This post may contain affiliate links; please see our disclaimer for details.

You have finally saved up enough for a down payment and planning to give an offer on the house of your dreams. The thought of a bidding war may have already crossed your mind.

You’ve looked at a lot of houses and finally found the house that best suits you and your family.

Now you’re ready to put down your offer hoping it gets accepted sooner than later.

We wish getting an offer accepted was that easy and smooth. In recent years the housing market has become the seller’s market.

Especially after the COVID-19 Pandemic outbreak, things have become much crazier with bidding wars. In another article I’ve outlined some of the positive and negative takeaways from Covid-19 that you can check out today.

YouTube Video On How to Win a Home Bidding War

What is the Seller’s Market?

Compared to the buyer’s market, the seller’s market is when there are more buyers than houses available for sale.

Utah has been a seller’s market for a long time now. I’m sure this is the case in other states and regions.

Even though we were outbid during the bidding war, we didn’t give up. It was difficult at first for sure but we quickly adjusted ourselves.

We became more ready for the next property we found, a cozy three-bedroom/two bath condo built in 2002.

Fortunately, our offer was accepted!

So, what can you do to get the perfect real estate property you have been looking for?

In this article, I share Six tips we learned from being outbid.

Utilizing these tips may push your offer to the forefront and give you a better chance of having your offer accepted!

Tip #1: Check regularly for new houses on the market.

Searching for new homes on the market

Remember, it’s important to always aware and check for new houses to come out on the market.

If you find one you like, you should make an appointment to inspect the house immediately. Zillow has been a good platform to see new homes on the market. Being in Utah ourselves, we have mostly used utahrealeastate.com.

Here’s a story to illustrate why you should check for new homes…

One time we found a property (condo) we really like and were ready to check it out. We booked an appointment with the seller’s agent and couldn’t wait to see the condo!

BUT! Just like that the seller’s agent canceled our appointment and told us the seller had already accepted an offer – they had already gone under contract! So that was it, no more showings. 🙁

Unfortunately, we didn’t have a chance to give an offer but we learned some important lessons.

Having a good buyer agent to help you is very important. I still remember my wife found our second real estate property right after it came out on the market, even before our real estate agent saw it. The condo was empty inside with the homeowner completely moved out so potential buyers could go in and check at any time.

The time was around 8:00 pm at night when my wife saw the listing and our agent was still very willing to take us to check it out.

We were the first ones this time to check out the condo and also the first ones to give an offer. The next day our offer got accepted and we were under contract, hurray!!

Let’s discuss more helps tips below –

Tip #2: Ask how many people have checked the property and if there have been any offers.

Sellers and their listing agents are generally not allowed to tell about other people’s offers, especially in detail. But the seller’s agent generally wants to spread the word that a house is in high demand in order to get the best offer in the bidding war.

It is totally ok to let your real estate agent ask how many people have checked the property already and how many are going to check in the near future.

You can also have them ask how many people have shown interest in buying and if they have received any offers yet.

Asking those questions can let you know the demand (how hot) and make a better decision when you make an offer.

This is exactly what we did. You need to have an experienced buyer agent and keep in close touch with the seller’s listing agent.

Tip #3: Give your best and final offer ASAP.

Giving your best and final offer means you can leave without any regrets if the offer falls through, but don’t offer something that you cannot afford! If the final price of the home is higher than you can afford, it is not the perfect place after all.

Speaking with a lender will help you know exactly how much you can afford, but you’ll want to have extra cash flow at the end of each month for investments and savings.

“Just because you can make the monthly payment doesn’t mean you can afford it.”

Dave ramsey

If you have a real estate agent, he or she should have all resources to help you check on the most recent final selling prices and listing prices of homes in the same community.

Pay extra close attention to the highest-selling ones.

But why?…

You’ll be able to compare the real estate property you like to other homes that have been sold and are in a similar condition.

The highest sold price we saw was for a condo that was in better condition than ours but in the same general location. It was a top-floor unit and had a vaulted ceiling but our condo was on the middle floor. The top floor usually holds more value than the middle floor or bottom floor.

We REALLY liked the middle-floor condo we found and did not want to get outbid again.

After calculating our budget, we decided to add $1,000 more than the highest-sold condo we found. We did this because we really liked the property and the most recently sold condo in the area was sold at a higher price and was in better condition.

We gave our best and final price, and our offer got accepted!

