This post may contain affiliate links, please see our disclaimer for details.

The kitchen of our third property located in Utah

Initially, we had no plans to buy our third property anytime soon (in Utah). My wife Shan and I were going to wait until after I graduated with my MBA.

One day we were looking around at different home builders, but just for fun.

One of the builder’s sales agents wrote down our contact information. Within one week, he told us new lots were being released soon.

Since the new community of homes being built was close to my parents’ house, only a 3-minute drive away, we decided to go and check it (still, just for fun)!

The agent told us two days later there would be an increase of $5,000 to the base prices of all new homes within the next few days. He explained that any contract signed soon will keep the current price and not be increased.

This news impacted our decision to go under contract! After discussing with my wife, we realized if we kept our original plan (to wait), it would become difficult to afford a nice home with the constantly rising prices!

Turns out we made a good decision since our house increased in value by over $100,000 from the time we went under contract to when we closed!

Construction started on our new home in July of 2020. The building process took about ten months to finish. We officially closed on our house / third property in May of 2021!

Price of Third Property

The total price of our new single-family home in Utah was close to $340,000 (with a few upgrades included). The square footage is 2,300, and the lot size is 0.12 acres.

We put 5% down, which was $20,000. Our interest rate is 3%, with mortgage insurance around $35. In total, our mortgage payment is just $1,600 a month!

Also, reach out to at least three different lenders so you can compare rates and get the best deal at closing.

One of the lenders we spoke with told us they would beat anyone else, even if it meant lowering their commissions.

We went with him because he could give us the best deal for closing costs and interest rates.

Here are the most commonly required documents when applying for a home loan or refinance. Your lender may ask for additional documents on a case-to-case basis.

Common documents when applying for a mortgage or refinance:

2-year tax returns

Pay stubs, W-2s, or other proof of income

Bank statements and other assets

All of your debt monthly payment history

Credit score, credit history

Gift letters (if someone helps you with down payment etc.)

Photo ID, SSN

Rent history if you are renting, mortgage/HOA history if you are a house owner

House insurance company if you have a preference, usually it will cheaper when you bundle with car insurance

If you have tenants, include rent payment history & current lease agreement

Why we decided to buy our third property.

These are the three main reasons we decided to purchase our third property –

1. Higher annual income

2. Low-interest rates

3. Family expanding

1. Higher annual income.

By reading how I graduated debt-free, you will see how I moved up to a new job as a Product Development Specialist after starting the first semester of my MBA program.

Having a higher annual income helped us qualify for a nicer house. It’s important to always make sure you budget and don’t restrict cash flow when purchasing a house.

Just because you can make the monthly payment doesn’t mean you can afford it.

Dave Ramsey

2. Low interest rates.

Covid-19 was just starting when I switched to my new job. Due to bad economics, the government approved near-zero interest rate plans to help the economy. See HERE for more details.

The interest rates became amazing to buy a home but also sped the housing market prices like crazy. We are so grateful to have built a house at the beginning of the market housing market boom.

We started to expand our family. Now we have one baby boy and a baby girl on the way. We needed more space in the house and also need a nice sized backyard for them to play and run around.

We also wanted to move nearby my parents. Living close to them would be convenient when we needed their help taking care of kiddos and family events.

Regardless of if you have a family or not, it’s vital to understand one’s finances and follow a monthly budget.

Are you looking for a robust app to help you gain awareness of your spending habits and stay on top of budgeting? If so, we highly recommend Rocket Money (formerly Truebill). Their app is extremely easy to use and can help you gain better control over your finances and know your net worth. Feel free to check them out today!

Advantages of building a brand new house.

Locked in Price

Extra time to prepare a down payment.

Choose your own design.

Less fixing and maintenance costs.

1. Locked in Price

We could lock in our home’s final price at the beginning (once under contract). Even when it took 10 months to build our house.

No matter how crazy the house price increased, our price was 100% locked in and would not increase. During these 10 months, our house increased by almost $100,000!

By the way, we did see some news that some builders weren’t honest and broke the contract to increase the price. Luckily we did not have any such issues.

