It can be tough to know where to start if you’re trying to decide whether a Roth 401(k) or Traditional 401(k) is right for you.

According to RetireWire.com, “There’s 5.4 trillion dollars in IRA’s Assets in IRA’s have grown 10% per year. Nearly 49 million households have a traditional IRA”.

You can see great potential for return, especially in the long run.

Both the Roth 401(k) and the Traditional 401(k) have their pros and cons, and it cannot be easy to figure out the best option for your specific situation.

This post may contain affiliate links; please see our disclaimer for details.

If you prefer to watch my video instead, you can check out my YouTube video!

What is a Roth 401(k)?

A Roth 401(k) is a retirement savings account that offers tax-free growth and tax-free withdrawals in retirement.

Roth 401(k)s are funded with after-tax dollars, which means you won’t get a tax deduction for your contributions. However, all earnings and withdrawals are tax-free in retirement.

Roth 401(k)s are an excellent way to save for retirement, especially if you’re in a high tax bracket now and expect to be in a lower tax bracket in retirement.

They are also a good choice if you’re young and have many years to let your money grow tax-free.

However, Roth 401(k)s are not right for everyone. If you’re in a low tax bracket now and expect a higher tax bracket in retirement, you may be better off with a traditional 401(k).

With a traditional 401(k), you get a tax deduction for your contributions now, but you’ll pay taxes on your withdrawals in retirement.

What is a Traditional 401(K)?

A traditional 401(k) is a retirement savings account that offers tax-deferred growth and taxable withdrawals in retirement.

Traditional 401(k)s are funded with pre-tax dollars, which means you get a tax deduction for your contributions. However, all earnings and withdrawals are taxable in retirement.

With a traditional 401(k), you get a tax deduction for your contributions now, but you’ll pay taxes on your withdrawals in retirement.

When you are ready to retire, you may be in a higher tax bracket and owe more taxes on your withdrawals.

However, traditional 401(k)s may not be the best choice for everyone. If you’re in a high tax bracket now and expect a lower tax bracket in retirement, you may be better off with a Roth 401(k).

The main difference is that Roth 401Ks offer tax-free growth, while traditional 401Ks offer tax-deferred growth.

Tax-free growth: You will never have to pay taxes on the money you contribute or the earnings it generates.

Tax-deferred growth: You won’t have to pay taxes on the money you contribute or the earnings it generates until you withdraw it from your account.

The Roth 401K is unique because it allows you to contribute after-tax dollars to your retirement account. This means that when you retire and begin taking distributions, you won’t have to pay any taxes on the money you withdraw.

A traditional 401K, on the other hand, uses pre-tax dollars. This means you will be taxed on the money you withdraw from your account when you retire.

Should You Choose A Roth 401(K) or a Traditional 401(K)?

The Roth 401(k) was created in 2006 as an addition to the traditional 401(k). Both types of accounts are employer-sponsored retirement savings plans that offer tax advantages.

So, which is better for you? Roth or traditional?

Questions to First Ask Yourself:

When do you plan on retiring?

What is your tax rate now?

What do you think your tax rate will be in retirement?

How much money do you think you will need in retirement?

What is your investment strategy?

Are you comfortable with the idea of having your money invested for the long term?

The Roth 401(k) offers more flexibility and tax-free growth, while the traditional 401(k) offers tax-deferred growth.

Consider your retirement goals, tax situation, and investment strategy when deciding between a Roth 401(k) and a traditional 401(k).

What are Roth 401(k) and Traditional 401(k) Contribution Limits for 2022?

These two accounts share the same contribution limits for 2022 at $20,500.

Can I contribute to both a Roth 401(k) and a Traditional 401(k)?

Yes, you can contribute to a Roth 401(k) and a traditional 401(k), but your total contributions cannot exceed the $20,500 limit.

For example, if you’ve already contributed $10,000 to your Roth 401(K) this year, you can only contribute an additional $10,500 to your traditional 401(K).

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

Choosing between the two options depends on your circumstances. If you think you will be in a higher tax bracket in retirement, then a Roth 401(k) can offer significant tax savings.

If you are young and just starting your career, you may be in a lower tax bracket now than when you retire. The traditional 401(k) can offer significant tax savings.

Deciding Based On Your Tax Bracket: Roth 401(k)s offer tax-free growth and tax-free withdrawals in retirement, which can result in significant savings over the traditional 401(k).

Talk to a financial advisor if you’re unsure which is right for you. They can help you determine the best option for your unique circumstances.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Ever wonder if you should get a 15-year or a 30-year mortgage? Many homeowners and homebuyers are asking themselves that exact question.

Both options have pros and cons, but which one should you choose to get the best deal?

In this article, we will break down 15 vs. 30 years mortgages so that you can make a more informed decision!

This post may contain affiliate links; please see our disclaimer for details.

Before diving into the details of 15-year and 30-year mortgages, let’s first define what fixed rate means. Understanding this is the most important factor to consider when making your decision.

Fixed-Rate

With a fixed-rate mortgage, the interest rate and monthly payment stay the same for the entire duration of the loan.