Oh, and don’t forget to give your loan pre-approval letter with your offer together. Your lender can help get you a pre-approval letter showing you can afford the loan amount.

Tip #4: Don’t ask too many questions before the offer is accepted.

There are a lot of questions that you might have when buying a house that you’ll want to ask the seller. You’ll want to know the condition of the house if there is anything that needs to be repaired, and so on.

I totally understand that and you for sure have the right to ask and know.

We’ve found it is really best to wait until your offer is accepted before you start asking too many questions.

Don’t let the seller and their listing agents think that you are just asking questions and are very picky. This may make them more unwilling to accept your offer because they will think you’ll be difficult to deal with and don’t like the property as-is.

We always start asking detailed questions once an offer is accepted. Especially since you will typically have a professional inspector to help you inspect the house condition later on.

Tip #5: Put down a backup offer.

If the seller doesn’t choose your offer, ask if you can put down a backup offer.

You never know, some contracts don’t always go through! A lot of homes fail to sell at the end because of buyers’ financial situations where they did not obtain the house loan successfully.

Put down your backup offer ASAP and try to be first in line just in case the deal falls through.

This is what happened when my parents sold their house. The family who was going to purchase their property failed to get the house loan due to some financial problems.

Then my parents quickly decided to accept a back offer which worked out great.

Tip #6: Have faith in more dream homes to come!

Don’t give up if you’ve been outbid!

As mentioned in the beginning, our search to find our second real estate property took longer than we expected and we actually got outbid once.

Being outbid was a disheartening experience no doubt.

We quickly adjusted and learned our lesson from our outbid experiences. There will always have good new properties coming out on the market!

We eventually found a cozy three-bedroom/2-bath condo built-in in 2002. The previous owner had new painting and flooring done which made the property attractive to a young couple like us.

The location was also very close to our college, our first real estate property, and my company back then. On top of that, the condo was also only 3-5 minutes from Walmart, Costco, and other shopping districts! Talk about an awesome location!

Remember in the meantime there is more than one way to invest in Real Estate; that’s why we love Fundrise!

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

Here is a summary of the 6 tips to help you during a bidding war.

Tip #1: Frequently check for new houses on the market.

Tip #2: Ask how many people have checked the property and if there have been any offers.

Tip #3: Give your best and final offer ASAP.

Tip #4: Don’t ask too many questions before the offer is accepted.

Tip #5: Put down a backup offer.

Tip #6: Have faith in more dream homes to come!

In recent years it has been a seller’s market, especially after the COVID-19 Pandemic outbreak where the bidding war has become much more terrifying.

Many properties we knew of received over ten offers in just one day after they went on the market!

One of our friends got outbid six times until his offer was finally accepted.

We hope these experiences and tips can help you win in those crazy bidding wars!

Wish you all the best in finding your dream home that fits your and your family’s needs. 🙂

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

We were college students and did not possess the skills or knowledge of how to be professional landlords.

Now we are more seasoned but looking back at our experiences we wish we would have avoided some mistakes!

In this article I will go over 7 mistakes you will want to avoid as a new landlord.

If you prefer to watch instead of reading this article, please see my YouTube video below.

7 Landlord Mistakes to Avoid YouTube Video

1. NOT doing credit and background checks

Although you may be anxious to rent your house, it is not worth rushing the screening process to find your first tenants. Failing to check each renter’s background and credit history might result in a nightmare tenant.

The correct thing to do is conduct a professional tenant screening process.

We did not conduct any credit checks, payment history, or background checks when finding our very first tenants for our first rental property.

We completely relied on using ‘face screening’ when finding renters for two reasons –

First, as we mentioned at the beginning we were only 22 and 24-year-old college students and this was our first experience renting out a property.

We had no experience or knowledge of the screening process and relied on our gut feeling only.

Second, we were in the process of buying our second condo property and were in a little rush to rent out our first property.

We needed to provide leasing documents, rental deposits, and proof of first-month rental income from our tenants to our lender in order to get a house loan.

We were fortunate enough to find good tenants our first time, but we still consider not going through a formal screening process a huge mistake.

You never really know a person during a short meet-up and without any tenant screening…

Now we have more experience and always conduct tenant screenings. We used Zillow and apartments.com to list our property for rent and send out screening applications.

Signing up was very straightforward and we just used their free services.

2. NOT taking before and after pictures

After you have completely cleaned and have your property ready for renters, make sure to take LOTS of photos before your tenants move in.

