Do you want to retire early? The 4% rule is a common guideline that can help you achieve this goal.

The 4% rule states that you should withdraw no more than 4% of your retirement savings (nest egg) each year to ensure that it lasts throughout your retirement.

This article will explain the 4% rule in more detail and discuss some pros and cons of using this guideline.

This post may contain affiliate links; please see our disclaimer for details.

What Is The 4% Rule?

The 4% rule is a guideline that suggests that you withdraw no more than four percent of your portfolio value each year during retirement. The money you take out can go towards living expenses or other things, such as travel or gifts. The rule is meant to help ensure your retirement funds last without having to go back to work.

Some experts suggest using a slightly lower withdrawal rate, such as three percent or even two and a half percent, especially if you’re retired for 20 years or more.

Regardless of your withdrawal rate, it’s important to remember that the 4% rule is just a guideline.

It’s not set in stone, and there will be years when you may need to adjust your withdrawals up or down based on market conditions and circumstances.

This leads to the importance of having a 2-year emergency fund that can cover all expenses if there is a large drop in the market.

What is the Purpose of the 4% Rule?

Simply put, the purpose of the 4% rule is to help ensure that your money lasts throughout retirement.

This is especially important if you plan to retire for 20 years or longer.

The 4% rule is based on the work of William Bengen, a financial planner who wrote a paper in 1994 about safe withdrawal rates from retirement portfolios.

Bengen looked at historical data to see how different portfolio types and withdrawal rates would have fared over time.

He concluded that a portfolio consisting of 50% stocks and 50% bonds would have had a 95% chance of lasting 30 years if the investor withdrew no more than four percent per year.

How Does The 4% Rule Work?

The rule is simple:

You can only withdraw 4% of your retirement account per year.

If your retirement account is $100,000, you can withdraw $4000 per year.

Now you might be thinking, that’s not a lot of money. And you’re right, it’s not.

But the goal of the 4% rule is to make sure your money lasts throughout retirement, even if you live for 30 years or more.

The rule is based on the idea that your portfolio will grow over time and that the money you don’t withdraw will continue to grow and provide for you in retirement.

There are a few things to remember with the four percent rule.

First, it’s based on historical data and may not hold in the future.

Second, it’s a guideline, not a guarantee – you may need to save more or less depending on your individual circumstances.

For example, if you’d like a more comfortable retirement, you can set a goal of $1,000,000 in your retirement account. With the 4% rule, you could withdraw $40,000 per year!

Finally, it assumes that you will withdraw 4% of your savings each year in retirement, which may not be the case.

Despite these caveats, the 4% rule is a helpful way to estimate how much you need to save for retirement.

By following this rule, you can ensure that you are on track to reach your retirement savings goal.

Using The 4% Rule With An Investment Portfolio

To successfully use the 4% rule, it would need to be in an investment portfolio.

This is because the rule is based on the idea that your portfolio will grow over time, and you can withdraw four percent of the value each year without depleting your savings.

For example, if you’re 30 years away from retirement, the fund may be 90% stocks and just 10% bonds. But if you’re only five years away from retirement, it might be 50% stocks and 50% bonds.

This gradual shift helps to protect your savings while still allowing you to grow your money over time.

The most effective fund for the 4% rule is the S&P 500 Index Fund. On average, the S&P 500 grows at 11.5% per year.

Here is an example of calculating how much you’d need to retire comfortably using the 4% rule with the S&P 500.

The first step would be to decide how much income you’d need to live a financially free life.

The average cost of living for a U.S. citizen is approximately $1100 per month but let’s go with $2000 to be conservative and plan for a great retirement!

To receive a retirement income of $2000 per month ($24,000 per year), you’d need $600,000 invested into your S&P 500 account.

Now let’s see how long it would take to reach our goal of $600,000 using the historical growth rate of the S&P 500 at 11.5% annually.

$600,000 might seem like a lot, but with the power of compound interest and consistent monthly contributions, you can get there with just $121,000 as a total investment.

If you start with $1000 and invest $400 per month into an S&P 500 index fund, it would take 25 years to reach the goal of $600,000. But if you started investing at 25 years old, you could retire with an income of $24,000 at 55 years old!

If 25 years is too long, you can get there in only 15 years with monthly contributions of $1400. As you can see, there are many different variables that you can adjust to make the four percent rule work for you.

The Bottom Line: By calculating your desired income, you can find a retirement number that is comfortable for you.

The important thing to remember with the four percent rule is to start saving early and invest often!