2. Extra time to prepare a down payment.

We only needed to pay $3,500 to go under contract. The building process took around 10 months. That means we had an awesome 10 months to prepare everything.

We sold our first property, rented our second property, paid off student debt, and saved up the rest of our down payment by closing!

3. Choose your own design.

The most fun and exciting thing for us was being able to choose your upgrades for both the exterior and interior. At the design center, you can choose the flooring you like, paint colors, and much more.

We didn’t do a lot of upgrades because we didn’t want to max out our loan. We had to work hard to stay calm in the design center because everything was so attractive and made you want to spend more money!

4. Less fixing and maintenance costs.

The second-hand houses we bought before always had small problems (sometimes big problems!) that needed to be fixed.

Compared to the old properties, the new home we purchased would not need repairs for a long time. This is a big relief having everything inside just new and fresh!

Our third property, a single-family home in Utah, during the building phase.

We officially bought our third property this year in May 2020. During the building period, I was taking Maser courses, and we had our first kid.

It was so fun and exciting to see the whole building process of the house. We just went and checked practically every week. 😀

Now we enjoy living there and recently got a Samoyed puppy after moving in. Her name is Tofu. Our baby girl is due at the end of February next year (2022)!

Our lives are becoming better and better! We are excited to share more of our FIRE journey with you in future articles!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links, please see our disclaimer for details.

In this article, I will share how we came to realize student loan debt is the best thing to have. Then I will introduce the 11 money tips that helped accelerate our debt-payoff process and allowed me to become student debt free by graduation! In total we paid off $56,000 in student loans.

The Realization

Back in the day, my wife Shan and I didin’t think student loans were a bad thing. The thought of graduating zero debt in student loans had never crossed my mind.

When purchasing our first townhome, I had to give our lender my student loan payback plan. This is the amount I would owe each month upon graduation.

At that time I had a much lower income. The monthly payment plan was only $30 going off an income-driven payment plan. I thought to myself, wow! Having student loans isn’t too bad because the monthly payments after graduation are so low.

I would only need to pay $30 a month after I graduate! But when we purchased our second property I had a better job with a higher income.

At that point, we needed to provide another income-driven payment plan to our lender. I was shocked to see how much I needed to pay every month. The monthly payment amount shot up like crazy!

I realized student loans were not the best thing to have.

Thankfully we found Dave Ramsey and agree with many of his money tips. Even now, we are still very grateful for Dave Ramsey’s teachings on personal finance and getting out of debt. His teachings helped spark our change toward our finances.

At first, it was Shan who listened to him who would tell me, “let’s save up for your MBA tuition by ourselves and pay down your bachelor’s student loans”!

“The average total student debt continues to teeter around $30,000”

US News

She received a full scholarship, and her parents also helped her with other expenses before we got married.

Me, on the other hand… I had accumulated $25,000 in student debt from my bachelor’s degree.

My MBA program was remote/online with six semesters, and the total tuition for the program was $31,000.

So, we needed to pay off $56,000 once I graduated!

It was time to change and start paying off my student loans EARLY! Let me introduce how I graduated debt-free and after becoming a new father and still being a college student.

My graduation ceremony at Utah Valley University (UVU)

1. Mint Mobile: monthly phone plans at AMAZING prices

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

2. Budgeted life and Raise

We wouldn’t eat out a lot but instead would cook at home. We would frequently make a lot of food, divvy it up into lunch boxes, then put it in the freezer.

Doing this was so convenient, especially when constantly on the go. You can just warm it up in the microwave when needed.

We decided to buy a lot of things second-hand, don’t buy brand new!

There are many free things through the Facebook marketplace, such as our baby’s toys, stroller, etc.!

We are big fans of Raise where you can buy gift cards at a discount for places like Walmart.

3. Rent out our extra room

Before having our first baby, we would always rent out our extra room to friends or family members.

We personally didn’t want to share the place with someone we didn’t know so we typically stuck to people we knew.

Giving them a good deal was important to us, so it turned out to be a nice win-win situation.

