This post may contain affiliate links; please see our disclaimer for details.

First, I would like to share some interesting numbers with you.

The average monthly car payment in the U.S. is $563 for new vehicles, $397 for used vehicles, and $450 for leased vehicles.1

If you invest $563 a month in a reliable fund such as the S&P 500 with an average 12% return, you will have around $130,000 in 10 years and ONE MILLION in 25 years!

The average value of a new vehicle drops around 20% in the first year of ownership and will drop up to 60% of its value within the first five years! 2

Back in the day, I took out a car loan to buy a land rover. This vehicle later became my worst nightmare. If you want to know more about this story, you can visit the article I wrote about why financing a car can be a bad decision.

I am very grateful to have later learned about Dave Ramsey. After watching many of his videos, my wife and I insisted on buying a car with cash.

So let’s dive in and see the 6 reasons to buy a car with cash!

1. Avoid Interest

If you don’t finance a car purchase, you can save a lot of money by avoiding interest payments on the car loan.

This may seem completely obvious but is worth repeating.

“The average auto loan rate is 3.64% for new cars and 5.35% for used cars”, according to Experian.

Paying interest on a car may seem normal, but it is not beneficial and will make your lender very happy and wealthy.

2. No Monthly Car Payments

Since my wife and I own our car and purchased it with cash, we don’t have any additional car monthly payments – this has greatly reduced our monthly expenses!

That’s one reason why we can save 56% of our income and allow us to invest more in our future.

Monthly payments means living paycheck to paycheck and not experiencing true financial freedom.

It’s a big deal if someone suddenly loses their job or has other emergency expenses that need to be resolved. Keeping expenses low and savings plus investments high is important to have peace of mind.

Instead of paying a monthly payment to a car that won’t hold its value, why not spend it where it will appreciate?

For example, a great place to put the extra money saved from not paying interest payments could go towards retirement/tax-advantaged accounts such as a Roth IRA, 401(k), HSA, etc.

“The average monthly car payment in the U.S. is $563 for new vehicles, $397 for used vehicles, and $450 for leased vehicles.” 1

If you invest $563 a month in a reliable fund such as the S&P 500 with an average of 12% return, you will have around $130,000 in 10 years, and ONE MILLION in 25 years!

3. Depreciation Doesn’t Matter

“According to industry experts, the value of a new vehicle drops by about 20% in the first year of ownership. Over the next four years, you can expect your car to lose roughly 15% of its value each year – meaning the average car will be worth just 40% of its purchase price after five years:

A 5-year-old vehicle that sold for $40,000 when new will be worth $16,000.

A 5-year-old vehicle that sold for $30,000 will be worth $12,000.” 2

What does depreciation mean?

The difference between the price you pay and the price you can sell something is called depreciation.

Cars depreciate quickly, especially new cars. The moment you leave the parking lot on a brand-new car, it starts to lose its value.

If you finance the purchase, you could end up owing more than the car is worth.. especially if you have a long loan term.

How to avoid depreciation?

Easy, buy a car in cash!

How can paying cash can help with depreciation?

If you already own the car, depreciation won’t hurt so much!

By already owning your car, you don’t have to worry about not being able to keep up with the car loan payments or needing to pay more than it’s worth.

4. The Vehicle is 100% Yours

I still remember receiving the car title letter saying I am the car owner. That was exciting, especially since I saved so hard to pay for it all in cash.

It feels very different when you drive a car without a loan. There’s no worry about monthly car payments. You don’t need to worry about car depreciation.

That’s the peace of mind that comes with buying a car with cash!

5. Prevents You From Overspending

Financing the purchase of a car will encourage you to spend more than you plan to because you will focus more on monthly payments rather than the car’s total price.

“Just because you can make the payments doesn’t mean you can afford it.”

Dave Ramsey

When planning to buy a car with cash, you have to buy it with the money you have on hand, so you will have to stick to your budget, and it will be easier to talk to sales representatives!