Properly document the condition of the property so that you don’t hear “it was like that when I moved in”. All the photos you take become evidence will back you up.

Also, remember to take a lot of photos immediately after your tenants move out and return the keys to you. Check the condition of the apartment and inform them immediately after they move out if there are any issues.

This way they will be less likely to dispute any damages they have caused to your property.

Take out the appropriate repair costs from their deposit if there are damages.

3. NOT treating it as a business

No matter your style of being a landlord, treat your rental property like a professional business.

I still remember when first becoming a landlord. We just wanted to be cool and chill since we are a similar age to our renters.

Since we were young at ages 22 and 24 years old at the time, we even told the people looked at our house that we are chill landlords, etc.

This is not good because it could be taken the wrong way. Your rents could be thinking “oh, they are chill and wouldn’t mind if I’m late on my rent”.

We also feel bad and would have a difficult time saying “no” because we wanted to be nice. Don’t be afraid to say no!

We rented out our first townhouse property to a newlywed couple. They were close to us in age and were very, very picky…

They loved asking us to fix small things and even when many times the contract said it is their responsibility. For example, the main sink in the kitchen got clogged. Instead of having them fix it I went over, added some Drano, and it was fixed in minutes.

Our lease agreement clearly said such problems are the responsibility of the tenant(s), not ours. We always wanted to be nice and so I would go fix it.

When they moved out we noticed scrapes on our wall, floor, and some other small damages. We could have taken some part out of their initial deposit, but instead, we just felt bad and wanted to be nice.

Don’t make our mistake, please!

Instead, we just fixed it all on our own with our money and gave them the full deposit back.

We really did not treat our rental property like a professional business at all. The good thing is that we have improved a lot and will continue to improve moving forward.

4. NOT changing home insurance to landlord insurance

Our rental property at the beginning was our primary residential property. When first purchasing the property we bought home insurance. We did not know that we needed to switch to landlord insurance.

During the process of buying our third single-family house property, we talked with our insurance agent and realized we needed to switch to landlord insurance.

One big advantage of having landlord insurance is having the option to have ‘loss of rent’ coverage if renters are unable to pay rent.

Having this additional coverage was only a little extra than regular landlord insurance but was not expensive at all.

Quick Tip: Generally it will be cheaper when you bundle car insurance and home/landlord insurance together.

5. NOT increasing rent price if you recieve tons of applications

After first posting our townhome for rent we received tons of interested people and applications, I mean TONS.

When this situation occurs, you can definitely increase your rental price a little bit but we had no idea, haha.

We also did not look at various resources to see the current rental price in that community at the time.

Later on, we found out that we could have rented our place out for an additional $100-$200 per month!

Thinking about how much money we lost is a bit disheartening but more important is we are focused on doing better moving forward.

6. NOT raising rent when renewing the lease

Many landlords are happy their rental properties are stably rented out without the thought of increasing rental prices.

Make sure to do your research to ensure that your rent is suitable for your area.

If you have already rented out your property but never increase the rent when the lease is renewed then you are losing out on extra income.

The market price has been increasing but also the cost to make repairs. Periodically having small increases in rent will benefit you in the long run.

You may think renters do not expect their rent to be raided but in fact, many renters expect a small increase every year or so.

It’s common to fear is the tenant will move out and you need to find new renters if there is a price increase. We’ve seen if you have good long-term tenants and you want them to continue to rent out your house then you can rent them out at a little lower than the average market rental price.

We wouldn’t increase the rent too much but instead just a little in order to keep them.

Back with our first tenants we did not do this and kept the price the same, regardless of being under market value. Life is all about learning lessons thought, right? 🙂

7. NOT remodeling before renting out

During the first year we lived in our first 2 bedroom/1.5 bathroom townhouse we did some remodeling and switched old appliances to new inexpensive ones.

As college students, we both did not have much knowledge on how to remodel/rehab properties. I was also not a natural handyman at the time so we did not do a ton of remodeling before renting out our first property.

Thinking back we kind of regret not doing more remodeling since it would have let us rent at a higher price and add more value to the property.

Here is a recap of each landlord mistake to avoid:

Common landlord mistakes to avoid

We understand every city and location is different. I am sharing our own experiences and lessons while investing in real estate in Utah.

Regardless of location, all of us landlords need to educate ourselves and establish contacts with other experienced landlords and related professionals.

