Breaking the chains of poverty can be a difficult task. It requires hard work, dedication, and, most importantly, change. The ten poor habits outlined in this article are commonly seen in those struggling financially.

If you want to improve your financial situation, it is important to break these poor habits and replace them with positive ones!

This post may contain affiliate links; please see our disclaimer for details.

1) You Don’t Have a Plan

How do you expect to achieve your financial goals if you don’t have a plan? Having a budget is one of the most important things you can do for your finances.

A budget allows you to track your income and expenses and adjust as needed.

2) You Live Paycheck to Paycheck

This is a common habit among those who are struggling financially. If you’re living paycheck to paycheck, you’re not saving money. It then becomes difficult to build an emergency fund or save for other financial goals.

To break this habit, you need to start budgeting and making a plan for your finances. Begin by setting aside money each month to save.

Even if it’s only a small amount, it can make a big difference in the long run.

3) You Have High Debt Levels

Another common habit among those who are struggling financially is high debt levels. This can make it difficult to manage your finances and make ends meet.

If you have high debt levels, it is important to create a plan to pay it off. Begin by making a list of all of your debts and their interest rates. You can focus on paying off the debt with the highest interest rate first or focus on paying off the smallest debt amount first with the Debt Snowball Method.

As you progress, you can start working on paying off the other debts.

4) You Don’t Invest

Investing is one of the most important things you can do for your finances. It allows you to grow your money over time and build wealth.

However, many people who are struggling financially don’t invest. This is usually because they don’t have the money to invest or don’t understand how it works.

If you’re not investing, it’s time to start. Begin by setting aside a small amount of money each month to invest.

You can then use this money to purchase stocks, bonds, or other investment products. As your investments grow, you’ll be on your way to building wealth.

5) You Don’t Have an Emergency Fund

An emergency fund is a savings account that you use to cover unexpected expenses. This could include medical bills, car repairs, or job loss.

Many people who are struggling financially don’t have an emergency fund. This can leave them in a tough situation if they experience an unexpected expense.

It would be best to start saving for an emergency fund to break this habit. Begin by setting aside a small amount of money each month. Doing this will help you build up enough savings to cover unexpected expenses.

My wife and I set up automatic transfers to a high-yield savings account, our Emergency Fund. It provides us with great peace of mind knowing we are prepared for the worst.

A great place to get started with your savings account isCIT Bank. They offer very competitive saving rates with no monthly maintenance fees.

With their Saving Connect Account, you can earn 12x the national average! There are no ATM fees, and you have the convenience of online banking.

If you don’t have a retirement plan, it’s time to start one. A retirement plan is a savings account used to save for retirement. Many people who are struggling financially don’t have a retirement plan. This can make it difficult to retire when you’re ready.

You must begin saving for retirement at the earliest possible age to break this bad habit. Start by setting aside a small amount of money each month.

By building up your retirement savings, you’ll be on your way to a comfortable retirement.

Increasing your income is essential to your financial freedom. Many individuals who are struggling financially suffer from this issue. It often stems from a limited belief about their earning potential.

In this situation, looking for ways to increase your income is important. This could include getting a better-paying job or starting a side hustle.

Making more money is a great way to break the cycle of poverty. If you can find ways to increase your income, you’ll be on your way to financial success.

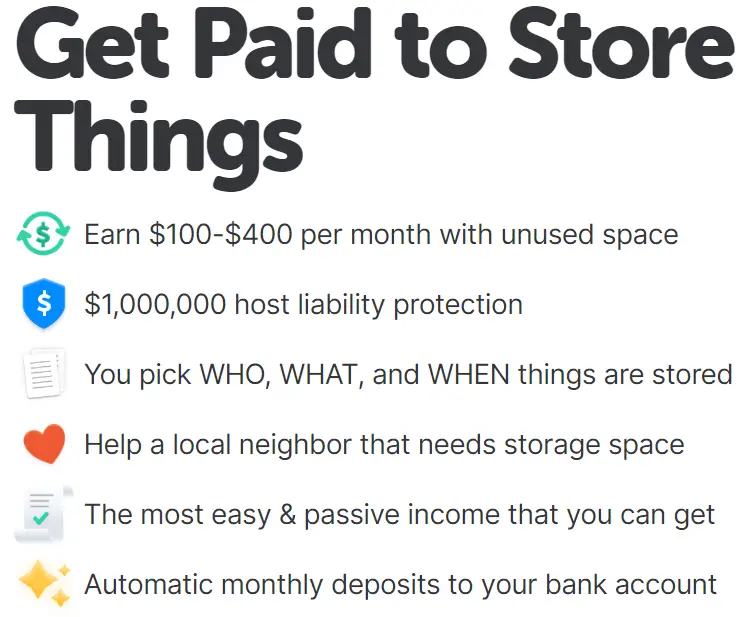

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

8) You Don’t Have or Stick to a Budget

If you don’t have a budget, it can be not easy to manage your finances. A budget is a plan for your money that helps you track your spending and ensure you’re not overspending.