In contrast, there is the variable or adjustable-rate mortgage (ARM), which has an interest rate that can change over time.

For most people, a fixed-rate mortgage is preferable. It provides stability and peace of mind knowing that your monthly payments will never increase.

Budgeting is easier since you’ll always know exactly how much you need to set aside each month.

Now that we’ve covered what fixed rate means, let’s get into the 15 vs. 30 years mortgage debate!

Simply put, a 15-year mortgage is a loan that matures in 15 years.

The interest rate on a 15-year mortgage is usually lower than that of a 30-year mortgage. The payments, however, are higher.

With the shorter term, a 15-year mortgage will be paid off sooner. Less interest will need to be paid over the life of the loan.

This can be advantageous if you want to own your home free and clear and if you plan to move within the next few years.

What is a 30-year mortgage?

A 30-year mortgage is a loan that matures in 30 years.

The interest rate on a 30-year mortgage is usually higher than that of a 15-year mortgage, but the monthly payments are lower.

Since the 30-year mortgage has a longer term, you will pay more interest over the life of the loan.

However, your monthly payments will be more affordable, which can be helpful if you’re on a tight budget.

Now you know the basics of 15 vs. 30 years mortgages. It’s now time to decide which is right for you!

Want lower monthly payments: go with a 30-year mortgage.

Own your home free and clear faster: go with a 15-year mortgage.

If you stay in your home for longer: opt for a 30-year mortgage. Doing so can help your monthly payments be more manageable.

To help you decide, we will review the math of 15 vs. 30 years mortgages. You’ll also see the difference in interest paid over time.

15-year vs. 30-year mortgage comparison

So what does the math say?

With a fixed-rate mortgage, the interest rate and monthly payment stay the same for the entire duration of the loan.

First, let’s assume a 20% down payment of $40,000.

15-year mortgage: ($200,000) at an interest rate of 3.4%

30-year mortgage: ($200,000) at an interest rate of 4.1%

With a 30-year mortgage, you’ll end up paying $73,848 more in interest over the life of the loan. But, your monthly payments will be lower at $773 rather than $1,136 with a 15-year mortgage.

With a 15-year mortgage, you will be debt-free on your house 15 years earlier. On the flip side, you will have $363 less per month.

30-year mortgage: lower monthly payment, higher total interest paid, stay in debt longer.

What can you do to make both options more favorable?

You can increase the downpayment above 20%. Let’s see what the math would look like if we double the down payment to 40% at $80,000

15-year mortgage: ($200,000) at an interest rate of 3.4%

30-year mortgage: ($200,000) at an interest rate of 4.1%

With a 30-year mortgage, you’ll end up paying $55,386 more in interest over the life of the loan. But, your monthly payments will be lower at $580 compared to $852 with a 15-year mortgage.

With a 15-year mortgage, you will be debt-free on your house 15 years earlier. You will have $272 less to spend per month though.

So, 15 years vs. 30 years… which one should you choose?

As you can see, there are pros and cons to both 15-year and 30-year mortgages.

The best way to decide is to look at your current financial situation. Ask yourself what makes the most sense for you.

Now that you know the math comparing the two options let’s break down the pros and cons of each mortgage decision.

We will also show you if you are ready to consider a 15-year or 30-year mortgage.

When to consider a 15-year mortgage?

There are a few key things to consider when thinking about whether a 15-year mortgage is right for you:

Your current financial situation: A 15-year mortgage may be a good option if you can afford higher monthly payments.

You’ll also need to have the extra cash on hand for a larger down payment. The 15-year mortgages typically require at least 20% down.

Your long-term goals: If you’re planning on staying in your home for more than 15 years or if you plan to sell within the next few years, a 15-year mortgage may not make sense.

On the other hand, if you’re looking to retire sooner or if you think there’s a chance you may move in the next few years, a 15-year mortgage could be a good option.

Your interest rate: This is a big one! If you can get a lower interest rate on a 15-year mortgage than on a 30-year mortgage, it may make sense to go with the 15-year option.

You’ll want to compare rates from multiple lenders to ensure you’re getting the best deal possible.

Remember that 15-year mortgage rates are typically 0.50% to 0.75% lower than 30-year mortgage rates.

15-Year Mortgage Pros

You’ll save money on interest over the life of the loan

You’ll own your home free and clear sooner

Your monthly payments will be higher

15-Year Mortgage Cons

Your monthly payments will be higher, which could be a strain on your budget

If you need to sell your home before the 15 years is up, you may not recoup all of the money you’ve put into it (since you would have paid less interest overall)

30-Year Mortgage Pros

Your monthly payments will be lower, which can help with cash flow on a tight budget.

You’ll pay more in interest over the life of the loan, but it will be more manageable.

If you need to sell your home before the 30 years is up, you may recoup more of the money you’ve put into it (since you would have paid more interest overall)

You’ll have more flexibility in making extra payments or taking a break from payments if needed.