After reading this article, you probably know more than the average new landlord. At least you can avoid the mistakes we made as new landlords!

We’d love to hear your experiences or tips, feel free to drop a comment below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Hello F.I.R.E. friends!

Budgeting for expenses, savings, and investments each month is imperative to achieving financial independence.

We hope that you will receive some valuable insights by seeing our monthly spending breakdown.

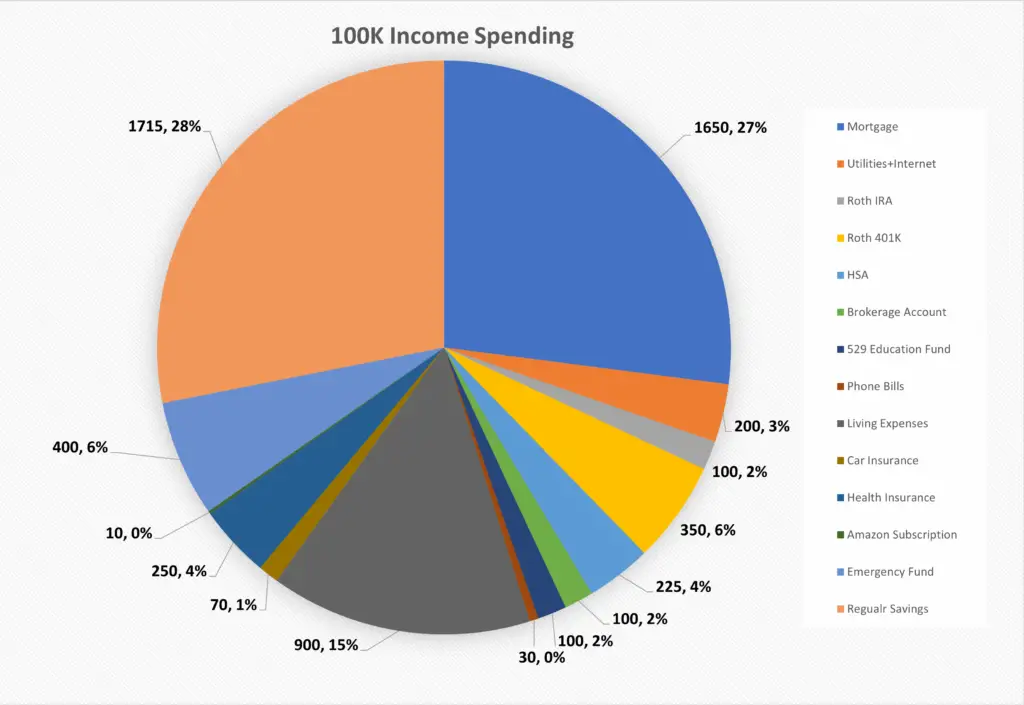

My wife and I’s total pre-tax income is currently $100,000, including both of our salaries (basic salary + bonuses) and our extra rental income.

After taxes, we are at $7,000 a month net income.

Now I’d like to share with you how we spend our $100,000 income as a family of 3 (soon to be 4)!

Our Annual Income Spending

Here is a video of this content if you prefer to watch it instead!

1. Housing Expenses

Our largest expense comes from our monthly mortgage payments. When applying for our house loan, we tried to keep all of our house costs (mortgage+utilities+internet) under 30% of our net income.

The goal is to keep our mortgage payment as low as possible.

We feel this is a healthy percentage and don’t want to max out our house loan debt because we’d rather not be house poor.

We want extra money to invest!

2. Investment Accounts

We are completely debt-free except for the mortgage. This allows us to use more of our income to invest! As you can see from the pie chart, most of our income is going to tax-advantaged accounts/retirement accounts.

My wife and I chose to use Roth IRAs because we don’t want to worry about tax at all when we retire. The thought of being a tax-free millionaire in the future is very exciting.

My wife holds her IRA at Vanguard and mine is with Fidelity. Both investment companies have been great to work with!

After paying off our student loan debt we started to max out our two Roth IRAs each year. The max contribution is $6000 per IRA, so we invest $12,000 total for both of us. We also contribute enough to our companies’ Roth 401Ks to get the company match. Our companies match 4% but we have to contribute 5% to obtain the full 4%.

My wife and I are on separate health insurance plans. I have an HDHP plan and my company matches the money I put into my HSA.

I max out my HSA every year which is $3,200 and invest most of the money into an HSA because it has triple tax benefits and can also be your secondary/regular retirement account when you are 65 years old.