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

What Are The Pros And Cons Of The Four Percent Rule?

There are pros and cons to using the four percent rule as a retirement guideline.

Some of the pros include:

It’s simple to understand and follow.

You can adjust your withdrawals up or down as needed based on market conditions and your circumstances.

It’s a helpful way to estimate how much you need to save for retirement.

It uses the stock market’s ability to grow to your advantage.

Some of the cons include:

It’s based on historical data and may not hold true in the future.

It’s a guideline, not a guarantee – you may need to save more or less depending on your circumstances.

It assumes that you will withdraw four percent of your savings each year in retirement, which may not be the case.

The large number needed can seem overwhelming.

Common Mistakes With The 4% Rule

Regarding retirement planning, the “four percent rule” is a guideline that’s often cited.

The rule of thumb goes like this: If you withdraw four percent of your nest egg each year during retirement, you’re unlikely to run out of money.

But as with any rule of thumb, there are exceptions – and the four percent rule is no exception.

People make several common mistakes when using the four percent rule. Here are eight of the most common:

Mistake #1 – Not Adjusting for Inflation: One mistake people often make with the four percent rule is not adjusting for inflation.

When you retire, your expenses will likely go up – not down. That’s why it’s important to factor in inflation when withdrawing money from your nest egg.

Mistake #2 – Not Taking Into Account Your Longevity: Another mistake people make is not considering their longevity.

Just because the average life expectancy is around 78 years doesn’t mean that’s how long you will live.

If you want to be safe, plan for a longer retirement.

Mistake #3 – Not Planning for Unexpected Expenses: People do not plan for unexpected expenses.

Retirement is often unpredictable, and you may need more money than you think.

Make sure to have a cushion in your nest egg so you can cover any unexpected costs that come up.

Mistake #4 – Failing to take into account your own individual circumstances: The four percent rule is a guideline, not a definite rule.

Your retirement plan should be unique to you and consider your circumstances.

Mistake #5 – Assuming that you will have the same expenses in retirement as you do now: Retirement is often a time when people have time to spend money on things like travel and hobbies that they didn’t have time for while working.

As a result, your expenses in retirement may be different than they are now.

Mistake #6 – Not factoring in Social Security: If you’re eligible for Social Security, be sure to factor this into your retirement plan.

Social Security can provide you with a source of income in retirement, which can help reduce the amount you need to withdraw from your nest egg.

Mistake #7 – Withdrawing in tax-inefficient ways: People do not consider the taxes they’ll owe on their withdrawals.

If you’re not careful, you could owe more in taxes than you need to.

That’s why investing with a tax-efficient account is important from the start.

Mistake #8 – Not having a plan B: Another mistake people make is not having a backup plan. What if the market crashes and your nest egg takes a hit?

What if you live longer than expected and run out of money?

Having a plan B can help you weather any storms that come your way in retirement.

As mentioned previously, we highly recommend having a fully funded emergency fund that can cover all expenses in case of a market crash.

The Bottom Line:

If you avoid these mistakes, you’ll be well on your way to a successful retirement.

Just remember to factor in inflation, plan for long life, and have a cushion for unexpected expenses.

You can make the four percent rule work with those three things in mind.

The Rule of 25 vs. the 4% Rule: What’s the Difference?

The Rule of 25 vs. the 4% Rule

The 4% rule indicates that you can withdraw 4% from your retirement and expect that the returns from your investment will surpass the withdrawal rate.

The problem is that with inflation added to this equation, the purchasing power of your money will decrease over time. If you withdraw 4% and the inflation rate was at 8% last year, you’re withdrawing 12% in purchasing power.

If the growth of your investment were less than 12% last year, then you would have to begin dipping into your principal, which is not ideal. This is where the multiply-by-25 rule comes in.

The rule of 25, on the other hand, is a general guideline that suggests you multiply your total salary by 25 to determine how much money you need to save for retirement.

This rule of thumb assumes that you will want to replace your current income via investments during retirement.

It also factors in an estimated annual return of around 10.5% but is used to calculate the total principal you’d need for retirement. It helps to build a mental framework for those pursuing financial freedom.

The 4% rule calculates how much you can withdraw from your principal after the 25x rule is implemented.

For example, first, you would use the 25 rule to calculate how much you need to have saved. Then, the four percent rule would tell you how much you can withdraw from that savings account each year. The 25x rule is a good starting point, but the 4% helps ensure you don’t outlive your money.

Common Questions About The 4% Rule

Q: How long will it take to retire if I follow the rule?