Many people who are struggling financially don’t have a budget. This can make it difficult to stay on track with your finances.

To break this habit, you need to create a budget. Begin by tracking your spending for one month. This will help you see where your money is going and how much you spend each month.

Once you understand your spending well, you can create a budget that will help you stay on track.

9) You Don’t Stay Disciplined

Discipline is essential for financial freedom. It can be not easy to manage your finances without out. This is a common problem for many people who are struggling financially.

In this situation, it’s important to find ways to stay disciplined. This could include things like setting up a budget or tracking your spending. Staying disciplined is a great way to break the cycle of poverty.

10) You Don’t Live Within Your Means

Making ends meet can be difficult if you don’t live within your means. Finding ways to cut back on your spending is important in this situation. This could include things like eating out less or downsizing your home.

Poor spending habits can often be caused by insecurity or not having delayed gratification.

For example, if you want something but can’t afford it, you may be tempted to put it on a credit card. This can lead to debt and further financial problems. If you’re struggling to live within your means, finding ways to curb spending is important.

There are some simple rules that you can follow to help live below your means. The 50/30/20 rule is one such rule.

The method states that you should allocate 50% of your income toward essentials, 30% towards wants, and 20% towards savings.

All in All

These are just a few of the common habits that keep you poor. If you want to improve your financial situation, it is important to break these poor habits and replace them with positive ones.

If you break these habits, you’ll be on your way to financial success!

A plan to achieve your financial goals, budgeting, investing, saving, living within your means, and paying off debt are great ways to start. Breaking the chains of poverty can be difficult, but it is possible.

With hard work and dedication, you can achieve your financial goals. So don’t give up and keep working towards your goals. You can achieve anything you set your mind to.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

I never imagined that a book could have such a profound impact on our lives. After reading Total Money Makeover by Dave Ramsey, I realized that I had been living beyond my means and was in debt up to my eyeballs.

The book taught me five important lessons that changed my thoughts about money.

In this article, we will discuss those five lessons in detail.

If you are struggling with your finances, then know these lessons could change your life too!

This post may contain affiliate links; please see our disclaimer for details.

Book Summary (Total Money Make Over – Dave Ramsey)

Ramsey’s book is based on the idea that ‘we must live like no one else now so that later we can live like no one else.’

In other words, we need to make sacrifices now to enjoy a comfortable retirement later.

The book covers various topics, such as how to get out of debt, save for emergencies and retirement, and invest wisely.

Ramsey also stresses the importance of giving back to charity.

What resonated with me were the five key lessons that he discusses in detail:

The first step to getting your finances in order is to create a budget. This may seem like a no-brainer, but you’d be surprised how few people do this.

A budget forces you to be mindful of your spending and helps you make better financial decisions.

Once the written budget is created, you can better understand where your money is going each month.

You may be surprised that you are spending more than you realized on unnecessary items.

Creating a budget is the first step to taking control of your finances.

It may not be the most exciting task, but it is necessary if you want to achieve financial success. He recommends including insurance for the following items in your written budget:

Auto and homeowner insurance

Life insurance

Long-term disability

Health insurance (If your nation/state does not provide this)

Long-term care insurance

Although adding insurance bills to your budget is never fun, they can save you a lot of money in the long run.

Items that can be removed from your budget are:

Cable TV

New cars

Eating out

Clothes shopping

Gym memberships

Latte factors (small, daily expenses that can add up)

These are just a few examples, but the point is that you need to be mindful of your spending.

Once you have a handle on your spending, you can start to make changes that will help you save money.

Lesson #2 – Create a Debt Snowball

I created a Debt Snowball by listing all my debts, regardless of interest rate, from smallest to largest.

Next, I made the minimum payments on all my debts except the one with the smallest balance. I paid as much as I could afford each month on that debt.

I was motivated to stay out of debt because I saw my balances going down each month.

This system also allowed me to pay off my debt faster because I put more money into the smaller debts first.

If you’re struggling with debt, I encourage you to try the Debt Snowball method. It works!

Starting with the highest interest rate could save more money in the long run, but psychologically, this method was the best for me, and we had low-interest rates.

3) Save for Retirement Now

Delayed gratification and thinking long-term are two important aspects of personal finance. Dave Ramsey famously said –

“Adults devise a plan and follow it, children do what feels good“.

Dave Ramsey

It’s never too early to start saving for retirement, and the sooner you start, the more time your money has to grow.

Ramsey suggests investing 15% of your household income into tax-advantaged accounts.

I knew retirement was in the cards but I realized I could start preparing better and preparing NOW.

We are maxing out our Roth IRA contributions each year, and I am on track to retire much sooner than I ever thought possible.