4. Sold a lot of stuff (minimalize)

We watched minimalism videos which were very intriguing to us and gave us the motivation to sell items we didn’t need.

To help us know what we don’t need, we would ask ourselves, “does this item really add value to my life?”.

I even sold my PS4 and Nintendo Switch because I was simply too busy with my full-time job and full-time school.

I wanted to spend any extra time doing more meaningful activities (such as learning about investing!).

We love pets! Whenever our friends would ask us to help watch their pets, we were more than willing to do so.

My wife is from China, so she knew a lot of international students who didn’t have family here. They needed people to watch their pets when they traveled or went back to China.

Since we love animals, this was an easy side hustle.

For us, this was not a job at all; we both enjoyed playing with each pet (by the way, we would only watch fully trained pets, so it wouldn’t be hard to take care of them).

We like using the pet sitting site/app called Rover where you can get paid to help watch other people’s pets!

Regardless of what you do, finding a side hustle is a great idea to add some extra cash to help pay off student debt.

6. Donating Plasma

I heard about donating plasma from my brother and started donating it.

You can probably make around $400 a month, sometimes even more, when there is a promotion going on! Depending on the place, each donation will take around one hour total and you can donate up to twice in one week.

It was so easy, I just had to lie down there and could read a book or play on the phone.

I still donate plasma sometimes when they have a good promotion, but now the money I get is my “freedom/fun money” lol.

7. Find a higher-paying job

I always worked full time while going to school full time. During my time at college, I moved up the ranks to a supervisor position when I first got married. Then to an account manager during the last year of my bachelor’s program. I then became a product development specialist after the first semester of my MBA.

Each position change gave me around a $15,000 salary increase. In total, I had around a $30,000 salary increase during school! I would quickly move to another position once I became comfortable with my job responsibilities and look for opportunities to expand my knowledge and skills.

8. Employer tuition reimbursement.

The company I work at as a product development specialist is amazing. They offered me $3000 each year of tuition reimbursement.

For my two years of studying for my MBA, I received a total amount of $6000 for tuition reimbursement.

This is a great benefit that helped us pay off debt faster.

9. Other student financial aid

After getting married, I received some grants! So I didn’t pay any tuition for the remainder of my bachelor’s degree.

We highly recommend looking and applying for scholarships or financial aid rewards.

While we were saving and paying for my MBA tuition, I still needed to pay off the student loans left from my bachelor’s degree. We used the debt snow method to get it.

First, we listed out all the balances and then paid them off from small to big, ignoring the interest rate. Using this method gave us so much motivation and a very positive feeling whenever we paid a loan balance off!

Then what happened later was the COVID student loan relief plan, where the interest rate became zero during a certain time period. We were able to save a lot on interest from that relief plan.

Due to Covid in 2020, the interest rate became so low resulting in a boom in the housing market.

It was a hard decision to sell our first rental property because we want to keep it long-term.

After thinking long and hard, we both feel peaceful about selling it. Around the last year of MBA, we sold our first property. I used part of the profit to pay off the rest of the student loans we owed.

It was an amazing feeling to be able to use cash to pay off the rest of my MBA tuition.

We became 100% debt-free except for the mortgage after that!

12. Bonus Tip: Refinance Student Loans

Although we did not need to refinance student loans, it can be an option that can save you potentially thousands of dollars over the life of a loan.

If you need to refinance student loans, we highly recommend using LendKey.

They offer low-rate and low-cost student loan refinancing. Additionally, your credit score will not be impacted when exploring rates.

Although the journey was not the path of least resistance, it was the biggest relief for us to pay off all student loans. The feeling is amazing and free!

No pain, no gain! We really like what Dave Ramsey has said, “live like no one else, and then live like no one else”! Below is a recap of the 11 steps:

Screenshot of my Navient Loans all paid off with zero balances!

The average monthly student debt payment in the USA is around $400 a month. If you instead invest $400 a month in a reliable fund (like S&P 500) with average an average return of 12%, you will have around $92,000 in 10 years and ONE MILLION in 28 years!