30-Year Mortgage Cons

You’ll pay more interest over the life of the loan

It will take longer to own your home free and clear

Use this information to weigh your options and decide which type of mortgage is right for you. Remember, there is no wrong answer – it depends on your unique circumstances.

Now let’s look at when you should consider a 30-year mortgage…

When to consider a 30-year mortgage?

There are also a few key things to consider when deciding if a 30-year mortgage is right for you:

Your current financial situation: If you can’t afford the higher monthly payments of a 15-year mortgage, a 30-year mortgage may be a better option.

Remember that even though your monthly payments will be lower, you’ll pay more in interest over time.

Your long-term goals: If you plan to stay in your home for longer than 15 years or if you think there’s a chance you may move within the next few years, a 30-year mortgage could make sense.

This gives you more flexibility than a 15-year mortgage and may save you money in the long run.

Your interest rate: Like with a 15-year mortgage, you’ll want to compare rates from multiple lenders to ensure you’re getting the best deal possible.

Remember that 30-year mortgage rates are typically 0.50% to 0.75% higher than 15-year.

15-year mortgages vs. 30-year mortgages – What’s The Difference?

The main difference between a 15 and a 30-year mortgage is the amount of time it will take to pay off your loan.

With a 15-year mortgage, you will pay less interest in the long run, but your monthly payments will be higher.

Conversely, a 30-year mortgage will have lower monthly payments, but you’ll end up paying more in interest over the life of the loan.

Which option is better depends on a few factors, such as how much money you have saved and your current interest rate.

If you can afford the higher monthly payments of a 15-year mortgage, it will save you a lot of money in the long run. However, if you’re not quite ready to commit to such a short loan term, a 30-year mortgage may be a better option.

If you’re unsure which mortgage is right, talk to your bank or financial advisor to get expert advice. They will be able to help you crunch the numbers and figure out what option makes the most sense for your unique situation.

Worst Case Scenarios

The chances of a worst-case scenario are rare. However, it is still helpful to know as many potential outcomes as possible.

These examples should not scare you from deciding but rather prepare and inform you.

Financial Difficulties: If you choose a 15-year mortgage and then experience financial difficulty halfway through the loan, you may have to sell your home or extend the loan term.

If you choose a 30-year mortgage and then experience financial difficulty halfway through the loan, you may be able to sell your home or refinance the loan to a 15-year mortgage.

This would provide some relief in terms of your monthly payments, but you would still be paying more interest over the life of the loan.

Job Loss: If you choose a 15-year mortgage and then experience job loss, you may have difficulty making your monthly payments

If you choose a 30-year mortgage and then experience job loss, you may be able to continue making your monthly payments for a while.

This will give you more time to find another job or come up with another source of income.

Death: If you die before the 15-year mortgage is paid off, your family will be responsible for making the remaining payments.

If you die before the 30-year mortgage is paid off, your family may be able to sell the house or refinance the loan to a 15-year mortgage.

This will depend on the housing market and their financial situation.

As you can see, there are real worst-case scenarios, and factoring these into your decision is important.

A mortgage is a big commitment, so understand all the risks and rewards involved before signing on the dotted line.

The Best Strategy For Improving The Outcome For Either Decision

By optimizing for these three factors below, you will improve the outcome of your 15 or 30-year mortgage.

If you can afford to put more money down, get a lower interest rate, and/or shorten the loan term, you will save even more money on your mortgage. Conversely, if you cannot afford to do any of those things, you may want to consider a 30-year mortgage.

Higher Down Payment: The more money you put down, the lower your total interest rate paid will be. Saving up and being patient can be offsetting.

However, if you are concerned about a tight monthly cash flow because of a high mortgage, you may consider paying more than 20%.

As you can see with the math we did together above; this will help lower your monthly mortgage expenses for both options.

You will also have some reassurance if you lose your full-time job sometime throughout the loan and can only come up with a part-time income.

A higher down payment can be seen as insurance for a loss of income that will make the monthly expenses less difficult to pay.

Lower The Interest Rates: It may be difficult to select your ideal interest rate for the loan. You can act when opportunities arise and are patient when rates are too high. Interest rates for mortgages can fluctuate between lenders and over time.

You want to get the best interest rate possible because this will directly impact your monthly mortgage payment, as well as the total amount of interest paid over the life of the loan.

Shorten The Loan Term: If you can afford it, you should try to shorten the loan term. This will result in higher monthly payments, but you will save money on the total interest paid over the life of the loan.

However, remember that you cannot always choose your loan term; it may be determined by the lender or based on how much money you can put down.

No matter which type of mortgage you choose, 15 years or 30 years, be sure to consider the following:

How much can you afford for a down payment?

What is the interest rate and how does it compare to other offers?

How long do you want the loan term to be?

Considering these things, you can make the best decision for your financial situation.

Optimizing for these three factors ensures you are getting the best possible deal on your 15 or 30-year mortgage.

You have more ways to improve your financial well-being beyond just the two options of the loan length when it comes to securing a mortgage.

Conclusion

Deciding on a mortgage is no easy decision. It can be daunting to commit to multiple decade-long financial obligations. But with this guide, you can make the best decision for your desires and circumstances.