In 2022, you can contribute up to $3,650 for self-only coverage and up to $7,300 for family coverage into an HSA. HSA funds roll over yearly if you don’t spend them and never expire. That’s about a 1.5 percent increase from 2021. Let’s invest more in 2022!

We invest $100 into our regular brokerage account and another $100 for our son’s 529 education fund. Invest in your kid’s future if you can, even just $10 a month!

Small contributions can really add up over time.

Compound interest is the most wonderful thing in the world!

3. Phone Bill

We pay only $15 each per month for our phone bill!

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

4. Living Expenses

Our living expenses include food, outside eating, gas, etc. We have a baby so there are also formula and diaper costs too. We try very hard to minimalize and only spend money on things we need and buy items when on sale.

5. Insurance

We only have one car right now (paid off), and our car insurance is $70 per month. Health insurance and life insurance are through our employers and are $250 a month for our family of 3. Combining all insurances cost totals 4.9% of our monthly net income.

6. Subscriptions

Amazon Prime is currently our only Subscription and it’s been amazing! The most benefits we love are free 2-day shipping and unlimited photo storage space! Amazon Music is also a great plus. It totally worth the money because we have tons of photos!

The monthly cost is $12.99 (plus taxes), and if you buy yearly like us will be even cheaper at $119 (plus taxes). If you are a student, it will be $6.49 per month and $59 yearly.

8. Savings

We transfer $400 a month to our High Yield Saving Account – our Emergency Fund. We will keep transferring money until we save enough for 6 months of expenses.

During times like the 2008 economic recession and COVID-19, tons of people lost their jobs. An emergency fund isn’t just in case of losing a job but also applies to other big and sudden things that happen in life.

For example, the car engine might just break down. Just imagine having enough money in a specific account for all types of emergencies – the peace of mind is real.

We also have a regular savings account. After our expenses, investments, etc., all the rest of the money we have left goes to our standard savings account for other purchases like Christmas gifts, new clothes, travel, even our next house down payment, etc.

Are you looking for a robust app to help you gain awareness of your spending habits and stay on top of budgeting? If so, we highly recommend Rocket Money (formerly Truebill). Their app is extremely easy to use and can help you gain better control over your finances and know your net worth. Feel free to check them out today!

Mortgage

23.6%

$1,650

Utilities+Internet

2.9%

$200

Roth IRA

14.3%:

$1,000

Roth 401K

5%

$350

HSA

3.2%

$225

Brokerage Account

1.4%

$100

529 Education Fund

1.4%

$100

Phone Bills

0.4%

$30

Living Expenses

12.9%

$900

Car Insurance

1.0%

$70

Health Insurance

3.6%

$250

Amazon Subscription

0.14%

$10

High Yield Saving account/Emergency Fund

5.7%

$400

Regular Savings

24.5%

$1,715

Total

100%

$7,000

Our Annual Income Breakdown

Now you know how we spend our $100,000 income as a family of 3.

Comment below or email and tell us how you budget your income! Share with us any other money-saving tips you use!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

The term HSA is short for ‘health saving account‘. An HSA is an amazing tax-advantaged account! Whenever we hear or see the word tax-advantaged, we pay special attention to learning all we can about it.

This post may contain affiliate links, please see our disclaimer for details.

My wife and I have separate health insurance. She and our kids are under her company’s PPO (preferred provider organization) plan.

I have an HDHP which is a high-deductible health plan. With an HDHP, I have the option to open an HSA account.

My company matches part of the money that I put into the HSA!

We had our first baby in Oct 2020 and our second is due at the end of February 2021. I will use part of our HAS fund for eligible expenses from the upcoming hospital bill.

We use the remaining amount to INVEST!

You may use your HSA funds on both your spouse and tax dependents. For example, you can use it for eligible medical expenses for your children (not adult children, haha).

So even if you’re like us and your spouse and kids are not on an HDHP plan, don’t fear! They can still use the funds from your HSA for eligible medical expenses.

I max out my HSA every year!

An HSA has triple tax advantages and can also be considered a retirement account when you are 65.

It is a fantastic FIRE friend to have on our fire journey.

I will first explain an HSA’s Triple tax benefits in this article. Then I will share how to invest in an HSA for retirement!

What exactly is an HSA?

A health savings account is a tax-advantaged savings account. It is available for those who have an HDHP (High Deductible Health Plan).