4) Pay Cash for Everything: Cash IS King

Spending with credit cards reduces the brain’s ability to feel pain.

When we make a purchase using cash, it feels much different than when we use a credit card. That’s because we physically see the money leaving our hands.

But when we use a credit card, it doesn’t feel like we’re spending real money. This can lead to overspending and accumulating debt.

It’s important to be mindful of your spending and only charge what you can afford to pay off each month.

You can earn slightly more money from credit card cash back, but it’s important to consider psychological factors. Credit card companies are very good at getting us to spend more money than we have.

It’s important to be aware of this and only use the credit card as a tool to build credit, not for shopping sprees.

Although the lessons taught in this book about credit cards are valuable, we’ve found that using a credit card wisely has many benefits.

Just be aware, do not overspend, and pay down credit cards on time – just our thoughts on this topic.

For most people, the mortgage is the biggest expense.

The author advocates for paying off your mortgage as quickly as possible so you can be debt-free and have more financial freedom.

There’s a saying that the grass feels different in your yard once you’ve paid off your mortgage because you fully own that land.

We, the Biesinger’s, personally feel investing at a young age is important, and real estate is generally increasing in value over the years. For these reasons, we have not started paying off our mortgage early yet, but it could be an option in the future.

Dave Ramsey’s lesson here is to take a zero-risk approach, but we want to have a small amount of risk to see more significant returns.

The choice is ultimately yours; paying off the mortgage provides peace of mind, but mathematically speaking, investing that money in the S&P 500 has more significant rewards.

You won’t be able to turn your financial life around overnight.

It took me years of bad spending habits to get into the mess I was in; my Wife and Dave Ramsey were able to help me correct those bad habits.

I could make significant changes in my financial life by taking small steps.

I started by reading this book and then implementing the lessons I learned.

Over time the steps brought me to accomplish my financial goals, even though they were small.

Try these baby steps from Dave Ramsey if you are struggling with finances. Like us, you can emphasize specific steps, such as getting out of debt but also focus on investing.

In Summary

This book is a great place to start if you want to pay off your debt or improve your financial situation.

It gave me a great personal finance perspective, and I’m sure it can do the same for you.

I recommend this book to anyone who wants to get their finances in order.

It’s an easy read and packed with valuable information to help you make better financial decisions.

If you’re looking for a personal finance book that will change your life, look no further than Total Money Make Over.

If finances overwhelm you, don’t worry because many people like me were in your shoes before reading this book.

The lessons I learned from Total Money MakeOver has helped me get my finances in order.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

When it comes time to buy or lease a new car, there are a lot of factors to consider.

You may be asking yourself the following questions:

What’s the difference between leasing and buying?

What are the pros and cons of each option?

In this blog post, we’ll break it all down for you!

We’ll discuss the benefits and drawbacks of leasing vs. buying a car, so you can decide what’s best for you. 🙂

My YouTube Video Sharing The Differences Between Leasing or Buying a Car

What’s the difference between buying and leasing a car?

The biggest difference between buying and leasing a car is that you own it outright when you buy a car.

You can sell it, trade it in, or keep it for as long as you want.

When you lease a car, on the other hand, you’re essentially renting it from the dealership for a set period (usually two to four years).

At the end of your lease term, you can buy the car, return it to the dealership, or lease another one.

Another difference is that you’re responsible for all repairs and maintenance when you buy a car.

However, the dealership is typically responsible for any necessary repairs or maintenance with a leased car.

Another difference is that when you buy a car, you are spending a lump sum of cash or taking out a loan to pay the car in full.

When you lease, on the other hand, you’re only responsible for paying a monthly fee to use the car.

If you miss payments on a lease, the dealership can repossess the car.

If you miss payments on a loan for a car you’ve bought, the lender can repossess the car as well.

However, if you buy the car in full, you won’t have any payments and won’t risk losing the car to repossession.

Another key difference between buying and leasing a car is that when you buy a car, its value depreciates as soon as you drive it off the lot.

With a leased car, you’re only responsible for the depreciation during your lease term.

Car ownership is also a larger commitment to the vehicle as it may be difficult to get out of a car loan.

We recommend buying a reliable car with cash if at all possible and explain this further in an article I wrote – 6 Reasons to Buy a Car with Cash

If you bought the car and it breaks down shortly after, you may be “stuck” with the car until it is fixed or find another transportation source.

On the other hand, if you lease a car and it breaks down, you can bring it back to the dealership and get a new one without worrying about repairs.

A lease can be more flexible as you can return the vehicle or upgrade to a new one at the end of the lease term.

To summarize, here are the key differences between buying and leasing a car:

When you buy a car, you own it outright. When you lease a car, you’re essentially renting it from the dealership for a set period.

The dealership is typically responsible for necessary repairs or maintenance with a leased car. You’re responsible for all repairs and maintenance when you buy a car.