A: This depends on how much money you have saved and how much you can save each year.

Use the example mentioned above and adjust the variables to your preference.

Q: What happens if my retirement lasts more than 30 years?

A: If you want to retire sooner than 30 years, you will need to invest more each month. This is because compound interest will build more reserves for retirement.

You can also consider withdrawing only 2% rather than 4% to allow your investments to keep growing beyond 30 years.

Q: What if I can’t save enough money to retire?

A: If you cannot save enough money to retire using the four percent rule, there are a few options you can consider.

One option is working part-time in retirement. This can help supplement your income and give you something to do in retirement.

Another option is to downsize your lifestyle. Doing so will reduce your expenses and free up extra cash to help fund your retirement.

Lastly, you can delay retirement. This may not be ideal, but it can give you more time to save money and prepare for retirement.

Q: Is the four percent rule a guaranteed way to retire?

A: No, the four percent rule is not a guaranteed way to retire. It is simply a guideline that many people with success have used.

There are no guarantees in life, so it is important to remember that anything can happen when following this rule.

In Summary

The four percent rule is a simple estimate of your retirement savings needs.

Remember to take into account your circumstances when using this guideline.

With careful planning and consistent investing, you can ensure a comfortable retirement for yourself down the road.

Thanks for reading!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Are you looking for a rule of thumb to help you figure out how much money you need to be saved for retirement? If so, you may have heard of the 25x Rule.

This rule states that you should aim to have 25 times your annual living expenses saved by the time you retire. While there are no guarantees regarding retirement planning, the rule of 25 is a good starting point for most people.

This article will discuss the rule, how it works, and why it can be a helpful guideline for retirement savings. So, if you’re curious about the rule of 25, read on!

This post may contain affiliate links; please see our disclaimer for details.

What Is the 25x Rule for Retirement?

The 25x rule for retirement is a guideline that suggests you should aim to have 25 times your annual cost of living saved. This method is from the financial planning community and is based on the idea that you will need to have enough money saved to withdraw approximately four percent of your nest egg each year.

The rule provides a general guideline for how much you should have saved. It is not meant to be an exact formula but a starting point for your retirement planning.

The number 25 is used because it is believed to be a safe withdrawal rate at 4%. This should leave you with 30 years’ worth of income to cover your costs in retirement.

This percentage is based on historical data and research on retirement planning. The average annual return from the stock market is around 10.5%, but this number can fluctuate.

So, with a 4% withdrawal rate, you would have a greater chance of not running out of money in retirement. That’s even factoring in the possibility of the stock market taking a downturn.

Withdrawing four percent of your nest egg each year should give you enough money to cover your living costs. It also allows your savings to last for at least 25 years in retirement; pretty cool right?

Most people retire at 65, so the 25x Rule is meant to make your money last throughout your retirement.

How Does The Rule of 25 Work?

The way the rule of 25 works is pretty simple. You take the age you plan to retire and multiply it by your current annual salary.

Let’s say you want to retire at 65 and make $50,000 per year. To live comfortably, you will need 25 x $50,000 = $1,250,000 annually.

The rule of 25 is a guideline to help you know how much money you should have saved for retirement by the time you reach a certain age. This would give you 40 years to save for retirement if you started saving at 25.

However, this rule of thumb doesn’t work for everyone. Several factors can affect how much money you will need in retirement. Some examples are lifestyle, health, and whether you plan to retire early.

If you want to retire at 55 instead of 65, you will need to save more money. You would have a shorter time frame to save for retirement. Thus, you would also need to account that you may live longer in retirement than someone who retires at 65.

You may also need to save more money if you have a more lavish lifestyle. A giant nest egg is needed to cover your costs in retirement.

Health is another factor to consider. If you have good health, you may need less money in retirement than someone with health issues. You would have more money to cover other costs with fewer medical bills.

The rule of 25 is a helpful guideline, but it’s essential to remember your circumstances. Having this clear picture of your situation will affect how much money you need to save.

It works (most of the time), but some variables can change the amount of money you need to save.

Why the 25x Rule Works (Most of the Time)

The main reason why the 25x rule works is that it’s based on a very solid foundation: the basic principles of saving and investing.

When you save money, you’re essentially putting your money into a “pot” that you can use later down the road.

The same principle applies to investing. When you invest your money, you’re essentially putting your money into a “pot” that will grow over time.

The goal of saving and investing is to grow your pot of money so you can eventually use it for something important, like retirement. We personally love index funds since they minimize risk and, historically speaking, have performed well with an average increase.