An HSA allows you to deposit pre-tax funds each year. You can then use those funds to pay for qualified medical expenses.

Each company may have a different HSA contribution limit that must be reached before being able to use the funds to invest.

For my HSA, the requirement is to have a minimum of $1000 saved up before being able to invest in the stock market.

If you have an HDHP in 2022, you can contribute up to $3,650 for self-only coverage and up to $7,300 for family coverage (different HDHP plans).

HSA funds roll over year to year if you don’t spend them.

What are the HSA Triple Tax Benefits?

Contributions Are Tax-Free

Withdrawals for Qualified Medical Expenses are Tax-Free

Investment Growth is Tax-Free

Triple tax benefits can be difficult to come by. That’s why an HSA is so amazing.

Here are more details on each of the three tax benefits.

Contributions are tax-free

Taxes do not need to be paid on the money you deposit into your Health Savings Account!

In general, there are two ways you can put money into an HSA. First, your HSA contributions can come straight out of your paycheck through a pretax payroll deduction.

Second, if you choose to make contributions with after-tax dollars on your own, you can claim them as tax deductions when you do your income taxes return.

There is no “use or lose” rule like an FSA (Flexible Spending Account). The money saved up in an HSA will roll over year after year.

Withdrawals for Qualified Medical Expenses are Tax-Free

Not only can you contribute money tax-free to an HSA, but also money taken out from your HSA follows the same principle!

As long as you use your HSA money to pay for qualified medical expenses, you won’t need to pay any taxes or penalties on the withdrawal.

Investment Growth is Tax-Free

As mentioned previously, once your account hits a required minimum balance, you can start investing the money you have in your HSA.

For my HSA, the requirement is to have a $1000 minimum saved up first.

Choosing to invest in your HSA has the advantages of tax-free growth and makes a nice addition to our retirement portfolio.

Our HSA is a good FIRE friend on our fire journey!

How an HSA Works as a Retirement Account

BEFORE age 65: withdrawals for non-qualified medical expenses will have a penalty and income tax that must be paid. Usually, the penalty is 20%, ouch!

AFTER age 65: withdrawals from your HSA may be used for anything you’d like without paying the 20% penalty fee, but you’ll still have to pay income tax on the withdrawals. It works similarly to a Traditional IRA.

Now you know the HSA’s Triple tax benefits and how it can be used as a tax advantage retirement account! We are grateful we didn’t miss such a good triple tax advantage account.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links, please see our disclaimer for details.

Before jumping into the debt snowball method and how it works, I’d like to share a quick statistic regarding the average amount of debt in the United States.

According to business insider, the average American has $52,940 worth of debt across mortgage loans, home equity lines of credit, auto loans, credit card debt, student loan debt, and other debts like personal loans!

YouTube video sharing how I paid of $56,000 in student loans

If you are one of countless Americans who want to know how to repay debts, you may have heard of a lot of different methods of repaying debts.

One such method is the debt snowball method!

The debt snowball method has helped us stay on track when paying off debt and is the method we used to pay off $56,000 in student loans.

Using the debt snowball made us very excited and stay motivated when paying down our student loans. I remember how my smallest student loan was only $800. We were able to pay it off quickly. It felt GREAT!!

We really could not express our excitement in words when we saw the balance for that small loan become zero!!

That excitement gave us the motivation to keep going. To make all the remaining loan balances become ZERO.

If you are reading our article, you must wonder how to pay off your debt. Let me introduce you to your best new friend: the debt snowball method!

What is the Debt SnowballMethod?

The debt snowball is one method to pay off debts in a specific way. You just need to arrange and pay off your debts from smallest to largest, ignoring the interest rate. Doing so builds momentum or a snowball effect that helps keep you going.

Imagine a snowball rolling down a mountain. At first, it was very small. As it continues to roll, the snow layers increase.

Each time you add a layer, the snowball gets bigger and bigger. This helps the snowball gain a lot of momentum.

By the time the snowball had reached the foot of the mountain, it had grown to the size of a boulder!

How Does the Debt Snowball Work? Step-By-Step

Step 1: List your debt amounts (except mortgages) from smallest to largest, regardless of interest rate.

Step 2: Continue making the minimum payment on all debts except for the smallest debt amount.

Step 3: Pay off as MUCH of your smallest debt as FAST as possible.

Step 4: Repeat steps 1 through 3 until all debts are paid off in full!