You’re responsible for the entire purchase price when you buy a car. When leasing, you’re only responsible for paying a monthly fee to use the car.

If you miss payments on a lease, the dealership can repossess the car. You don’t have to worry about repossession if you buy the car.

Pros and cons of leasing a car

Leasing a car has its pros and cons, like everything else. Here are a few things to consider if you’re considering leasing a car.

PROS

You can drive a brand new car every few years.

Leasing generally has lower monthly payments than buying.

The warranty covers most repairs when you lease, so you don’t have to worry about unexpected costs.

You may be able to get into a nicer car than you could afford to buy outright.

CONS

At the end of the lease, you don’t own anything.

You’re restricted in how many miles you can drive each year. Going over the limit will cost you.

You may have to pay extra fees at the end of the lease if you want to keep the car or if there’s damage.

Leasing generally means higher insurance payments than if you owned the car outright.

So, those are a few things to consider before leasing a car. It’s not necessarily the right choice for everyone, but it could be a good option for some people. Weigh the pros and cons and make the best decision for you.

Do your research before signing a lease to ensure you understand all the fees and restrictions. And be sure to drive safely and within the mileage limits to avoid extra charges!

Pros and cons of buying a car

Like leasing, there are pros and cons to buying a car. Here are a few things to consider if you’re considering buying a car.

PROS

You own the car outright and can do what you want with it.

There’s no mileage limit, so you can drive as much as you want.

You don’t have to worry about extra fees at the end of the lease term.

Insurance is generally cheaper when you own the car.

CONS

The initial purchase price is usually higher than leasing.

You’re responsible for all repairs and maintenance costs.

You may have difficulties selling the car later on down the road.

So, those are a few things to consider before buying a car. As with leasing, it’s not necessarily the right choice for everyone.

Examine each option’s advantages and disadvantages so you can make an informed decision.

Before purchasing a vehicle, do your homework and make sure you know all the expenses and limitations.

And be sure to drive safely to avoid any accidents!

Should You Buy or Lease a New Car?

Ultimately, it depends on your individual needs and circumstances.

If you like to have the latest and greatest car every few years, leasing might be the best option.

But buying might be the way to go if you want to keep your car long-term and don’t mind taking on repair costs.

There are a few other things to remember when deciding whether to buy or lease a car.

For instance, buying might be a better option if you plan to drive more than 15,000 miles per year since most leases have mileage limits.

And if you like to customize your car, buying might also be the better choice since you can make any modifications you want without worrying about violating the terms of your lease.

Another thing you should consider is your credit score. If you have good credit, you’re more likely to get a lower interest rate when financing a car purchase.

But if you have bad credit, you might not be able to qualify for an auto loan at all. In that case, leasing might be your only option.

Buying a car with upfront cash can also open you to opportunity costs.

For example, a $10,000 car will begin to lose its value within a year, but if a stock doubles over the next year, you would have been better off investing that money.

It is typically cheaper to lease a car than to buy one outright, but buying might be the more cost-effective option if you want to own the car long-term.

Ultimately, it depends on your financial circumstances and your driving habits.

It all comes down to personal factors and requirements.

There are benefits to buying a car and owning a vehicle, but it’s important to remember the opportunity costs or loan obligations of the purchase.

Leasing a car can be cheaper in the short term, but it’s important to be aware of mileage limits and other restrictions.

Do your research and make the best decision for you!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Millions of people are in the same situation around the world. We spent a lot of time and used many strategies to get out of debt ourselves!

This article will discuss 11 strategies that can help you get out of debt fast!

1) Know Where Your Money Comes and Goes

Couple Budgeting

The first step to getting out of debt is building awareness of your money and creating a budget. You need to know how much you are bringing in and how much you are spending.

Once you have a good understanding of your finances, you can start making changes to your spending habits.

How To Start This Strategy: Start by creating a budget. You can use a simple spreadsheet or an online budgeting tool.

Once you have your budget, start tracking your spending.

Make sure to include all your expenses, including credit card payments, groceries, and gas.

Why This Works: This strategy works because it gives you a good understanding of your finances.

Once you know where your money is going, you can start changing your spending habits.

2) Cut Down on Expenses

Once you have a budget, it’s time to start cutting expenses. These first two pay-off debt strategies are crucial.

Look for ways to reduce your monthly expenses. You may need to make some lifestyle changes, but it will be well worth it.

How To Start This Strategy: Start by evaluating your monthly expenses.

Where can you cut back?

Are there any unnecessary expenses that you can eliminate?

Once you have identified areas where you can cut back, start changing your spending habits.

Why This Works: This strategy works because it allows you to save money each month.

The more money you can save, the faster you can get out of debt and avoid more consumer debt.

3) Increase Your Income

If you want to get out of debt fast, you must find ways to increase your income.

If you can’t find a way to increase your income, you may need to consider finding a new job or starting a side hustle.