Now, the reason why the 25x rule works most of the time is that it takes into account two very important factors: inflation and investment returns.

Inflation is the natural tendency for prices to go up over time. This is why groceries and gas cost a little bit more each year.

Investment returns are the money that you earn from investing your money.

For example, if you invest $100 in stock and it goes up by $20, your investment return would be 20%. The 25x rule considers both of these factors when calculating how much money you need to save for retirement.

It doesn’t sometimes work because the inflation rate can increase or decrease over time, and the same goes for investment returns.

If inflation increases faster than expected or investment returns are lower than expected, you may need to save more than 25x your annual expenses.

It can be challenging to predict what inflation and investment returns will be like in the future, which is why the 25x rule is just a guideline and not an exact science.

As we mentioned earlier, other factors such as your lifestyle, health, and retirement age can also affect how much money you need to save.

It’s always important to remember that your circumstances will ultimately determine how much money you need to save for retirement. That’s why the 25x rule is just a guideline, not a hard-and-fast rule.

The Rule of 25 vs. the 4% Rule: What’s the Difference?

The 4% rule indicates that you can withdraw 4% from your retirement and expect that the returns from your investment will surpass the withdrawal rate.

The problem is that with inflation added to this equation, the purchasing power of your money will decrease over time. This means that if you withdraw 4% and the inflation rate was at 8% last year, you’re withdrawing 12% in purchasing power.

If the growth of your investment were less than 12% last year, then you would have to begin dipping into your principle, which is not ideal. This is where the multiply-by-25 rule comes in.

The rule of 25, on the other hand, is a general guideline that suggests you multiply your total salary by 25 to determine how much money you need to save for retirement.

This rule of thumb assumes that you will want to replace your current income via investments during retirement.

It also factors in an estimated annual return of around 10.5% but is used for calculating how much total principle you’d need for retirement. It helps to build a mental framework for those pursuing financial freedom.

The 4% rule calculates how much you can withdraw from your principal after the 25x rule is put into place.

For example, first, you would use the 25 rule to calculate how much you need to have saved. Then, the four percent rule would tell you how much you can withdraw from that savings account each year. The 25x rule is a good starting point, but the 4% helps ensure you don’t outlive your money.

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

The rule of 25 can be a helpful way to estimate how much money you need to save for retirement. Remember it is a guideline and to be flexible when creating your own financial plan.

Everyone’s retirement savings needs are different and will depend on factors such as your desired lifestyle in retirement and how long you expect to live.

If you’re unsure how much money you’ll need in retirement, several online calculators can help you estimate your specific retirement savings needs.

When saving for retirement, the earlier you start, the better. So, if you haven’t started saving, now is the time!

The sooner you start saving, the more time your money will have to grow, and the less you’ll have to save each month.

If you’re already saving for retirement, stay on track to reach your goals by regularly reviewing your savings plan. This will help you ensure you’re still on track and make any necessary adjustments to ensure you have enough money saved when it’s time to retire.\

As always, thank you so much for reading. We’d love to hear your thoughts in the comments section below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Do you ever wonder how long it would take for your invested money to double?

If so, you are not alone.

There is a whole field of study devoted to answering this question, called financial mathematics.

And one of the most popular methods for estimating doubling time is the Rule of 72.

In this blog post, we will discuss the rule of 72, how to use it, and how accurate it is. We will also show you how to apply this rule to your investment planning so that you can make smart decisions about your money!

What Is the Rule of 72?

The rule is a simple formula that can help you estimate how long it will take for an investment to double in value. The rule is based on the idea that investments grow at a compound interest rate. It shows how many years it will take for an investment to double if it grows at a given compound interest rate.

Think of it as a financial tool to help you understand the power of compounding!

The rule of 72 was developed by a 19th-century Italian mathematician named Leonardo Pisano, also known as Fibonacci.

It can be used for any investment, including stocks, bonds, and savings accounts.

You can use this rule to estimate the doubling time if you know the compound interest rate.

The Formula for the Rule of 72

The rule of 72 formula is as follows:

72 / Compound Annual Growth Rate = the number of years until your money doubles.

For example, if you are earning a 12% compound annual return on your investment, it would take approximately 72/12 = 6 years for your money to double.

A great way to use the formula is to estimate how long it will take for an investment to double.

The rule cannot be used to estimate other financial goals, such as how much money you will have after a certain number of years.

