Set aside money for things like going out to eat.

Everyone gets tired of their cooking sometimes. So make sure to budget for nights out and other fun activities that you enjoy.

5. Hobbies are a must now that you have free time.

If you sit around at home all day, you’ll get bored quickly. Make sure to set aside money for hobbies and activities that you enjoy.

Some retirees may be fine for spending 40,000 per year during retirement.

That $40,000 may sound like a lot, but it won’t buy as much as you think. In Utah, the median household income is about $74,000. This means that your retirement income will only be about half of what you’re used to.

So, you can live somewhat comfortably for 25 years if you have a million dollars saved up. Somewhat is the keyword here. You’ll need to be careful with your spending and ensure you don’t outlive your savings.

I dived into the topics of how much you need in general for retirement by creating two other articles that I highly recommend you check out.

Ideally, you would have at least two million dollars or more saved to live more comfortably.

If you have a spouse, you’ll probably want to have more saved up. And, if you want to travel or do anything else with your retirement, you’ll need more than $40,000 per year.

How much should you have saved by age 65?

There’s no magic number, but the advice was to have 25 times your annual expenses saved by retirement. So, if you make $50,000 annually, you should have $1,250,000 saved.

If you have less than a million dollars saved, you could retire in Utah but may want to look at lower-priced homes.

If you’re in good health and don’t have a physical labor job, you may be able to put off retirement for a few years. This will give you more time to save and reduce the years you’ll need to support yourself.

Working a few extra years may not sound like fun, but it’s better than struggling to make ends meet in retirement.

Even if you scale back and work part-time, that can make a big difference.

Retiring in Utah – Conclusion

If you want to retire comfortably in Utah, you need to have enough money saved up. But the good news is that you have time to save if you’re young!

If you’re not so young, there are still things that you can do to make retirement more comfortable.

No matter your age, the most important thing is to start saving now.

The sooner you start, the more time you’ll have to let your money grow. The more money you save, the more comfortable your retirement will be. Taking advantage of the power of compound interest is one of the most important things to do now.

Make sure you have a plan and start saving now to enjoy your retirement years. You can always check out more articles on our blog to help increase your income while reducing your expenses!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.