I bought my Toyota corolla from my brother-in-law. I remember he showed me some nicer cars, but I always said, “sorry, this is not in my budget.”

Buying a car with cash really can help prevent you from overspending.

6. Won’t Effect Your Debt-To-Income Ratio

A car loan will affect your DTI (debt-to-income) ratio and eligibility for other loans, such as a house mortgage.

Lenders want to ensure you have enough money left over to cover other living expenses and extra cash flows.

Most mortgage lenders generally approve someone — including their new mortgage payments — when their debt-to-income ratio falls to 43% or less.

When you have a car debt, your buying power will be lower (higher DTI) when looking at homes.

You’ll have more room for DTI to buy your dream house when you don’t have car debt.

Quick Recap:

Avoid Interest

No Monthly Payments

Depreciation Doesn’t Matter

The Vehicle is 100% Yours

Prevents You From Overspending

Won’t Effect Your Debt-To-Income Ratio

Throughout my life, the Land Rover Defender model has always been my dream car.

My motivation is knowing that one day I will buy a brand new Land Rover with all cash.

I believe it will happen, and I will work hard to make that dream come true, including saving and investing to make it happen!

Others may think you’re crazy for not getting a car loan or driving an older vehicle, but it will be worth it in the end!

What are some of your positive experiences buying a car with cash? Please let us know in the comments section below!!

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links, please see our disclaimer for details.

Before jumping into the debt snowball method and how it works, I’d like to share a quick statistic regarding the average amount of debt in the United States.

According to business insider, the average American has $52,940 worth of debt across mortgage loans, home equity lines of credit, auto loans, credit card debt, student loan debt, and other debts like personal loans!

YouTube video sharing how I paid of $56,000 in student loans

If you are one of countless Americans who want to know how to repay debts, you may have heard of a lot of different methods of repaying debts.

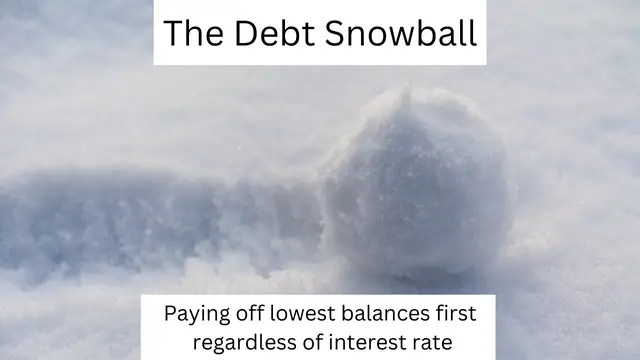

One such method is the debt snowball method!

The debt snowball method has helped us stay on track when paying off debt and is the method we used to pay off $56,000 in student loans.

Using the debt snowball made us very excited and stay motivated when paying down our student loans. I remember how my smallest student loan was only $800. We were able to pay it off quickly. It felt GREAT!!

We really could not express our excitement in words when we saw the balance for that small loan become zero!!

That excitement gave us the motivation to keep going. To make all the remaining loan balances become ZERO.

If you are reading our article, you must wonder how to pay off your debt. Let me introduce you to your best new friend: the debt snowball method!

What is the Debt SnowballMethod?

The debt snowball is one method to pay off debts in a specific way. You just need to arrange and pay off your debts from smallest to largest, ignoring the interest rate. Doing so builds momentum or a snowball effect that helps keep you going.

Imagine a snowball rolling down a mountain. At first, it was very small. As it continues to roll, the snow layers increase.

Each time you add a layer, the snowball gets bigger and bigger. This helps the snowball gain a lot of momentum.

By the time the snowball had reached the foot of the mountain, it had grown to the size of a boulder!

How Does the Debt Snowball Work? Step-By-Step

Step 1: List your debt amounts (except mortgages) from smallest to largest, regardless of interest rate.

Step 2: Continue making the minimum payment on all debts except for the smallest debt amount.

Step 3: Pay off as MUCH of your smallest debt as FAST as possible.

Step 4: Repeat steps 1 through 3 until all debts are paid off in full!