It is also important to know that the rule of 72 only applies to investments that compound interest regularly.

The rule of 72 is not an exact science. It’s a general guideline that can help you estimate how long it will take for your money to grow.

The math is accurate, but often investments won’t have a fixed interest rate.

In addition, the rule of 72 doesn’t take into account any fees or taxes that may be associated with your investment.

So, the rule of 72 can give you a general idea of how long it will take for your money to grow.

Talk to a financial advisor to get a more specific estimate when it comes to your own investments.

In general, the rule of 72 is accurate, but you must consider other factors that may affect your situation.

When using the rule of 72 for your investment planning, it’s important to be mindful of these variables.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

How to Use the Rule of 72 for Your Investment Planning

Now that you know the rule of 72 and how it works, you can start using it to help make investment decisions.

For example, let’s say you are considering investing in a stock with a history of growing at a rate of 20% per year.

Using the rule of 72, we can estimate that it would take approximately 72/20 = roughly 3.6 years for your investment to double in value.

This can be a beneficial way to compare different investments and decide which one is right for you.

You can also use the rule of 72 to see how much your investment would compound and double over and over again.

Imagine you had a $1000 investment that doubled every four years. That would be an 18% interest rate (72/16 = 4).

After only 12 years, you would have $8000.

Now, let’s explore the wonders of compound interest and stretch the timeline to 24 years.

After 24 years, assuming a consistent 18% interest rate minus fees and other expenses, you would have $64,000.

As you can see, with just $1000 and a little time, the rule of 72 can have your money working hard for you.

You would have made $63,000 in profit for no extra work. Consistent contributions and a larger initial investment can increase this.

Let’s say you have just $5000 instead of $1000; here is what the rule of 72 shows us:

After only 12 years, you would have $40,000. In 24 years, your investment of $5000 would grow to $320,000.

With the rule of 72, you can get a quick estimate of how your investment will grow over time. This can be helpful when you’re trying to decide how to invest your money.

The rule of 72 can Estimate How to Pay Off Debt

For example, let’s say you have a credit card with a balance of $1000 and an interest rate of 18%.

If you missed your four-year payments your debt would double to $2000 (72/18 = 4). After another four years, you would owe an additional $2000 with a total of $4000 in debt.

The rule of 42 can be used to see how quickly debt can compound out of control.

It’s a clear mathematical model that depicts the potential scenario if you don’t take action to get your debt under control.

This rule can help you plan and budget for your debt repayment. It also shows how compounding can also work against you if you’re not careful.

The rule of 72 can be a helpful tool when you’re trying to make financial decisions.

It’s important to remember that the rule is just an estimate and other factors can affect your specific situation.

Always speak to a financial advisor to get the most accurate information for your circumstances when in doubt.

In Summary

In conclusion, the rule of 72 is a helpful tool that can estimate how long your money will take to grow.

However, the rule of 42 only works if you have a fixed interest rate and doesn’t consider any fees or taxes.

The rule can be used to predict both investment growth and debt repayment.

When using the rule of 72, it’s important to remember that it’s just an estimate and other factors can affect your specific situation.

Always speak to a financial advisor to get the most accurate information for your circumstances when in doubt.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

There are also many paths to FIRE, and that’s a good thing! By reading this article, you too may find a type of FIRE strategy suitable for your life and circumstances.

So, what are the different types of FIRE? Let’s take a closer look.

This post may contain affiliate links; please see our disclaimer for details.

Traditional FIRE / Regular FIRE

The traditional FIRE movement is about saving as much money as possible and investing it in a diversified portfolio of stocks and bonds. The goal is to reach a point where your investment or nest egg returns are enough to cover your living expenses, so you can “retire” from paid work (although you may still choose to work part-time or volunteer).

This approach is often called the “4% rule” because it’s based on the idea that you can safely withdraw 4% of your portfolio each year, adjusted for inflation.

So, if you have a $1 million portfolio, you could theoretically withdraw $40,000 per year ($1 million x 0.04) and never run out of money.

Of course, there’s no guarantee that the markets will always cooperate, and you may have to adjust your spending if there’s a major market downturn. But over the long run, this approach is quite successful.

The best thing about traditional FIRE is that it’s relatively simple to understand and implement. And, if you start early enough, you can reach this type of FIRE with a fairly modest savings rate.

Lean FIRE is similar to traditional FIRE but with a twist. The goal is still to save as much money as possible and invest it in a diversified portfolio. But instead of aiming for the same amount of expenses, the goal is to retire with a lower lifestyle than you have today.