Remember to consider your financial situation, long-term goals, and interest rate when deciding.

15-year mortgages and 30-year mortgages both have unique benefits and drawbacks, so take your time to weigh your options before you make a final decision.

If you’re looking for lower monthly payments, go with a 30-year mortgage. If you want to repay your loan sooner, go with a 15-year mortgage.

It all depends on your current financial situation and long-term goals.

When in doubt, talk to an expert! Your bank or financial advisor can help determine which mortgage is right for you.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

1) Use a Gas Credit Card

The first thing that comes to mind is using a gas credit card. This is easy, but using a gas credit card can be effective if used correctly.

Gas cards are commonly used for cashback or rewards on gasoline purchases, which can add up over time.

It can be an effective method for saving money at the pump, but it’s important to take the annual fees the credit card charges per year.

It is important to know that it is still a credit card, and you should use it responsibly.

If this would work for you, find a gas credit card with good benefits and no annual fee.

2) Choose The Best Priced Pump

Shoppers may save money on gasoline by comparing several options.

You can browse for the best prices online or take a mental note as you drive past various gas stations on your regular commute.

3) Take Advantage of Discounts and Coupons

It may not be glamorous to keep discount codes and coupons, but they are a simple and effective way of saving money on gas.

Gas stations frequently provide discounts and coupons, so use them while you can!

4) Become a loyal customer

Some gas stations have loyalty systems allowing you to earn points or savings on gasoline purchases.

It could be a great option if you often go to the same gas station or if that location is most commonly known for the cheapest price.

You can also ask the staff if they offer this if it’s not advertised.

5) Drive Less

It’s more difficult to avoid driving than it appears, but reducing your mileage may help you save money on gasoline.

If you can carpool, use public transportation, or walk or bike when possible, you will save money on gas.

In most cases, it will be hard to avoid driving, especially if you need to for work or to get essential items.

However, taking the long scenic route and night drive around town can be avoided if you are trying to save money on gas.

6) Plan your commute

If you can, try to schedule your journey so that you’re driving during off-peak hours.

Doing so will help you save money on gas and avoid traffic. Running the engine and idling will burn more gas.

You don’t want to be paying the high prices at the pump to watch your money evaporate with honks and horns behind you.

7) Plan Your Refills

By scheduling your weekly refuels, you can fill your tank faster than the increasing prices.

If you know that gasoline costs will rise, fill up your automobile before they do.

This can be minor in money savings, but it can make a significant difference when paired with other tips.

8) Check Your Caps For Leaks

Loose gas caps can cause evaporation and result in a waste of gasoline and money.

You can avoid losing gas and money by ensuring your vehicle is well-maintained and free of technical issues.

9) Let Go of Extra Weight

Every hundred pounds you eliminate from your car saves it three to four percent in gasoline usage.

You may have some items in your vehicle that are weighing it down. It’s beneficial to empty the car and get rid of anything you no longer need.

10) Slow and Steady

As mentioned earlier, unnecessary slow drives around town can be cut out. However, it’s important to know that quick accelerations also harm your wallet.

When possible, try to drive at a consistent pace, so you’re not wasting gasoline.

You can increase your fuel efficiency by as much as 80% for every five miles per hour you decrease your speed.

If you ease off the gas, you may save up to 30 cents per gallon.

Only speed things up in emergencies. Having this concept in mind on the road may also save you from speeding tickets and accidents.

11) Buy In Bulk

Some supermarkets sell gasoline at a discount. This can be commonly seen at wholesale stores like Costco and Sam’s Club.

They do, however, necessitate a yearly membership. If you shop there for your food, it might be useful to fill up the tank simultaneously.

Like stacking all fuel purchases on one credit card for the best cashback, a household can share one membership.

As a bonus, you can also use your gas credit card at these bulk discount stores.

12) Money-saving Apps

We mentioned earlier the benefits of finding the best prices in town.

A great way to do this would be to use apps like GasBuddy, Gas Guru, or AAA Mobile.

According to GasBuddy, purchasing the cheapest gas in town may save drivers up to 25 cents a gallon.

The apps are available for download on Android and iOS devices.

13) Time Your Tank Replacement

If you’re in the market for a new car, it might be beneficial to time your purchase when you need to replace your old car’s engine.

New engines are much more fuel-efficient, so you’ll save money on gas in the long run.

This is because the older the engine, the less efficient it becomes.

14) Get a Fuel-Efficient Vehicle

The second last tip for how to save money on gas is to get a fuel-efficient vehicle.

If you’re in the market for a new car, many fuel-efficient options are available.

You can also purchase a used car that is known to be fuel-efficient.

Hybrid cars are a great option because they use a combination of gasoline and electricity.

You can save money on gas while doing your part for the environment.

There are many fuel-efficient models to choose from, so take your time finding the perfect car.

16) Go Electric

Electric cars are becoming more popular, and technology is constantly improving. If you can switch to an electric car, you’ll be sure to save money on gasoline in the long run. Not only are they much cheaper to operate, but they’re also much better for the environment.