We are so grateful that I could graduate student debt-free with both my bachelor’s and master’s degrees.

I know someone who wanted to buy a house but couldn’t qualify because of their huge student loan debt and needed to pay down the loan balances first.

The housing prices went up a lot when they finally qualified for a house loan. It was so sad! We hope our experiences and tips can help each one of you!

You will not regret starting now. Take the time to create the best method for you to pay off student loans early; you won’t regret it!

What other ways have you used or have thought of paying off student debt early?

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links, please see our disclaimer for details.

Before sharing my story on why and how I became car debt-free, I want to share these interesting numbers with you…

The average monthly car payment in the USA is around $550 for new vehicles, $400 for used vehicles, and $450 for leased vehicles.

If you invest $550 a month in a reliable fund with an average of 12% return, you will have around $126,000 in 10 years, and ONE MILLION in 25 years!

The average value of a new vehicle drops around 20% in the first year of ownership, and will drop up to 60% of its value within the first five years!

YouTube Video Why I Sold My Luxury Car

Throughout my life, I’ve always loved the Land Rover Discovery model. When I was a young college boy I did not understand much about personal finance and debt.

I made the unwise decision to go into debt with a car loan for a second-hand Land Rover (LR3 model). Soon that vehicle became my worst nightmare!

This was the first time I had received a car loan and taken on a large amount of debt.

Previously, I drove around an old Ford SUV my mom had given me, but I sold it to buy my dream Land Rover.

Things seemed amazing at the very beginning after getting the vehicle. I was living the dream, driving around off-road with buddies and living it up… but that didn’t last long.

My vehicle started having many small issues but they were very costly to fix. Being a Land Rover car, repairs were expensive and sometimes needed a specialist.

Another big cost for a young college student was the gas money. The vehicle had terrible gas mileage.

On top of all that, my tire blew out when I went off-roading with some friends. The cost to replace all tires (because I wanted the best ones) cost me almost a thousand dollars.

Yikes!

I had no savings left over each month because of that ‘fun’ car. My wife who was my girlfriend back then helped pay for the new tires.

I am grateful for her help but also feel bad that I was not in a financial position to take care of my expenses. It was time to change.

My Luxury Vehicle – Land Rover Discovery LR3

I woke up and realized it was time to let it go.

Sometimes the process of selling a car takes a long time. I had little patience to wait because I wanted to be car debt-free and not have so many car expenses.

Many people show up to check out the car which gave me hope but then ended up not buying it.

Two options remained; I could either sell for a lower price or wait it out.

In the end, I finally sold it after a couple more months at a decent price. I used the money to pay off my car loan completely.

I then purchased a second-hand Toyota Corolla from my brother-in-law at a really good price.

My brother-in-law has his own car shop and Toyota is his number one favorite brand. He would tell me how Toyota is an amazing brand with amazing reliability.

I could basically drive that new car forever!

Life finally calmed down a bit after I sold my Land Rover. I was very happy with my Toyota Corolla. It had no issues at all!

Even if there were repairs (which there weren’t any), the repairs would have been much cheaper.

The gas mileage was also much better than the gas guzzler I previously had. Best of all, I was car debt-free and felt fantastic.

“Drive like no one else, and then drive like no one else.”

In other words, be willing to sacrifice what you want now for what you want most.

Even now Land Rover is still my dream car but I will not get it until we hit our financial goals (FIRE!!).

We are still young and we should use extra money to invest, invest, and invest.

“Time is your friend, impulse is your enemy. Take advantage of compound interest…”

Warren Buffett

Compound interest is the most wonderful thing in the world. Start investing early and start now, you will see how miraculous it is and how it grows like crazy over time!

My motivation is knowing that one day I will buy a brand new Land Rover with all cash.

I believe it will happen and I will work hard to make that dream come true, including investing to make that happen!

I hope my personal story about car debt can aid you in making better decisions to help you achieve financial freedom sooner.