How To Start This Strategy: If you’re looking for a new job, start by evaluating your skills and experience.

What are you good at?

What do you enjoy doing?

Once you understand your strengths, start searching for jobs that match your skill set.

You can also increase your income by creating passive income-producing assets.

This can include starting a blog, an online business, or investing in dividend-paying stocks.

Why This Works: This strategy allows you to bring in more monthly money. The more money you have coming in, the faster you can pay off debt.

4) Make More Than the Minimum Payment

If you only make the minimum payment on your debts, they will take forever.

It would be best if you started making more than the minimum payment to get out of debt quickly.

How To Start This Strategy: Start by evaluating your monthly expenses.

How much can you afford to put toward your debt each month?

Once you understand your finances, start making more than the minimum payment on your debts.

Why This Works: This strategy allows you to pay off your debt faster and save money on interest.

The more money you can put towards your debt each month, the quicker you will be able to get out of debt.

By paying down the principal balance, you are effectively paying less interest each month.

6) Snowball Your Debt Payments

One of the best ways to get out of debt is to snowball your debt payments.

Start by listing out all of your debts from smallest to largest, and focus on paying off the smallest debt first.

Once you have paid off the smallest debt, you move on to the next one, and so on. This creates a momentum effect and can help keep you motivated!

Why This Works: This strategy allows you to focus on one debt at a time.

Focusing on one debt makes you more likely to pay it off successfully.

You’ll put all your extra money towards the debt until it is paid off.

Once you have paid off a debt, you will have more money available for the next one.

6) Attack Your Highest Interest Rate Debt First

Another popular strategy for getting out of debt is to attack your highest interest-rate debt first, otherwise known as the Debt Avalanche Method.

This will save you money in the long run because you will be paying less in interest, and is a good option when you have debt with high-interest rates.

Why This Works: This get-out-of-debt strategy works because it allows you to save money in the long run.

The less interest you pay, the more you will have to put toward your monthly debt.

Doing so can help you pay off your debt more quickly.

7) Refinance Your Debt

If you have high-interest debt, you may be able to save money by refinancing your debt.

You can take out a new loan with a lower interest rate and use the money to pay off your high-interest debt.

Why This Works: This strategy works because it allows you to save money on interest.

When you refinance your debt, you will have a lower interest rate, which means you will pay less monthly interest.

Ultimately this will help with your monthly cash flow.

8) Stop Adding More Debt

If you want to get out of debt, you need to stop adding more debt.

Stop using high-interest credit cards and taking out loans.

You need to live within your means and only spend the money that you have.

Why This Works: This strategy allows you to focus on paying off your existing debt.

When you stop adding more debt, you can focus on paying down the debt that you already have.

Eliminate your financial troubles sooner by starting to use this method today!

9) Use a Debt Settlement Program

If you are struggling to make your monthly payments, you may be able to use a debt settlement program.

This option can help you reduce and get out of debt quickly.

Why This Works: This method works because it can help you reduce your debt.

When you use a debt settlement program, you will negotiate with your creditors to lower your interest rates and monthly payments.

Doing this can help you get out of debt fast.

10) Sell Unused Items

If you have items that you no longer use, you can sell them and use the money to pay off your debt.

Selling unused items is a great way to eliminate clutter and make extra money.

You may realize that you have hundreds or even thousands of dollars worth of stuff you no longer need.

Instead of having it collect dust, you can use it to reduce your debt liabilities.

How To Start This Strategy: First, you would want to go through your house and list items you no longer need or use.

Once you have this list, you can start listing these items for sale online or have a garage sale.

You can use your money from selling these items to pay down your debt.

You can easily combine strategy #3 above (increasing income) and this one by renting out your extra space after selling unused items. That’s why we love NEIGHBOR!

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

Why This Works: This method works because it allows you to make extra money to put towards your debt.

When you sell unused items, you may receive a lump sum of cash, and you can pay off the principal of your debt with that profit.

11) Switch To A More Affordable Phone Plan

Another one of the pay-off debt strategies is to lower your monthly phone bill, thus allowing you to have more money to pay off debt.

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

Get Out Of Debt Strategies Conclusion

If you are struggling with debt, know there are many options available to you!

You just need to find the right one for your situation.

Use these strategies to get out of debt fast. Do not feel discouraged if you cannot pay off your debt overnight.

Just keep working at it and you will eventually get there.

Debt can be a burden and the faster you can get out from under it the better.

The following are eleven pay-off debt strategies that can help you achieve this goal.

By having a financially wise strategy and deploying discipline, you can be debt-free in no time!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Looking to improve your credit score fast? Don’t worry, you’ve come to the right place.

It’s no secret that mortgage rates are on the rise. According to CNBC, “In just a matter of months, mortgage rates have surged just over 3% for a 30-year fixed loan to just north of 5%”.

This article will discuss 13 genius tips that will help boost your credit score! Follow these tips, and you’ll be on your way to a better credit rating in no time.