They are not cheap, but this is the best option if you’re looking for ways to save money on gas. Consider it as an investment that results in money savings month after month.

Electric or Hybrid?

When your car’s time ends, you might want to consider an electric or hybrid model. These cars have been shown to save drivers money on gasoline in the long term.

They also have the added benefit of being better for the environment.

Electric cars are powered by electricity and thus do not require gas. Hybrid cars have both an electric battery and a gas tank.

The battery is used first, and then the gas kicks in when the battery needs help.

While the initial cost of these vehicles may be higher, you will save money on gas in the long run. In some cases, you may even qualify for tax breaks or subsidies.

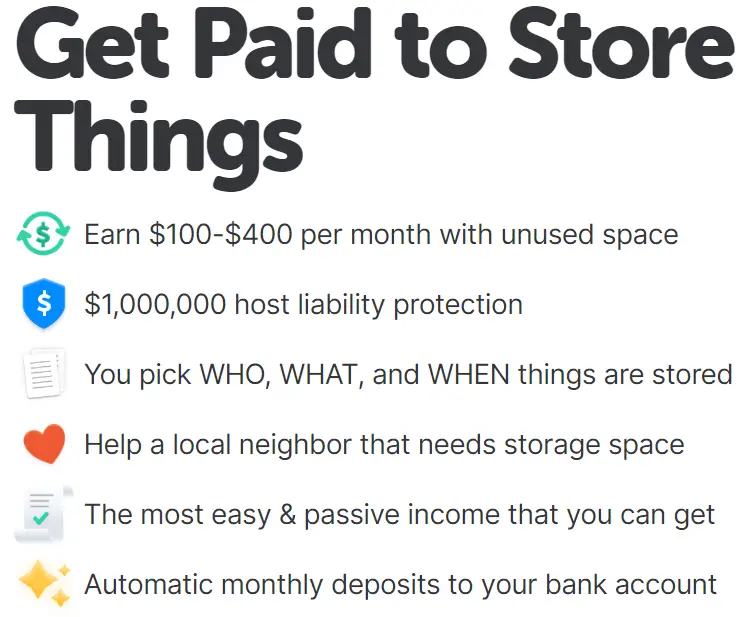

With the costs of gas continuing to increase, it’s not a bad idea to look at different ways to increase your passive income. This will give you more money at the end of the month to cover gas expenses.

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

Conclusion: Easy Ways to Save Money on Gas

Applying a combination of these 15 tips can help you save money on gas. Following these tips can ease the strain on your budget and pocketbook.

Some of these methods may not be realistic to your circumstance, such as buying a new fuel-efficient car.

However, there should be a few things mentioned in this article that you can do right now to start saving money on gas.

With the money saved, it can help keep your gas bill manageable while allowing you to save for a bigger purchase like an electric vehicle.

Use these tips and start saving money on gas today!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Do you want to retire early? The 4% rule is a common guideline that can help you achieve this goal.

The 4% rule states that you should withdraw no more than 4% of your retirement savings (nest egg) each year to ensure that it lasts throughout your retirement.

This article will explain the 4% rule in more detail and discuss some pros and cons of using this guideline.

This post may contain affiliate links; please see our disclaimer for details.

What Is The 4% Rule?

The 4% rule is a guideline that suggests that you withdraw no more than four percent of your portfolio value each year during retirement. The money you take out can go towards living expenses or other things, such as travel or gifts. The rule is meant to help ensure your retirement funds last without having to go back to work.

Some experts suggest using a slightly lower withdrawal rate, such as three percent or even two and a half percent, especially if you’re retired for 20 years or more.

Regardless of your withdrawal rate, it’s important to remember that the 4% rule is just a guideline.

It’s not set in stone, and there will be years when you may need to adjust your withdrawals up or down based on market conditions and circumstances.

This leads to the importance of having a 2-year emergency fund that can cover all expenses if there is a large drop in the market.

What is the Purpose of the 4% Rule?

Simply put, the purpose of the 4% rule is to help ensure that your money lasts throughout retirement.

This is especially important if you plan to retire for 20 years or longer.

The 4% rule is based on the work of William Bengen, a financial planner who wrote a paper in 1994 about safe withdrawal rates from retirement portfolios.

Bengen looked at historical data to see how different portfolio types and withdrawal rates would have fared over time.

He concluded that a portfolio consisting of 50% stocks and 50% bonds would have had a 95% chance of lasting 30 years if the investor withdrew no more than four percent per year.

How Does The 4% Rule Work?

The rule is simple:

You can only withdraw 4% of your retirement account per year.

If your retirement account is $100,000, you can withdraw $4000 per year.

Now you might be thinking, that’s not a lot of money. And you’re right, it’s not.

But the goal of the 4% rule is to make sure your money lasts throughout retirement, even if you live for 30 years or more.

The rule is based on the idea that your portfolio will grow over time and that the money you don’t withdraw will continue to grow and provide for you in retirement.

There are a few things to remember with the four percent rule.