Others may think you’re crazy for not getting a car loan or driving an older vehicle, but it will be worth it in the end! 🙂

Instead of financing a car, you can save up cash to buy a used reliable car. You can also focus on saving up the cash by doing different side hustles. We personally love Neighbor.

If you have extra unused space, such as an area for a parked car, then you should check out NEIGHBOR. They allow you to make money by renting out space you are not using!

Drop a comment or question below! We’d love to hear about your experiences dealing with car debt and car troubles.

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Hello, and welcome back! In this article, I will share how we purchased our second property by converting our first residential property into a rental, thus becoming first-time landlords!

Preparation and planning were vital when we bought a second property and rented out the first property.

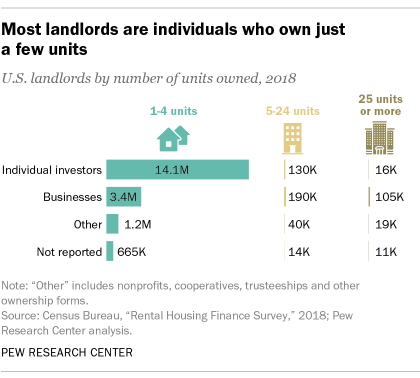

According to Pew Research Center, most landlords located in the US own just a few units (see image below). Starting small and early is the way to do it.

This post may contain affiliate links; please see our disclaimer for details.

After one year as a bilingual supervisor, I felt too comfortable with day-to-day responsibilities.

The work was not as challenging anymore, although I loved what I was doing.

Sometimes it can be very difficult to leave a job, especially when you feel comfortable and have good co-workers.

My wife Shan kept encouraging me to find a higher position or a new job. I am very grateful for her advice and encouragement!

A few months passed, and I received an offer as an account manager at a financial software company.

After accepting the job offer, I decided to switch all my college classes to online classes so my schedule could become much more flexible.

We then started looking for our second property in Utah. We planned to rent out the property we lived in (our first property) and become landlords.

We put down a 5% down payment for the second property because we did not have much in our savings at the time. We also wanted to move into a new place asap since the housing market was pretty hot.

The sooner we could close on the property, the sooner we could start building equity.

This is one of our favorite quotes about real estate –

“Don’t wait to buy real estate, buy real estate and wait. “

T. Harv Eker

Since it was our second property, we could only apply for a conventional loan which requires a minimum of 5% down. We also needed to pay PMI (mortgage insurance) since the down payment did not reach 20% of the loan’s total amount.

The process of finding our second property took a little longer than expected, and we actually got outbid once!

Eventually, we found a cozy 3 bedroom/2 bath condo built in 2002.

The condo had high-quality waterproof LVP flooring. The location was very close to our college, our first property, and my new company!

On top of that, the condo was also only 3-5 minutes from shopping districts with stores like Walmart and Costco. Talk about a great location!

Our Second Property

Outside of our second property/condo in Utah. Inside of our second condo in Utah. Three bedroom and two bath.

We highly recommend comparing and negotiating with at least three different lenders to get the best rate and deal at closing.

Sometimes smaller or less known lenders have more flexibility and can offer a better deal!

Here are some of the most commonly required documents when applying for a home loan or refinance. Your lender may ask for additional documents on a case-to-case basis.

2-year tax returns

Pay stubs, W-2s, or other proof of income

Bank statements and other assets

All of your debt monthly payment history

Credit score, credit history

Gift letters (if someone helps you with down payment etc.)

Photo ID, SSN

Rent history if you are renting, mortgage/HOA history if you are a house owner

House insurance company if you have a preference, usually it will cheaper when you bundle with car insurance.

If you have tenants, include rent payment history & current lease agreement.

The total price of the condo was $171,000. Our down payment + closing costs combined were around $10,000 total.

Our monthly payment with HOA and mortgage insurance included was $1,200.

When applying for the loan, we found out we had a collection account – which we had no idea about!

We ended up not getting the best interest rate due to the collection account, which was very tough at the time.

The interest rate ended up being around 5%. The good thing is that we learned a valuable lesson and have since become much more careful of our credit scores in the future.