This could mean retiring to a smaller house, driving an older car, or giving up some of your hobbies and travel. The idea is to reduce your costs to reach FIRE with a smaller nest egg.

Lean FIRE is an excellent option for people willing to make some lifestyle changes to retire early. And it can also be a good choice for people who are risk-averse and don’t want to rely entirely on investment returns to fund their retirement.

Fat FIRE

Fat FIRE is the opposite of Lean FIRE. Instead of retiring on a leaner lifestyle, the goal is to retire with the same (or even a better) lifestyle as you have today. To do this, you’ll need to save a lot of money and invest it in a way that generates high returns. This could mean investing in growth stocks, real estate, or other assets that can generate a high return on investment.

Fat FIRE is a good option for people willing to take on more risk to retire with a better lifestyle. It’s also a good choice for people who want the flexibility to retire early and then go back to work if they want to.

Let’s be honest the average person isn’t going to be able to save enough to retire on a fat FIRE lifestyle. But, if you have a high income and are willing to take a few gambles, it’s possible.

Obese FIRE

Obese FIRE is similar to Fat FIRE, but with one key difference. Instead of retiring with the same lifestyle as today, the goal is to retire with an even better lifestyle.

Some of you might be thinking, “Isn’t that just called rich?” And, well, yes. But the term “Obese FIRE” is usually used to describe people who are retiring with a lifestyle that is far above their current lifestyle.

This could mean retiring to a private island, buying a yacht, or just living in a mansion. But, basically, it’s any lifestyle that most people would consider to be unobtainable.

Obese FIRE is only an option for a very small number of people. But if you have the income and the investment returns to make it happen, more power to you!

Everyone dreams of retiring early and living a life of luxury. It may be your goal; however, it’s essential to know that if it isn’t your reality, that’s okay too!

It’s perfectly fine to live your life in the clouds as long as your feet are firmly placed in reality. So, if you’re planning to achieve obese FIRE, make sure you have a solid plan in place and that you’re prepared for the possibility that it may not work out.

Coast FIRE

Coast FIRE is a strategy for financial independence that involves saving as much money as possible over a short amount of years, then living off the interest once you reach your goal. With Coast FIRE, you save until you reach a predetermined amount by a specific age, at which point you stop saving and let compound interest “coast” you to your desired retirement nest pile.

You could quit your preparatory work and instead take on a part-time job or establish passive income streams to live off of after reaching your financial independence goal, perhaps 80% there. This would allow you to meet life’s essential expenses.

Coast FIRE is a great way to get off to a fast start with active saving and investing, and it can help you achieve financial independence sooner than you might think.

Flamingo FIRE is a new concept that is quickly gaining popularity. The name comes from the Money Flamingo blog, which discusses various ways to achieve financial independence.

Flamingo FIRE refers to the three stages of retirement: semi-retirement, early retirement, and standard retirement. In the first stage, you work full-time to develop a nest egg by saving and investing.

You enter semi-retirement when you reach half of your FIRE number. During those ten years, you don’t need to invest. You can retire if it doubles in 10 years. After that, you can work part-time or a less-paying job that makes you happy till then. Twenty-five times your estimated living expenditures is full FIRE, stage 3. This final stage is when you are truly retired and no longer working.

The Flamingo FIRE concept is an innovative way to think about retirement. It could be an excellent option for those looking for an alternative to the traditional retirement plan.

Barista FIRE

Barista FIRE is where you’re working part-time to pay for healthcare and whatever costs you encounter. For many people, healthcare is their largest expense in retirement.

Paying for healthcare is one of the biggest financial challenges that Americans face. In fact, healthcare costs are one of the main reasons why people say they can’t afford to retire.

One way to pay for healthcare in retirement is to work part-time. This is what’s known as Barista FIRE.

With Barista FIRE, you’re working part-time to cover your healthcare costs. Once your healthcare costs are covered, you can use the money you’re saving to retire early.

This strategy is becoming more popular as healthcare costs continue to rise. It’s a great way to ensure you have the coverage you need while also giving you the freedom to retire early.

Slow FIRE

Slow FIRE is where you’re working towards financial independence, but you’re not in a hurry to retire. The goal is to reach financial independence, but you’re not in a hurry to quit your job.

It’s a good option for people who want to achieve financial independence but don’t want to retire immediately. It’s also a good option for risk-averse people who want to take a slow and steady approach.

The key to making Slow FIRE work is to find a balance between saving for retirement and enjoying your life. You don’t want to sacrifice your lifestyle today in order to retire tomorrow.