First, it’s based on historical data and may not hold in the future.

Second, it’s a guideline, not a guarantee – you may need to save more or less depending on your individual circumstances.

For example, if you’d like a more comfortable retirement, you can set a goal of $1,000,000 in your retirement account. With the 4% rule, you could withdraw $40,000 per year!

Finally, it assumes that you will withdraw 4% of your savings each year in retirement, which may not be the case.

Despite these caveats, the 4% rule is a helpful way to estimate how much you need to save for retirement.

By following this rule, you can ensure that you are on track to reach your retirement savings goal.

Using The 4% Rule With An Investment Portfolio

To successfully use the 4% rule, it would need to be in an investment portfolio.

This is because the rule is based on the idea that your portfolio will grow over time, and you can withdraw four percent of the value each year without depleting your savings.

For example, if you’re 30 years away from retirement, the fund may be 90% stocks and just 10% bonds. But if you’re only five years away from retirement, it might be 50% stocks and 50% bonds.

This gradual shift helps to protect your savings while still allowing you to grow your money over time.

The most effective fund for the 4% rule is the S&P 500 Index Fund. On average, the S&P 500 grows at 11.5% per year.

Here is an example of calculating how much you’d need to retire comfortably using the 4% rule with the S&P 500.

The first step would be to decide how much income you’d need to live a financially free life.

The average cost of living for a U.S. citizen is approximately $1100 per month but let’s go with $2000 to be conservative and plan for a great retirement!

To receive a retirement income of $2000 per month ($24,000 per year), you’d need $600,000 invested into your S&P 500 account.

Now let’s see how long it would take to reach our goal of $600,000 using the historical growth rate of the S&P 500 at 11.5% annually.

$600,000 might seem like a lot, but with the power of compound interest and consistent monthly contributions, you can get there with just $121,000 as a total investment.

If you start with $1000 and invest $400 per month into an S&P 500 index fund, it would take 25 years to reach the goal of $600,000. But if you started investing at 25 years old, you could retire with an income of $24,000 at 55 years old!

If 25 years is too long, you can get there in only 15 years with monthly contributions of $1400. As you can see, there are many different variables that you can adjust to make the four percent rule work for you.

The Bottom Line: By calculating your desired income, you can find a retirement number that is comfortable for you.

The important thing to remember with the four percent rule is to start saving early and invest often!

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

What Are The Pros And Cons Of The Four Percent Rule?

There are pros and cons to using the four percent rule as a retirement guideline.

Some of the pros include:

It’s simple to understand and follow.

You can adjust your withdrawals up or down as needed based on market conditions and your circumstances.

It’s a helpful way to estimate how much you need to save for retirement.

It uses the stock market’s ability to grow to your advantage.

Some of the cons include:

It’s based on historical data and may not hold true in the future.

It’s a guideline, not a guarantee – you may need to save more or less depending on your circumstances.

It assumes that you will withdraw four percent of your savings each year in retirement, which may not be the case.

The large number needed can seem overwhelming.

Common Mistakes With The 4% Rule

Regarding retirement planning, the “four percent rule” is a guideline that’s often cited.

The rule of thumb goes like this: If you withdraw four percent of your nest egg each year during retirement, you’re unlikely to run out of money.

But as with any rule of thumb, there are exceptions – and the four percent rule is no exception.

People make several common mistakes when using the four percent rule. Here are eight of the most common:

Mistake #1 – Not Adjusting for Inflation: One mistake people often make with the four percent rule is not adjusting for inflation.

When you retire, your expenses will likely go up – not down. That’s why it’s important to factor in inflation when withdrawing money from your nest egg.

Mistake #2 – Not Taking Into Account Your Longevity: Another mistake people make is not considering their longevity.

Just because the average life expectancy is around 78 years doesn’t mean that’s how long you will live.

If you want to be safe, plan for a longer retirement.

Mistake #3 – Not Planning for Unexpected Expenses: People do not plan for unexpected expenses.

Retirement is often unpredictable, and you may need more money than you think.

Make sure to have a cushion in your nest egg so you can cover any unexpected costs that come up.

Mistake #4 – Failing to take into account your own individual circumstances: The four percent rule is a guideline, not a definite rule.

Your retirement plan should be unique to you and consider your circumstances.

Mistake #5 – Assuming that you will have the same expenses in retirement as you do now: Retirement is often a time when people have time to spend money on things like travel and hobbies that they didn’t have time for while working.

As a result, your expenses in retirement may be different than they are now.

Mistake #6 – Not factoring in Social Security: If you’re eligible for Social Security, be sure to factor this into your retirement plan.

Social Security can provide you with a source of income in retirement, which can help reduce the amount you need to withdraw from your nest egg.

Mistake #7 – Withdrawing in tax-inefficient ways: People do not consider the taxes they’ll owe on their withdrawals.

If you’re not careful, you could owe more in taxes than you need to.

That’s why investing with a tax-efficient account is important from the start.

Mistake #8 – Not having a plan B: Another mistake people make is not having a backup plan. What if the market crashes and your nest egg takes a hit?