During the one month of underwriting, we started renting our first property/townhome out and officially became first-time landlords! We had to contact our HOA to inform them we would be renting out our unit and provided a city rental license.

During our first year living in our first property, we remodeled and switched old appliances to new ones. We found the least expensive appliances to replace the old ones.

As college students, we both did not have much knowledge on how to remodel/rehab properties. I was also not a natural handyman, so we did not do a ton of remodeling before renting out our first property.

Thinking back, I regret not doing more remodeling since it would have let us rent at a higher price and would have added more value to the property.

Fortunately, the townhome was close to colleges, so renting out was not difficult.

We were happy to find a very nice newlywed couple as our first tenants.

We rented the unit out to them for $1000 a month, giving us $250 extra cash flow each month!!

Our realtor let us use a free rental agreement that she was also using. I remember when talking to our first tenants for the first time, and they were shocked we were the landlords at our young age.

If we can become first-time landlords in our early 20s, you can too; it’s never too late (or early) to start!

If you are tight on cash and looking for an affordable way to invest in Real Estate now, then FUNDRISE is an excellent choice. They provide a crowdsourcing real estate investing platform where the investing minimums are only $10.

Feel free to drop a comment below with your thoughts or questions!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you’re looking for tips on how to start investing in Real Estate in your 20s, you’ve come to the right place!

My first real estate property in Utah.

This post may contain affiliate links, please see our disclaimer for details.

In this article, I’m excited to share with you how my wife and I purchased our first real estate property in our early 20s. We were both college students, ages 21 and 23. I will also share eight tips to save up a downpayment, and much more.

You probably already know that investing in real estate at a young age can have many benefits.

When my wife and I were young college students we started looking for our first home.We learned firsthand how investing in real estate is possible, even for busy college students with low-paying jobs!

Shan (my wife) and I worked very hard to reduce our expenses, save more money, and find ways to make more money to build up our first down payment.

Purchasing your first home not only gives you a safe place for loved ones but also presents you with the opportunity to build wealth over the long term. There’s no better time to start investing than than RIGHT NOW!

If you prefer to watch this story, check out my YouTube video below!

How Our Real Estate Investing Started

Shortly after getting engaged to my sweetheart in December 2016, we discussed whether we should rent or buy a home after getting married.

My in-laws were landlords in China, so my wife grew up with investors and always had a fascinating perspective on real estate and investing.

People we knew would encourage us to rent since we were still in college, but Shan kept telling me we should work hard to buy a home instead.

My grandpa (father’s side) was a builder who owned many investment properties. So I was intrigued by the idea of buying a property that could be turned into an asset/rental property in the future.

The main concern was that it would be too expensive, but I was reminded how we don’t need the fanciest property on the block.

We would have the amazing opportunity to rent it out in the future instead of paying rent to a landlord. Not to mention extra passive cash flow each month… sounded pretty amazing to me.

Shan and I quickly agreed that our first property would NOT be a forever home but WOULD be an excellent investment opportunity!

So we started comparing locations and properties to find the best deal and place for our future rental.

Shan found a townhome in a stellar location – the unit was close to two prominent colleges. We both felt it would be a great investment property since it would be easy to rent out.

That’s when we started seriously discussing how to cut back on spending and save up enough money to purchase it!

An important lesson I learned when starting my investing journey was to think “how can I make something happen” instead of going to the default of saying “I can’t do that”, or “that’s too difficult at my age”.

My original plans were not to become a landlord at such a young age, but I realized that dreams are possible if you work hard at it – and having a partner who is on the same page financially certainly helps!

Remember that success is inevitable as long as you are determined, resilient, pivot when needed, and work hard.

Never put boundaries or limits on yourself when chasing your dreams and goals! Ok enough about our origin story; let’s jump into the juicy details.

How We Saved Up A Down Payment

1. Moved in with Parents: After my wife accepted my wedding proposal (sigh of relief that she accepted), we moved in with my parents. We were very fortunate to have this option which helped us to save more money.

2. Switched to full-time work: I switched from working a part-time job to a full-time job. All while going to school full-time.