Here are more details for each of the steps:

Step 1: List your debts (Except your mortgages), from smallest to largest, regardless of interest rate.

Write down every outstanding debt you have (except for the mortgage). This may include credit cards, student loans, medical bills, car loans, and any other types of debt you have broken out from smallest amount to largest.

Write down the minimum monthly payment, monthly due date, etc., just to keep everything on track.

Step 2: Make a minimum payment for all debts except the smallest debt.

Keep paying the minimum monthly payment for all debts. The payment history will affect your total credit score.

Therefore, the more you pay on time, the fewer the late fees. Doing this will increase your credit score!

Having an excellent credit score is so important. We ended up not getting the best interest rate for our second property due to having a bad credit score which was sad.

The positive thing is that we learned a valuable lesson and became more careful of our credit and monitoring our credit scores.

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

Step 3: Repay as much of your smallest debt as possible.

After making a minimum payment on all debts accounts, put any remaining money into the smallest debt (loan) until the smallest debt is paid off. Then move on to the next smallest debt.

Step 4: Repeat steps until all debts you have paid off all debts in full.

Continue to put all extra cash into the smallest outstanding debt until it is paid off in full.

You can then focus your efforts on paying off the next smallest debt. Do this until all debts are fully paid off!

Why we used the debt snowball

“Focusing on paying down the account with the smallest balance tends to have the most powerful effect on people’s sense of progress – and therefore their motivation to continue paying down their debts.”

In the beginning, like many people out there, I didn’t know that student loans were bad and never thought I could graduate student debt-free.

People I knew would congratulate me on successfully receiving a student loan for any given semester. When we purchased our first townhome, I still recall how I was required to give our lender a future monthly student payback plan (once I graduated).

My income was lower then, so the monthly payment plan was about $30 a month going off an income-driven payment plan. I thought to myself, “oh!? student loans aren’t too bad.

I only need to pay back $30 a month after I graduate!” but when we purchased our second property, I had a better job with a higher income.

At that moment, I was shocked to see how much I needed to pay every month after graduating on an income-driven plan.

The number went up like crazy! That was the first time I realized student loans are not good.

If interested, please contact your student loan provider to see your payment plan when your income increases. Then you will know what I am talking about.

Thank goodness my wife found out about the amazing Dave Ramsey. Even now, we are still very grateful for Dave Ramsey’s teachings on personal finance and getting out of debt, he helped change our lives!

My wifey listened to him tons at first and then would tell me, “Hey baby, let’s save up for your MBA tuition by ourselves and pay down your bachelor’s student loans”!

My wife received a full scholarship, and her parents also helped her with other expenses before we got married. I had accumulated $25,000 in student debt from my bachelor’s degree. My MBA was a remote/online program with six semesters; the total tuition was $31,000.

That means we needed to pay off $56,000 once I graduated!

While saving and paying for my MBA tuition, I still needed to pay off the student loans left from my bachelor’s degree. We used the debt snow method to get it done.

First, we listed all the balances and then paid them off from small to big, ignoring the interest rate. Using this method gave us much motivation and a positive feeling whenever we paid a loan balance off!

Later, the COVID student loan relief plan went into effect, and the interest rate became zero during a specific period. We were able to save a lot on interest from this relief plan.

From the point of view of mathematics and numbers, Snowball’s debt won’t let you save the most because of varying interest rates.

The point is to change behavior and encourage/motivate us to pay our debts faster with more motivation in the long run.

“Winning at money is 80 percent behavior and 20 percent head knowledge. What to do isn’t the problem; doing it is. Most of us know what to do, but we just don’t do it. If I can control the guy in the mirror, I can be skinny and rich.”

Dave Ramsey

Everyone’s financial situation is different. Please consider other debt repayment strategies until you find one that suits you best. For us, the debt snowball worked great!

Remember, many methods and strategies help you pay off your debts. We all are in unique financial situations and may have different types of debt, and we hope you can find a method or a combination of methods that works best for you.