What if you live longer than expected and run out of money?

Having a plan B can help you weather any storms that come your way in retirement.

As mentioned previously, we highly recommend having a fully funded emergency fund that can cover all expenses in case of a market crash.

The Bottom Line:

If you avoid these mistakes, you’ll be well on your way to a successful retirement.

Just remember to factor in inflation, plan for long life, and have a cushion for unexpected expenses.

You can make the four percent rule work with those three things in mind.

The Rule of 25 vs. the 4% Rule: What’s the Difference?

The Rule of 25 vs. the 4% Rule

The 4% rule indicates that you can withdraw 4% from your retirement and expect that the returns from your investment will surpass the withdrawal rate.

The problem is that with inflation added to this equation, the purchasing power of your money will decrease over time. If you withdraw 4% and the inflation rate was at 8% last year, you’re withdrawing 12% in purchasing power.

If the growth of your investment were less than 12% last year, then you would have to begin dipping into your principal, which is not ideal. This is where the multiply-by-25 rule comes in.

The rule of 25, on the other hand, is a general guideline that suggests you multiply your total salary by 25 to determine how much money you need to save for retirement.

This rule of thumb assumes that you will want to replace your current income via investments during retirement.

It also factors in an estimated annual return of around 10.5% but is used to calculate the total principal you’d need for retirement. It helps to build a mental framework for those pursuing financial freedom.

The 4% rule calculates how much you can withdraw from your principal after the 25x rule is implemented.

For example, first, you would use the 25 rule to calculate how much you need to have saved. Then, the four percent rule would tell you how much you can withdraw from that savings account each year. The 25x rule is a good starting point, but the 4% helps ensure you don’t outlive your money.

Common Questions About The 4% Rule

Q: How long will it take to retire if I follow the rule?

A: This depends on how much money you have saved and how much you can save each year.

Use the example mentioned above and adjust the variables to your preference.

Q: What happens if my retirement lasts more than 30 years?

A: If you want to retire sooner than 30 years, you will need to invest more each month. This is because compound interest will build more reserves for retirement.

You can also consider withdrawing only 2% rather than 4% to allow your investments to keep growing beyond 30 years.

Q: What if I can’t save enough money to retire?

A: If you cannot save enough money to retire using the four percent rule, there are a few options you can consider.

One option is working part-time in retirement. This can help supplement your income and give you something to do in retirement.

Another option is to downsize your lifestyle. Doing so will reduce your expenses and free up extra cash to help fund your retirement.

Lastly, you can delay retirement. This may not be ideal, but it can give you more time to save money and prepare for retirement.

Q: Is the four percent rule a guaranteed way to retire?

A: No, the four percent rule is not a guaranteed way to retire. It is simply a guideline that many people with success have used.

There are no guarantees in life, so it is important to remember that anything can happen when following this rule.

In Summary

The four percent rule is a simple estimate of your retirement savings needs.

Remember to take into account your circumstances when using this guideline.

With careful planning and consistent investing, you can ensure a comfortable retirement for yourself down the road.

Thanks for reading!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Real estate investing can be a great way to make money and build wealth over time. However, we’ve learned it’s important to do research and learn as much as you can from those who have been successful. This blog post will discuss the BRRRR method of real estate investing.

Many investors use this popular strategy to achieve success in the market. We will go over each step of the process so that you can understand how it works and decide if it is right for you!

This post may contain affiliate links; please see our disclaimer for details.

What Is The BRRRR Method?

The BRRRR method is a strategy for real estate investing that stands for “buy, rehab, rent, refinance, repeat.”

This methodology can be used in both residential and commercial real estate investing.

Buy: The first step is to find a good property you want to purchase.

Once you have found a property, you will need to put down a deposit and then close on the deal.

Rehab: After you have purchased the property, you will need to renovate or repair it so that it is in good condition and value is added.

Once the repairs are complete, you can rent the property to tenants.

Rent: After the property has been rented out for some time, you can refinance the property loan.

Refinance: You can conduct a cash-out refinance where you take out cash for the equity in your property and use it to purchase your next one.

Repeat: Once you have refinanced the property, you can then repeat the process by finding another property to purchase and rehab.

How The BRRRR Method Works

The BRRRR method is a great way to invest in real estate because it allows you to use other people’s money to finance your investment.

In the beginning, you will need to put down a deposit on the property.

However, once you have renovated the property and rented it out, you can refinance the loan and use it to buy another property.

This process can be repeated repeatedly to build up a portfolio of rental properties.

The BRRRR method is a great way to succeed in real estate investing!

Example of how the BRRRR method for real-estate investing works

You find a fixer-upper home for sale at a great price, put down a deposit, and close on the deal.

You then spend the next few months repairing and renovating the property. Once the repairs are complete, you start renting the property to tenants.

After a few years, you refinance the loan on the property at a lower interest rate. This saves you money on your monthly payments.

You then repeat the process by finding another property to purchase and rehab.

What Are The Benefits of The BRRRR Method?