You can check out our YouTube video if you prefer to watch instead of reading.

In this day and age, your credit score is super important. A good credit score can help you qualify for a loan, get a lower interest rate, and rent an apartment.

On the other hand, a bad credit score can result in higher interest rates and difficulty getting approved for loans.

That’s why it’s important to do everything you can to improve your credit score.

And fortunately, there are a few simple things you can do to give your score a boost.

This post may contain affiliate links; please see our disclaimer for details.

How are credit scores calculated?

Credit scores are calculated based on several factors, including:

Payment history

Credit utilization

Length of credit history

Types of credit

New credit inquiries

Let’s take a closer look at each of these factors and how you can improve your score in each area.

Payment history is one of the most important factors in determining your credit score.

Therefore, it’s important to always make your payments on time.

If you have missed any payments in the past, now is the time to start making them on time. This will show creditors that you’re serious about paying your debts and improve your chances of getting approved for new loans.

Credit utilization is another important factor in determining your credit score.

This is the amount of credit you’re using compared to the amount of credit you have available.

For example, if you have a credit card with a $1000 limit and you’re carrying a balance of $500, your credit utilization would be 50%.

You can improve your credit utilization by paying down your debts and keeping your balances low.

Creditors like to see that you’re not maxing out your credit cards, so this is a great way to improve your score.

Length of credit history is another factor that lenders look at when determining your creditworthiness.

The longer you’ve been using credit, the better.

Therefore, it’s important to keep old accounts open even if you don’t use them often.

Creditors will see and care that you have a long history of responsible credit use.

Types of credit also affect your credit score. Creditors like to see that you’re using a variety of different types of credit, such as revolving credit (e.g., credit cards) and installment loans (e.g., auto loans). This shows that you’re able to manage different types of debt responsibly.

New credit inquiries are the last factor we’ll discuss. Whenever you apply for new credit, it will result in a hard inquiry on your report.

Too many hard inquiries can hurt your score, so it’s important to only apply for new credit when you really need it.

Now that we’ve discussed the factors that go into your credit score, you might be wondering, does a good credit score matter? The simple answer is yes.

Why Does A Good Credit Score Matter?

A good credit score can save you money. A bad credit score can cost you money. It’s as simple as that.

For example, let’s say you’re looking to buy a new car. If you have good credit, you’ll likely qualify for a lower interest rate on your loan. This could save you hundreds or even thousands of dollars in interest payments over the life of the loan.

On the other hand, if your credit is poor, you may not qualify for a loan at all. Or, if you do qualify, you’ll likely be stuck with a high-interest rate which will end up costing you more in the long run.

A good credit score can also help you get into an apartment.

Many landlords check your credit score before approving you for a lease application. And if your score is low, you may be denied service or required to pay a deposit.

Another reason why a good credit score is important is that it can help you get a job. Many employers will check your credit history as part of the hiring process. And if your score is low, it could be a red flag for them and they may decide to hire someone else instead.

As you can see, having a good credit score is important for many different reasons. Fortunately, there are a few simple things you can do to improve your score.

So a good credit score is important because it can save you money and help you get approved for the things you need in life. By following the tips we’ve discussed in this article, you can start boosting your credit score today!

How To Increase Your Credit Score?

Now, let’s discuss how you can increase your credit score.

Here are 13 genius tips to improve your credit score fast…

Before we begin, it’s important to note that there is no one-size-fits-all solution when it comes to improving your credit score.

What works for one person might not work for another. So, take these tips as general guidelines and tailor them to your own situation.

Tip #1: Pay your bills on time

One of the biggest factors that affect your credit score is your payment history.

So, if you want to boost your credit score fast, you need to make sure that you’re always paying your bills on time.

Even one late payment can negatively impact your credit score, so it’s important to be vigilant about making all of your payments on time, every time.

Tip #2: Keep your balances low

Creditors like to see that you’re not maxing out your credit cards, so keep your balances low.

You can improve your credit utilization by paying down your debts and keeping your balances low.

Tip #3: Use a mix of different types of credit

Creditors like to see that you’re using a variety of different types of credit, such as revolving credit, installment loans, and even store credit cards.

So, if you want to boost your credit score fast, make sure to use a mix of different types of credit.

Tip #4: Check your credit report regularly

Another important tip to boost your credit score fast is to check your credit report regularly. This will help you catch any errors or discrepancies that could be dragging down your score.

You can get a free credit report from each of the three major credit bureaus once per year.

Remember always to ensure that it is a soft check, not a hard one. Keep reading as we go over the differences between the two.

Tip #5: Dispute any errors on your credit report

If you do find any errors on your credit report, make sure to dispute them right away. You can do this by writing a letter to the credit bureau that issued the report.

Tip #6: Use automatic payments

One easy way to make sure that you’re always paying your bills on time is to set up automatic payments.