But, if you can find a balance, Slow FIRE can be a great way to achieve financial independence and retire on your own terms.

Fart FIRE (or Fast FIRE)

Fart FIRE is where you’re working towards financial independence, but you’re in a hurry to retire. The goal is to reach financial independence as quickly as possible, so you can quit your job and enjoy your retirement.

If you’re the type who loves to throw caution to the wind, Fart FIRE may be the right approach for you. It’s risky, but it can also be very rewarding.

The key to making Fart FIRE work is having a solid plan. You need to know how much you need to save and how you will invest your money.

You also need to be comfortable with the idea of retiring early. If you’re not ready to retire, Fart FIRE may not be the right approach.

It’s important to remember that when you’re trying to speed up the FIRE process, it’s possible to make mistakes. If you’re not careful, you could end up losing everything you’ve worked so hard for.

So, if you’re going for Fart FIRE, make sure you know what you’re doing.

Which type of FIRE is right for you?

Well, the first thing to do is accept that FIRE is a spectrum. There’s no right or wrong answer. You need to find the best approach for you and your family.

If you’re not sure which approach is right for you, ask yourself the following questions:

What are your goals?

How much risk are you willing to take?

How much time do you have to save?

What’s your lifestyle like?

Do you want to retire early or on your own terms?

Once you answer these questions, you should have a good idea of which type of FIRE is right for you.

If you want to retire early, you’ll need to save more money and take on more risks. If you’re not willing to take on as much risk, you’ll need to save more money and plan for a longer retirement.

It’s important to remember that there’s no one-size-fits-all approach to FIRE. You need to find the approach that works best for you and your family.

Conclusion

Almost all of you reading this will want to go the route of traditional FIRE. It makes sense because it’s the most logical and gives you the most control. You can always adjust your lifestyle later on down the road if you want to, but it’s much harder to do the reverse.

Remember, you don’t have to choose just one type of FIRE. You can use a combination of different types of FIRE to achieve your financial goals.

For example, you could use a mix of traditional and barista FIRE to achieve your financial goals. It all depends on your health, age, and desired lifestyle. Whatever type of FIRE you choose, the important thing is to start working towards your financial goals today. The sooner you start, the sooner you’ll be able to retire on your own terms.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

As with this image, you will need to tear back certain parts of your life or make changes to find Financial Freedom.

What does financial freedom mean to you? Is it being able to afford whatever you want without having to worry about money? Or is it something else entirely?

In reality, financial freedom is different for everyone. For some, it might mean living a comfortable life without any debt. For others, it might mean being able to retire early and travel the world.

The important thing is that financial freedom means something different to each individual and everyone can achieve it.

So, how do you go about achieving financial freedom? Read on to find out!

There are many different paths to financial freedom. Some people achieve it through hard work and disciplined saving, while others come into money through investing or inheritances. No matter how you reach financial freedom, the important thing is that you have a plan and you stick to it.

Can you achieve financial freedom?

The short answer is yes! Financial freedom is possible for almost everyone, no matter your current situation.

So whether you’re struggling to make ends meet or already comfortable, you can always make changes to improve your financial situation. It might not be easy, but it is possible.

The key to achieving financial freedom is to have a plan and to be disciplined. You need to know your goals and what you’re willing to sacrifice to reach them.

For some people, that might mean cutting back on unnecessary expenses and saving as much money as possible. For others, it might mean taking on additional work or investing in high-yield investments.

For us, the Biesingers, Financial Freedom is living on our terms. Having enough money in savings and investments that we can pivot or change what we do for work or stop working entirely. We believe that flexibility allows us more opportunities to feel peace and happiness.

Let’s turn our attention to how you can obtain financial independence:

Understand your current financial situation

When it comes to financial freedom, the first step is always the hardest. But the journey becomes much easier once you take that first step.

The first step is to take stock of your financial situation. This means listing all of your debts and savings.

Once you have a clear picture of what you owe and have saved up, you can develop a plan to pay off your debts and grow your savings.

One strategy for reducing debt is first to pay the debt with the highest interest rate or try the Debt Snowball Method. Another method for growing your savings is setting up automatic transfers from your checking account to your monthly savings account.

Have clear goals that you can achieve

The second step to achieving financial freedom is to set clear goals. This means knowing what you want to achieve and when you want to achieve it.

For example, do you want to be debt-free in five years? Do you want to retire at age 60?