Although we did not need to refinance student loans, it can be an option that can save you potentially thousands of dollars over the life of a loan.

If you need to refinance student loans, we highly recommend using LendKey.

They offer low-rate and low-cost student loan refinancing. Additionally, your credit score will not be impacted when exploring rates.

Has the debt snowball method been effective for you? What are some other strategies you’ve enjoyed to pay off debt?

Please leave a comment below and let us know!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Getting out of debt and knowing how to deal with debt collectors is essential to gaining control over your finances. This article aims to help you successfully negotiate and deal with debt collectors.

Did you know that every 1 out of 3 US adults has a debt collection account(s)?

In this article, I share our story dealing with debt collectors including 4 tips to help you when dealing with debt collectors.

This post may contain affiliate links; please see our disclaimer for details.

My collection account came as a big surprise, it was from past college tuition that was never paid off.

I transferred to a new college in Hawaii and thought I had successfully received the student loan for the semester.

Turns out I was wrong.

One document needed to be signed before the tuition/loan could be dispersed, but I completely missed it.

Since the document wasn’t signed, I never received the student loan. Unfortunately, the entire amount was sent to collections.

After one semester of school in Hawaii, I transferred back to my school in Utah. One year later, I started getting calls from a debt collector.

They told me that I had a collection account because I didn’t pay my tuition.

Both my wife and I didn’t believe it at all and thought it was a scam at first. We thought there was no way I didn’t pay my tuition, so we just ignored it.

Our Story Continued…

We discovered the collection account was real when applying for our second property loan. It turns out it was not a scam, hurting my credit score!

Fortunately, my wife’s credit score was still excellent, so our combined score wasn’t too bad. My wife’s credit score was terrific. Together our score was still around 700.

Unfortunately, we could still not get the best interest rate for our second property loan. The interest rate on the mortgage ended up being almost 5%, ouch!

We learned a valuable lesson and became much more aware and careful of our credit scores.

We started saving like crazy after we closed on the loan. Our total debt collection account was $6,000, but we successfully negotiated with the debt collector.

For the final settlement, we only needed to pay $3,500 in total as a one-time payment. After paying, the collection account would be removed entirely from our credit history.

Our credit score shot up a lot after that, YES!

Now let’s look at the reasons for how we successfully dealt with debt collectors.

How to Successfully Deal with Debt Collectors

1. Verify Your Debt, Avoid Scams!

First, you must ensure the collection account is yours, including all information regarding the debt. There are real scammers out there trying to collect personal information.

Don’t give away your trust or your personally identifiable information too easily. Remember it is best to be careful.

We requested the debt collector send us everything in writing through the mail. We also called my school in Hawaii to verify the debt account was real.

Don’t just negotiate regarding your monthly payments or lower your total debt. Request they remove the collection account from your credit account/history.

Removing the lousy credit account from your credit score sooner will be well worth it.

After finding out the total collection amount was around $6000, we calculated our monthly budget to see how much we could afford for a monthly payment.

We worked hard to save up a big lump sum of money to pay off the account with a one-time payment, even though it was less than the collector was asking for.

We talked with the debt collector, and they agreed on a very minimal amount for the monthly payment plan.

You can always explain your financial situation to the debt collectors. It’s okay to say you don’t have much money or cash flow and propose the only amount that works for you.

Saving Up Money & Negotiating to Pay Off With One Lump Sum

After that phone call, we worked our butts off and saved $3,500!

We felt we could try to negotiate again with the debt collectors by proposing to pay off all debt with a lump sum of money.

We didn’t think our negotiations would be successful because it was almost half of our original collection amount, from $6,000 to $3,500. It never hurts to try!

We called our debt collector and discussed what was possible if we made a one-time payment. Next, we requested debt account be removed from my credit report.

The debt collector listened as we explained we didn’t have a lot of money and worked our butts off to save this $3,500. Having him agree to a one-time payment would help us a lot.

We also told him how the collection account happened and how we didn’t know if the collection account typically takes full responsibility for our bills.