That way, you’ll never have to worry about forgetting a payment or being late on a payment.

Tip #7: Consider a balance transfer

If you have multiple high-interest credit cards, another great way to boost your score is to transfer the balances to a single low-interest card. This will help reduce your overall debt and show creditors that you’re working to pay off your debts.

Just make sure you don’t incur any new debt on the cards while you’re working on paying off the balance transfer.

Tip #8: Use a credit monitoring service

If you want to keep an eye on your credit score and ensure you’re always taking steps to improve it, consider using a credit monitoring service.

These services can help you track your progress and give you personalized tips to improve your score.

Tip #9: Get help from a professional

If you’re having trouble boosting your credit score on your own, consider getting help from a professional.

A credit counselor or financial advisor can provide valuable guidance and help you create a plan to improve your credit score.

Tip #10: Ask for a higher credit limit

A helpful tip to consider if you want to boost your credit score is to get a credit card with a higher limit. This will improve your credit utilization and show creditors that you can manage more credit responsibly.

Just make sure you don’t max out the card and always pay your bill on time. If you do, you’ll see a significant boost in your credit score in no time.

Tip #11: Prepay the balance and plan ahead

If you know you’ll be carrying a balance on your credit card for a couple of months, one way to avoid paying interest is to prepay the balance.

This way, you can pay off the entire balance before interest accrues. Have the money available in your account so you don’t overdraw and incur fees.

This helps to prevent you from going over your credit utilization ratio for larger purchases.

It’s a good idea to have a couple of months’ worth of payments saved up so you can prepay when necessary.

Tip #12: Get a lower interest rate credit card

Another tip to consider if you want to boost your credit score is to get a credit card with a lower interest rate.

Doing so will help you save money on interest and show creditors that you’re a responsible borrower.

Tip #13: Stay patient

Last but not least, it’s important to stay patient when you’re trying to boost your credit score.

It takes time to make improvements, so don’t get discouraged if you don’t see results overnight. Just keep working at it and you’ll eventually see the improvements you’re looking for.

Take these 13 genius tips and put them into action to boost your credit score fast!

Remember –

The sooner you start working on improving your credit, the better off you’ll be in the long run.

So don’t wait – get started today!

How Long Does It Take To Rebuild Credit?

The answer to this question largely depends on your credit situation. If you have a long history of late payments, it will take longer to rebuild your credit than if you have a shorter history or no late payments.

You can expect changes every 30 to 45 days, so it may take a few months to see significant improvement. It’s important to do a soft credit check, not a hard credit check, as the latter can harm your score.

Soft Credit Check: This type of credit inquiry does not impact your credit score. This is the ideal type of credit check to do if you are looking for new credit, such as a credit card or loan.

Hard Credit Check: This type of credit inquiry will show up on your credit report and temporarily lower your credit score. This is the type of credit check you should avoid if at all possible.

Patience is important when rebuilding your credit. The key takeaway is to follow all these steps and avoid the common mistakes that could hurt your progress.

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

By following the 13 genius tips above, you can give yourself a much better chance of success. Do your best to stay patient and consistent with your payments, and you’ll eventually see your score improve.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Getting approval for a home mortgage may not be easy, especially if you are a first-time homebuyer. Lenders look for many things when deciding whether or not to approve a mortgage application.

According to Forbes, about one-third of Americans without a high credit score are rejected for a home loan mortgage.

This blog post discusses 15 expert tips to increase your chances of getting approved for a home mortgage!

This post may contain affiliate links; please see our disclaimer for details.

Being approved for a mortgage can be a nightmare if you do not know these strategies and tips. This is because a mortgage is a large loan, and lenders are careful when they lend their money.

They want to make sure that you can repay the loan, and they will look at various factors to determine this.

So let’s jump into the 15 tips I’ve prepared!

1) Track all income and expenses.

One of the most important things you can do before applying for a mortgage is to create a budget and stick to it. Know where all your money is coming from and leaving to.

This will show the lender that you are financially responsible and can stay disciplined within your budget. It is important to include all of your income and expenses in your budget, including debts and bills.

Lenders want to see that you can afford your monthly mortgage payments, other expenses, and/or debt payments.

If you show them that you can live within your means, they will be more likely to approve your mortgage application!

Another thing that lenders look at when considering a mortgage application is the amount of money you have saved up for a down payment.

The more money you can put down on your home, the more likely you will get approved for a mortgage.

Generally, if you cannot put down a 20% down payment, you will need to pay mortgage insurance.

The larger the down payment, the lower your monthly payments will be, and the more likely you will get approved for a mortgage.

If you struggle to get a mortgage, a lower total loan amount can help. Saving up can be difficult but well worth it in the long run. I wrote another article specifically sharing 15 Frugal Living Tips to Save a Ton of Money; feel free to check it out!

3) Have a good credit score.