3.Promoted at Work: Doing this provided a needed boost to our combined income. Not long after working full-time, I was promoted to bilingual supervisor with an additional bump in pay.

4.On-Campus Job Discounts: Shan was an international student and was only allowed to work on school campus as a part-time employee, but that didn’t mean there weren’t other perks to her job.

We both enjoyed discounts whenever we ate or shopped on campus. Doing so helped us cut down a lot on eating costs.

5. Help with Wedding Expenses: We are also fortunate to receive help with most of our wedding reception expenses from my parents with my in-laws helping cover other costs such as my wife’s dress and our honeymoon trip.

6. Not Buy Expensive Rings: The only thing we spent money on by ourselves for our wedding were our rings, but wait, we only spent $150. I was surprised but touched when Shan said she would rather put that money towards a downpayment.

In a nutshell, we saved as much as we could. We focused on doing everything possible to cut back on spending and only buy what we needed.

7. Sold Car: Another reason I was able to get some more cash is that I made the difficult decision to sell my luxury car. It was older and high in miles, so we couldn’t get a ton out of it but it helped quite a bit with our downpayment.

An accumulation of many small decisions saved us considerable amounts of money in the long run.

In May of 2017, Shan and I were happily married after just finishing another semester of school.

8. Summer Break = Work MORE: During that summer, I worked another additional job to save more money for our down payment (one full-time + one part-time job).

Three months later, we had finally saved enough money for a down payment. We could start looking for our first real estate property!!

Find The Best Real Estate Property, For Your Budget.

Shan and I looked at many locations and properties close to two colleges.

We calculated our combined income and set a budget. Maxing our mortgage out would have significantly restricted our cash flow each month.

The perfect property for our budget was a townhome listed for $100,000.

The property was built in 1970 with two bedrooms and 1.5 baths.

Although an older property, the previous owner did some nice remodeling like repainting walls and putting in new wood floors!

Our offer was accepted, and we couldn’t have been happier!!

Through all of our hard work, we were able to put down a $20,000 down payment. Since the down payment was 20% of the house value, we did not need to pay mortgage insurance!

Our monthly mortgage payment was just $850, including HOA, utilities, and internet.

I still remember on closing day when the title company worker said, “wow! your monthly mortgage payment is even less than the rental prices around here”.

It’s important to find the best rate and deal at closing. We highly recommend finding at least three different lenders to compare and negotiate with.

One of the lenders we worked with told us they would take a cut on their own commissions to give us the best deal.

If you are a first-time homebuyer, you may be wondering which documents you’ll need to give your lender.

Below are the most common documents you’ll need when applying for a home loan or refinance. Your lender may ask for additional documents on a case-to-case basis.

Common documents when applying for a mortgage:

2-years of tax returns

Pay stubs, W-2s, or other proof of income

Bank statements and other assets

All of your debt monthly payment history

Credit score, credit history

Gift letters (if someone helps you with a down payment etc.)

Photo ID, SSN

Rent history if you are renting, mortgage/HOA history if you are a house owner

House insurance company if you have a preference, usually it will be cheaper when you bundle it with car insurance.

If you have tenants, include your rent payment history & current lease agreement.

Our First Property 🙂

Our first real estate property in Utah. An old yet nice townhome built in 1970.

If you are tight on cash and looking for an affordable way to invest in Real Estate now, then FUNDRISE is an excellent choice. They provide a crowdsourcing real estate investing platform where the investing minimums are only $10.

Conclusion – FIRE Journey Ignited

By September 2017, we had successfully closed our first real estate property!

My wife was 21 years old, and I was 23. The underwriting process and everything took approximately one month to be completed.

Waiting for the underwriting and everything felt like forever since it was our first time going through the process. We were worried we might be denied the loan amount, but everything went smoothly, and we were approved.

Not only did we take a significant investment step, but we also kickstarted our FIRE journey!

We have become very passionate about taking control of our finances, living below our means, and making our money work HARD for us.

Check out other articles in our blog where we share our financial freedom stories with tips on personal finance & investing!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.