As mentioned at the beginning of this post, it just happened by mistake.

The debt collectors told us he needed to talk with our original debt owner, my school back in Hawaii.

We told him to please tell my school our situation. We emphasized it would be a big blessing for our young family if they agreed to our plan.

Luckily just a few days later, we received a miracle call from the debt collector who told us my college agreed with the $3,500 settlement PLUS the collection account could be removed from my credit history!

We feel this is such a massive blessing that everything worked out great.

4. Have Everything In Writing.

After receiving the news of being able to make a one-time payment and have the account removed from our credit, we requested a settlement agreement showing we paid the total collection amount in full and that it would be removed from my credit history.

After the debt collector agreed to send over everything in writing, we made the one-time $3,500 payment.

My credit score shot up a few months later, and the collection account was gone!

In Conclusion

Life is a journey of learning lessons, and we have learned a lot about dealing with debt collectors. It’s important to learn quickly from mistakes and face life with an optimistic viewpoint.

Paraphrasing what Kevin Hart has said –

“It’s okay to make mistakes, we just need to learn how to fail better each time”

Due to this experience dealing with debt collectors, we have become more concerned about our credit scores.

Including more frequently checking our email and mail to see if there are any unpaid bills.

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you read How We Became Landlord At Age 22 As College Student, you will see that had a high and scary interest rate for our 2nd property/condo. The reason for this was that I had some surprising credit issues.

When COVID-19 happened, interest rates dropped significantly. Many people started to buy real estate and/or refinance their homes.

We noticed these fantastic interest rates and decided to refinance our condo! (We were also fortunate to buy and build our third property during the low-interest rate time).

Compelling advantages/reasons to refinance your home

Lower interest rate.

Pay off the home mortgage faster.

Get rid of home mortgage insurance (PMI).

Lower monthly payment.

Can take cash out to pay off high-interest debt, use for a new property down payment, etc.

Pay off loan faster (IE – change from a 30-year to 15-year term).

Switch from an adjustable mortgage rate to a fixed rate.

We chose to refinance primarily to obtain a lower interest rate, lower monthly payment, and wipe out mortgage insurance. We did not pull any cash out for our refinance.

I would like to share our refinance experience for our second property/condo. Side note: we refinanced while still living there, so it was our primary residence.

Our refinance process was easy! We shopped around and found three different lenders to give us a quote. Next, we would review and go with the best quote.

We highly recommend finding at least three different lenders to compare and negotiate with to get the best deal. One of the lenders told us, “ I would be willing to cut my commission to give you the best deal.”

After choosing the one we liked best, we started submitting documents. Below are the most common required documents when applying for a home loan or refinance.

Most common documents required for underwriting:

2-year tax returns

Pay stubs, W-2s, or other proof of income

Bank statements and other assets

All of your debt monthly payment history

Credit score, credit history

Gift letters (if someone helps you with down payment etc.)

Photo ID, SSN

Rent history if you are renting, mortgage/HOA history if you are a house owner

House insurance company if you have a preference, usually it will cheaper when you bundle with car insurance.

If you have tenants, include rent payment history & current lease agreement.

Back to our refinance process, the lender next sent out an appraiser to check our property and give an estimated value based on house conditions and the market.

Because the value of the home increased, we could avoid mortgage insurance when refinancing by having 20% equity in our condo.

We could have pulled out equity but decided to leave it all in there. Our mortgage insurance, or PMI, went from around 100 dollars to 0 dollars a month!

The interest rate dropped from around 5% to 3%, down 2%! Our monthly mortgage payment used to be approximately $1200 but went down to around $1000 (with HOA fees), saving us around $200 a month!

We paid nothing at closing. The refinance closing costs were added to our loan, and our total loan amount became about $161,000.

In Conclusion

Below is a chart to sum up our refinance experience with numbers.

Before Refinance

After Refinance

PMI

$100

$0

Interest Rate

5%

3%

Total Monthly Payment (with HOA)

$1,200

$1,000

Before and after refinancing our condo

We felt so blessed after finishing the refinancing process and know it will be worth it in the long run. Our next step was purchasing our third property and renting out our condo.