Lenders consider your credit score one of the most important factors when approving a mortgage application.

If you have a good credit score, it will show lenders that you are responsible for your finances.

If you have any negative items on your credit report, it is important to clean them up before applying for a mortgage.

This will show lenders that you are improving your finances and are more likely to make your monthly payments on time.

To boost your credit score, make sure to pay your bills on time, keep your credit utilization low, and don’t apply for too many loans at once.

4) Get pre-approved for a mortgage.

Getting pre-approved for one is a good idea if you want to increase your chances of getting approved for a mortgage.

This means that you have already been through the underwriting process and have been given conditional approval for a mortgage loan.

Doing so will give lenders confidence that you are a good risk and increase your chances of getting your mortgage approved.

You can use a traditional or an online lender to get a pre-approved mortgage.

Online lenders can often give you a decision more quickly, but they may not have as many loan options available.

5) Have a solid job history.

Lenders also look at your job history when considering a mortgage application.

They want to see that you have been employed for two years, which shows stability and responsibility.

If you have been unemployed or had a lot of job changes, it may not be easy to get approved for a mortgage.

6) Have a low debt-to-income ratio.

Another thing that lenders look at when considering a mortgage application is your debt-to-income ratio. This is calculated by dividing your monthly debts by your monthly income.

Lenders want to see that you can afford to pay for debt payments, along with all of the other living expenses.

If you show them that you can handle debt effectively, it can help raise your chances of being approved for a mortgage.

We were able to pay off $56,000 of school loan debt by using the debt snowball method, this helped lower our DTI significantly!

Tips for raising your income:

Job hunting

Ask for a raise

Start a side hustle

Invest in assets that produce passive income

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

A low debt-to-income ratio is important for mortgage approval.

For example, consider the two following scenarios:

Consistent income of $100,000 per year and have $0 in debt.

Earning $15,000-$20,000 per year and having $10,000 in debt.

If you were a mortgage lender and only had money to invest in one borrower, which one would you choose to lend to? The answer is clearly number one.

7) Save up for closing costs.

When applying for a mortgage, you must save up for closing costs.

These are the fees and expenses that are associated with getting a mortgage. Closing costs typically range from about three to five percent of the total loan amount, so it is important to budget for them.

By showing your lender that you are prepared for all the costs associated with getting a mortgage, you will increase your chances of getting approved.

8) Get help from a Mortgage broker.

If you are unsure how to get approved for a mortgage or have been denied, it may be helpful to work with a mortgage broker.

A mortgage broker can find you the best possible deal on a mortgage and help you navigate the application process.

9) Wait until you are ready.

One of the most important things to remember when applying for a mortgage is to wait until you are ready.

Don’t apply for a mortgage unless you are sure that you can afford the monthly payments. This will only lead to disappointment and could damage your credit score.

Your lack of confidence in paying your monthly payments will cause lenders to disapprove your application.

11) Start building credit ASAP

If you don’t have a lot of credit history or do not have a good credit score, it is important to start building credit (or fixing it) as soon as possible.

This will show lenders that you are responsible with money and can be trusted to make your monthly payments on time.

When applying for a mortgage, shopping around for the best options is important. This means comparing interest rates, terms, and fees from different lenders.

By doing your research, you can find the mortgage that is best for you.

The more mortgage options you have, the more likely you will be approved by at least one. However, it’s still important to consider the other tips on this list.

12) Find a co-signer

If you have difficulty getting approved for a mortgage, you might consider finding a co-signer.

A co-signer agrees to sign the loan with you and is responsible for making the payments if you default. This can be a family member, friend, or business partner.

The co-signer will need to have good credit and a steady income. And they should be aware of the risks involved before agreeing to sign the loan.

If you default on the loan, the co-signer will be responsible for the debt, and their credit will be impacted. So it is important only to use a co-signer as a last resort.

13) Rent to own

This is a type of contract in which you agree to rent a property for a specific period, with the option to purchase it at the end of the lease.

This can be a helpful way to get approved for a mortgage if you don’t meet all the requirements.

15) Lease options

This is similar to renting to own but gives you the option to buy the property immediately instead of waiting until the end of the lease.

This can be a good option if you are unsure if you want to purchase the property.

15) Government-backed loan

If you have difficulty getting approved for a mortgage, you may consider a government-backed loan.

These loans are backed by the federal government and have more flexible requirements than traditional mortgages.

Government-backed loans include FHA loans, VA loans, and USDA loans. Each loan program has eligibility requirements, so be sure to research which is right for you.

You may also want to talk to your local housing authority about government-sponsored mortgage assistance programs.

Conclusion

These are just a few tips that can help you get approved for a mortgage.

Be sure to research and talk to a lender about the best options. And remember, it’s always best to prepare for a mortgage well in advance.

Following these tips can improve your chances of getting approved for a mortgage. We wish you the best on your purchasing home journey.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.