Here are more details for each of the steps:

Step 1: List your debts (Except your mortgages), from smallest to largest, regardless of interest rate.

Write down every outstanding debt you have (except for the mortgage). This may include credit cards, student loans, medical bills, car loans, and any other types of debt you have broken out from smallest amount to largest.

Write down the minimum monthly payment, monthly due date, etc., just to keep everything on track.

Step 2: Make a minimum payment for all debts except the smallest debt.

Keep paying the minimum monthly payment for all debts. The payment history will affect your total credit score.

Therefore, the more you pay on time, the fewer the late fees. Doing this will increase your credit score!

Having an excellent credit score is so important. We ended up not getting the best interest rate for our second property due to having a bad credit score which was sad.

The positive thing is that we learned a valuable lesson and became more careful of our credit and monitoring our credit scores.

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

Step 3: Repay as much of your smallest debt as possible.

After making a minimum payment on all debts accounts, put any remaining money into the smallest debt (loan) until the smallest debt is paid off. Then move on to the next smallest debt.

Step 4: Repeat steps until all debts you have paid off all debts in full.

Continue to put all extra cash into the smallest outstanding debt until it is paid off in full.

You can then focus your efforts on paying off the next smallest debt. Do this until all debts are fully paid off!

Why we used the debt snowball

“Focusing on paying down the account with the smallest balance tends to have the most powerful effect on people’s sense of progress – and therefore their motivation to continue paying down their debts.”

In the beginning, like many people out there, I didn’t know that student loans were bad and never thought I could graduate student debt-free.

People I knew would congratulate me on successfully receiving a student loan for any given semester. When we purchased our first townhome, I still recall how I was required to give our lender a future monthly student payback plan (once I graduated).

My income was lower then, so the monthly payment plan was about $30 a month going off an income-driven payment plan. I thought to myself, “oh!? student loans aren’t too bad.

I only need to pay back $30 a month after I graduate!” but when we purchased our second property, I had a better job with a higher income.

At that moment, I was shocked to see how much I needed to pay every month after graduating on an income-driven plan.

The number went up like crazy! That was the first time I realized student loans are not good.

If interested, please contact your student loan provider to see your payment plan when your income increases. Then you will know what I am talking about.

Thank goodness my wife found out about the amazing Dave Ramsey. Even now, we are still very grateful for Dave Ramsey’s teachings on personal finance and getting out of debt, he helped change our lives!

My wifey listened to him tons at first and then would tell me, “Hey baby, let’s save up for your MBA tuition by ourselves and pay down your bachelor’s student loans”!

My wife received a full scholarship, and her parents also helped her with other expenses before we got married. I had accumulated $25,000 in student debt from my bachelor’s degree. My MBA was a remote/online program with six semesters; the total tuition was $31,000.

That means we needed to pay off $56,000 once I graduated!

While saving and paying for my MBA tuition, I still needed to pay off the student loans left from my bachelor’s degree. We used the debt snow method to get it done.

First, we listed all the balances and then paid them off from small to big, ignoring the interest rate. Using this method gave us much motivation and a positive feeling whenever we paid a loan balance off!

Later, the COVID student loan relief plan went into effect, and the interest rate became zero during a specific period. We were able to save a lot on interest from this relief plan.

From the point of view of mathematics and numbers, Snowball’s debt won’t let you save the most because of varying interest rates.

The point is to change behavior and encourage/motivate us to pay our debts faster with more motivation in the long run.

“Winning at money is 80 percent behavior and 20 percent head knowledge. What to do isn’t the problem; doing it is. Most of us know what to do, but we just don’t do it. If I can control the guy in the mirror, I can be skinny and rich.”

Dave Ramsey

Everyone’s financial situation is different. Please consider other debt repayment strategies until you find one that suits you best. For us, the debt snowball worked great!

Remember, many methods and strategies help you pay off your debts. We all are in unique financial situations and may have different types of debt, and we hope you can find a method or a combination of methods that works best for you.

Although we did not need to refinance student loans, it can be an option that can save you potentially thousands of dollars over the life of a loan.

If you need to refinance student loans, we highly recommend using LendKey.

They offer low-rate and low-cost student loan refinancing. Additionally, your credit score will not be impacted when exploring rates.

Has the debt snowball method been effective for you? What are some other strategies you’ve enjoyed to pay off debt?

Please leave a comment below and let us know!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.