We leased it out for $1,300, giving us around $300 monthly in cash flow! Having that type of investment property has been an enormous blessing.

We hope that our refinance story can help you better understand the process a little better and the benefits that can arise by doing a refinance.

Feel free to share other benefits or stories you have doing a refinance in the comment box below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

The Squid Game TV show has recently become the number one television show on Netflix in over 90 countries! The hype made its way to us, and we ended up watching the entire series. While watching Squid Game, we realized there are many important lessons to be learned on personal finance.

This post may contain affiliate links; please see our disclaimer for details.

As for a rough summary of the TV show, a secret group of rich people invited 456 people to participate in a series of six deadly games.

Those selected had serious money problems and many other issues. The main character was in massive debt and could have used some personal finance wisdom!

Although the Squid Game story is fiction, we can all learn valuable lessons regarding debt and personal finance.

So let’s jump in!

YouTube Video Sharing The 6 Financial Lessons Learned from Squid Game

Here are the six key takeaways we would like to share with each of you.

Because when the next recession or stock market crash hits, there will be enough money in the emergency fund so that no money needs to be taken out of retirement investment accounts.

Instead, you will be able to wait until the stock market recovers. 🙂

My wife and I started our Emergency Fund and put it into a high-yield savings account to give us more peace of mind.

We recommend not putting your emergency fund into a high-yield savings account and NOT into the stock market since you will need quick access to the money.

A great place to get started with your savings account isCIT Bank. They offer very competitive saving rates with no monthly maintenance fees.

With their Saving Connect Account, you can earn 12x the national average! There are no ATM fees, and you have the convenience of online banking.

“ Every time you borrow money, you’re robbing your future self” –

Nathan Morris

An important financial lesson from the Squid Game show is to stay away from bad debt! Which to us means debt doesn’t make you money, don’t hold onto it.

We can proudly say: We are completely debt-free except for the mortgage. We feel the freedom! It’s so good for our mental health and relationship!

We are not trying to boast but want to share our process and hope everyone can feel the freedom that comes from becoming debt-free.

3. Live the Budget Life (it’s worth it)

Buying things in cash is worth it, even though it takes patience and time to save up the needed cash.

Make sure to know if the thing you are thinking about buying is truly a ‘need’ or just a ‘want’. Give yourself time to think it over or cool down before purchasing.

It’s also okay to use a credit card, but make sure to pay it off immediately.

Instead of eating out a lot, my wife and I would cook at home. We would meal plan for the week and put any leftovers in the freezer. Doing this is convenient, especially when you’re constantly on the go.

We buy a lot of things second-hand and save a lot of money by not buying something brand new.

There are many free things through the Facebook marketplace, such as baby items, household items, etc.!

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

4. Have Health Insurance

In the squid game series, the main character made a huge mistake- he canceled his mom’s health insurance plan. In the USA, hospital bills can be very expensive.

If we didn’t have health insurance, then the delivery cost for our baby would have been $12,000 out of pocket. If there would have been complications or other issues, then that bill would have been higher.

Health insurance is a big blessing for us; we cannot imagine without it!

5. Invest Smart, Avoid Gambling

In one of the Squid Game episodes, one guy taught the lesson to “don’t put all your eggs in one basket.” We agree! We need to invest more and invest more wisely.

Regarding funds, we love the Total Market Fund and S&P 500 fund. If you don’t know what to invest in, they both can be a good starting point!

Gambling can become a scary addiction. We know recently how cryptocurrency, Game Stop stock, and other things have been crazy.

For us, it is more like gambling. Someone with much extra money could invest in these things but must be willing to lose it all.

90% of our stock market investments are in a regular mutual fund, index fund, or ETF. 9% of our investments are in single stocks. Less than 1% is in cryptocurrency.

6. Spend Quality Time With Your Family.

We know how life can get busy. We need to work and make money for family needs. No matter how busy life gets, it’s important to remember FAMILY TIME.