Perhaps what you what to achieve is financial independence and retire early. Whatever your goals may be, make sure that they are realistic and that you have a plan for achieving them.

To help you understand how much you may need for retirement, you can check out our other blog posts about the 4% rule or the 25x rule.

Be disciplined with your spending

The third step to achieving financial freedom is to be disciplined with your spending. This means knowing what you can and cannot afford and sticking to a budget.

It can be challenging to stick to a budget, but it is possible.

Many helpful resources are available, such as online budget calculators and financial planning apps.

You can’t just be disciplined regarding spending; you need to track every cent you spend. This means knowing where your money is going and ensuring you are not spending more than you can afford.

You can’t get a good picture of your financial situation if you don’t know where your money is going.

Spend far less money than you earn

The goal is to spend far less than you earn to save as much money as possible. This can be difficult, but it is possible.

There are many ways to save money, such as couponing, setting a budget, and cooking at home.

You also need to ensure you are not spending money on unnecessary things. For example, don’t buy anything on credit that you don’t have to.

The interest on credit card debt can quickly add up and make it difficult to get out of debt.

Have an emergency fund

Life can always throw you a curveball, no matter how well you plan. That’s why it’s crucial to have an emergency fund to cover unexpected expenses. This fund should be used for medical bills, car repairs, or job loss.

Your emergency fund is there to protect you from financial ruin, so don’t dip into it unless it is necessary.

I created another article sharing on everything you need to know about Emergency Funds.

Invest in yourself to become financially independent

It can’t be stressed enough that you must invest in yourself if you want to become financially independent. You should consider investing in college or learning a trade to earn more money.

You’ll never succeed in becoming financially independent or retiring early if you don’t have a skill that enables you to earn more money than the average person.

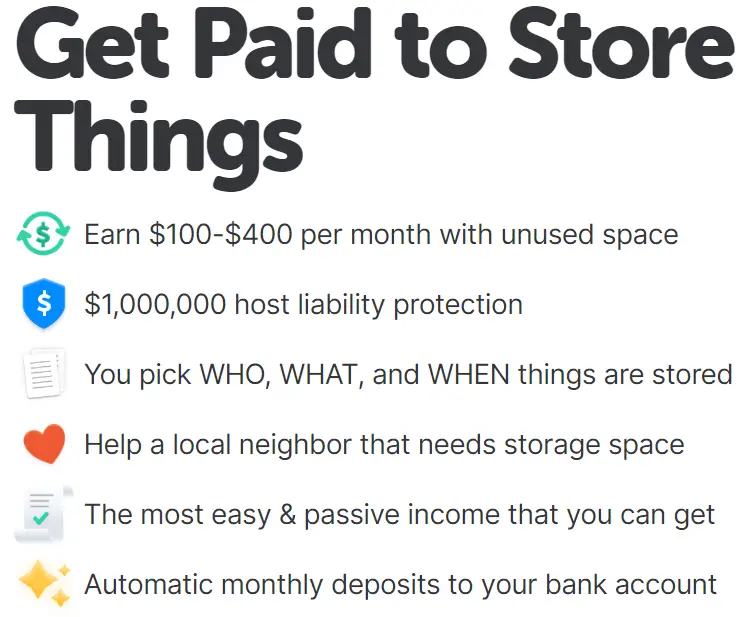

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

Start your own business

One of the best ways to achieve financial freedom is to start your own business. This can be a difficult and risky endeavor, but it can also be very rewarding.

When you own your own business, you control your financial destiny. This means you can earn a lot of money if your business succeeds.

Of course, starting your own business could be something you do on the side. It takes a lot of hard work, dedication, and some risk-taking. But if you are up for the challenge, it can be a great way to achieve financial freedom.

One of the most crucial steps: Paying off debt

Carrying around debt is like having a weight tied around your neck. It can be incredibly stressful and difficult to achieve your financial goals.

That’s why paying off your debt is one of the most important steps to becoming financially free.

There are a few different ways to pay off debt, such as using a debt consolidation loan or making extra payments on your debts.

Whichever method you choose, ensure you are dedicated to getting out of debt as quickly as possible.

Every person reading this can become financially independent

It’s true; every single person reading this can become financially independent. Of course, it will take work, dedication, and discipline, but it isn’t as complicated as you think.

If you are willing to put in the effort, you can achieve financial freedom. It is not an impossible dream; it is within your reach.

The difference between those who achieve financial independence and those who don’t is simply a matter of choice. You’ve got this; we’re rooting for you!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.