Time needs to be spent building important relationships with family.

We enjoy going on dates and spending time with our little kiddo away from work and distractions. Relationships are the spice of life!

When I was doing work and school full time, my schedule was pretty crazy, but I always did my homework after my baby was sleeping because I wanted to help my wife and spend time with our baby.

I don’t want to miss any special moments of fatherhood and raising a kid.

For a recap, below are six finance and life lessons we took away from the squid game series.

Save up an emergency fund

Get off of debt fast

Live the budget life

Have health insurance

Invest smart: avoid gambling (don’t put one egg in one basket)

Spend quality time with your family

Thanks for reading! We’d love to hear your thoughts on the tv series and personal finance lessons; drop a comment below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links, please see our disclaimer for details.

In this article, I will share how we came to realize student loan debt is the best thing to have. Then I will introduce the 11 money tips that helped accelerate our debt-payoff process and allowed me to become student debt free by graduation! In total we paid off $56,000 in student loans.

The Realization

Back in the day, my wife Shan and I didin’t think student loans were a bad thing. The thought of graduating zero debt in student loans had never crossed my mind.

When purchasing our first townhome, I had to give our lender my student loan payback plan. This is the amount I would owe each month upon graduation.

At that time I had a much lower income. The monthly payment plan was only $30 going off an income-driven payment plan. I thought to myself, wow! Having student loans isn’t too bad because the monthly payments after graduation are so low.

I would only need to pay $30 a month after I graduate! But when we purchased our second property I had a better job with a higher income.

At that point, we needed to provide another income-driven payment plan to our lender. I was shocked to see how much I needed to pay every month. The monthly payment amount shot up like crazy!

I realized student loans were not the best thing to have.

Thankfully we found Dave Ramsey and agree with many of his money tips. Even now, we are still very grateful for Dave Ramsey’s teachings on personal finance and getting out of debt. His teachings helped spark our change toward our finances.

At first, it was Shan who listened to him who would tell me, “let’s save up for your MBA tuition by ourselves and pay down your bachelor’s student loans”!

“The average total student debt continues to teeter around $30,000”

US News

She received a full scholarship, and her parents also helped her with other expenses before we got married.

Me, on the other hand… I had accumulated $25,000 in student debt from my bachelor’s degree.

My MBA program was remote/online with six semesters, and the total tuition for the program was $31,000.

So, we needed to pay off $56,000 once I graduated!

It was time to change and start paying off my student loans EARLY! Let me introduce how I graduated debt-free and after becoming a new father and still being a college student.

My graduation ceremony at Utah Valley University (UVU)

1. Mint Mobile: monthly phone plans at AMAZING prices

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

2. Budgeted life and Raise

We wouldn’t eat out a lot but instead would cook at home. We would frequently make a lot of food, divvy it up into lunch boxes, then put it in the freezer.

Doing this was so convenient, especially when constantly on the go. You can just warm it up in the microwave when needed.

We decided to buy a lot of things second-hand, don’t buy brand new!

There are many free things through the Facebook marketplace, such as our baby’s toys, stroller, etc.!

We are big fans of Raise where you can buy gift cards at a discount for places like Walmart.

3. Rent out our extra room

Before having our first baby, we would always rent out our extra room to friends or family members.

We personally didn’t want to share the place with someone we didn’t know so we typically stuck to people we knew.

Giving them a good deal was important to us, so it turned out to be a nice win-win situation.

4. Sold a lot of stuff (minimalize)

We watched minimalism videos which were very intriguing to us and gave us the motivation to sell items we didn’t need.

To help us know what we don’t need, we would ask ourselves, “does this item really add value to my life?”.

I even sold my PS4 and Nintendo Switch because I was simply too busy with my full-time job and full-time school.

I wanted to spend any extra time doing more meaningful activities (such as learning about investing!).

We love pets! Whenever our friends would ask us to help watch their pets, we were more than willing to do so.

My wife is from China, so she knew a lot of international students who didn’t have family here. They needed people to watch their pets when they traveled or went back to China.

Since we love animals, this was an easy side hustle.

For us, this was not a job at all; we both enjoyed playing with each pet (by the way, we would only watch fully trained pets, so it wouldn’t be hard to take care of them).

We like using the pet sitting site/app called Rover where you can get paid to help watch other people’s pets!

Regardless of what you do, finding a side hustle is a great idea to add some extra cash to help pay off student debt.

6. Donating Plasma

I heard about donating plasma from my brother and started donating it.

You can probably make around $400 a month, sometimes even more, when there is a promotion going on! Depending on the place, each donation will take around one hour total and you can donate up to twice in one week.

It was so easy, I just had to lie down there and could read a book or play on the phone.

I still donate plasma sometimes when they have a good promotion, but now the money I get is my “freedom/fun money” lol.

7. Find a higher-paying job

I always worked full time while going to school full time. During my time at college, I moved up the ranks to a supervisor position when I first got married. Then to an account manager during the last year of my bachelor’s program. I then became a product development specialist after the first semester of my MBA.

Each position change gave me around a $15,000 salary increase. In total, I had around a $30,000 salary increase during school! I would quickly move to another position once I became comfortable with my job responsibilities and look for opportunities to expand my knowledge and skills.

8. Employer tuition reimbursement.

The company I work at as a product development specialist is amazing. They offered me $3000 each year of tuition reimbursement.

For my two years of studying for my MBA, I received a total amount of $6000 for tuition reimbursement.

This is a great benefit that helped us pay off debt faster.

9. Other student financial aid

After getting married, I received some grants! So I didn’t pay any tuition for the remainder of my bachelor’s degree.

We highly recommend looking and applying for scholarships or financial aid rewards.

While we were saving and paying for my MBA tuition, I still needed to pay off the student loans left from my bachelor’s degree. We used the debt snow method to get it.

First, we listed out all the balances and then paid them off from small to big, ignoring the interest rate. Using this method gave us so much motivation and a very positive feeling whenever we paid a loan balance off!

Then what happened later was the COVID student loan relief plan, where the interest rate became zero during a certain time period. We were able to save a lot on interest from that relief plan.

Due to Covid in 2020, the interest rate became so low resulting in a boom in the housing market.

It was a hard decision to sell our first rental property because we want to keep it long-term.

After thinking long and hard, we both feel peaceful about selling it. Around the last year of MBA, we sold our first property. I used part of the profit to pay off the rest of the student loans we owed.

It was an amazing feeling to be able to use cash to pay off the rest of my MBA tuition.

We became 100% debt-free except for the mortgage after that!

12. Bonus Tip: Refinance Student Loans

Although we did not need to refinance student loans, it can be an option that can save you potentially thousands of dollars over the life of a loan.

If you need to refinance student loans, we highly recommend using LendKey.

They offer low-rate and low-cost student loan refinancing. Additionally, your credit score will not be impacted when exploring rates.

Although the journey was not the path of least resistance, it was the biggest relief for us to pay off all student loans. The feeling is amazing and free!

No pain, no gain! We really like what Dave Ramsey has said, “live like no one else, and then live like no one else”! Below is a recap of the 11 steps:

Screenshot of my Navient Loans all paid off with zero balances!

The average monthly student debt payment in the USA is around $400 a month. If you instead invest $400 a month in a reliable fund (like S&P 500) with average an average return of 12%, you will have around $92,000 in 10 years and ONE MILLION in 28 years!

We are so grateful that I could graduate student debt-free with both my bachelor’s and master’s degrees.

I know someone who wanted to buy a house but couldn’t qualify because of their huge student loan debt and needed to pay down the loan balances first.

The housing prices went up a lot when they finally qualified for a house loan. It was so sad! We hope our experiences and tips can help each one of you!

You will not regret starting now. Take the time to create the best method for you to pay off student loans early; you won’t regret it!

What other ways have you used or have thought of paying off student debt early?

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.