Many top real-estate investors use the BRRRR method. Now that you know this strategy, let’s look at the benefits. Here are the top 8 benefits of the BRRRR Method:

Benefit #1: Allows You To Reinvest Your Money.

This is because you’re only using a small amount of your own money to purchase the property.

The BRRRR method allows you to borrow against the equity in your property to purchase additional properties.

Benefit #2: Creates Equity and Builds Wealth.

Your tenants will help to pay off the mortgage, creating equity in the property for you.

As your tenants pay down the mortgage, your equity in the property increases, building your wealth over time.

Benefit #3: Improves Cash Flow.

The BRRRR method can improve your cash flow because you can leverage the equity in past properties for a larger down payment on the new ones.

Your monthly mortgage payments will be lower, leaving you with more cash flow each month.

Benefit #4: Reduces Risk.

Using other people’s money can spread out the risk of investing in real estate. You can also use the BRRRR method to buy properties in areas you’re familiar with and understand well.

Benefit #5: It’s a Simple Strategy To Follow.

The BRRRR method is a simple strategy to follow and doesn’t require a lot of experience or knowledge to implement.

With just 5 easy steps, it’s easy to remember and implement.

Benefit #6: Can Be Used In Any Real Estate Market. This is a great benefit because it does not matter whether it’s a buyer’s or seller’s market.

You can still use the BRRRR method to find and purchase investment properties.

Benefit #7: It’s a Powerful Tool For Creating Passive Income.

If you’re looking for a way to create passive income, the BRRRR method is a great option.

By charging higher rent than the monthly mortgage payment, you get to enjoy the difference as passive income.

Benefit #8: It’s Perfect For Those Who Want To Build Their Portfolio Quickly.

This strategy builds a real-estate portfolio fast because you’re able to buy multiple properties in a short period.

By refinancing, you can access the equity in your properties to purchase additional properties.

In other words, you don’t have to spend as much time saving up for a downpayment.

The BRRRR method is a great way to invest in real estate because it allows you to build property equity over time.

By refinancing at lower interest rates, you can also save money on your monthly payments.

If you are looking for a way to build wealth through real estate investing, the BRRRR method is a great option.

What Are The Drawbacks of The BRRRR Method?

The BRRRR method is not without its drawbacks.

One of the biggest dangers of using this strategy is that you could over-leverage yourself if you’re not careful. This can lead to financial ruin if the real estate market takes a turn for the worse.

Another downside of the BRRRR method is that it can take a long time to complete a deal.

If you’re not patient, you could miss out on other opportunities while waiting for your BRRRR deal to come together.

A common drawback many new investors aren’t aware of is that you need good credit to qualify for the loans required to do a BRRRR deal.

If your credit isn’t great, you may not be able to get the financing you need.

The BRRRR method does not protect investors from mistakenly selecting the wrong property.

Even with a powerful strategy like the BRRRR method, you can still fail if you don’t purchase the right property.

This is because you may find yourself overpaying for renovations/repairs.

Let’s say the contractor leaves the job unfinished or takes too long, you may also end up paying a mortgage while the property is left without a tenant.

Selecting the right property is critical to success, and there are several factors you need to consider before making an offer.

Finally, the BRRRR method may require a lot of cash upfront. By not having enough cash, you’ll need to either get creative with your financing or find another investing strategy altogether.

Despite these drawbacks, the BRRRR method can be a great way to succeed in real estate investing.

Through patience and persistence, you can use this strategy to build a portfolio of rental properties that will provide cash flow for years to come!

Just make sure you understand the risks involved before diving in headfirst.

What Are The Risks of The BRRRR Method?

The most common risk factors when it comes to the BRRRR method is:

Destructive Tenants: These tenants can do serious damage to your property, which will end up costing you a lot of money in repairs.

Bad Contractors: As mentioned before, if you hire a bad contractor, they could take forever to finish the job or do a terrible job.

Over-leveraging: This is probably the most dangerous risk in BRRRR investing. If you’re not careful, you can easily over-leverage yourself and end up in financial ruin if the real estate market turns worse.

To avoid these risks, it’s important to do your due diligence when selecting properties and contractors. You should also have a solid plan in place for how you will finance your deals.

Having some extra cash, consulting lawyers, and being conservative with leverage can help reduce the risks involved with BRRRR investing.

Despite the risks, the BRRRR method can be a great way to invest in real estate and build equity over time.

How To Get Started With The BRRRR Method?

If you’re considering using the BRRRR method to invest in real estate, you should keep a few things in mind.

First, this strategy requires patience and careful planning.

Second, you need good credit to qualify for the loans required to do a BRRRR deal.

Finally, ensure you understand the risks involved before diving in headfirst.

Here’s an in-depth guide on how to get started with the BRRRR Method:

Step One: Find a property that you can buy below market value.

There are a few ways to find properties selling below market value. You can look for properties that are in foreclosure, short sale, or REO (real estate owned).

You can also look for properties that need significant repairs.

Tips For (B)uy:

Look for motivated sellers.

Get a real estate agent that specializes in finding distressed properties.

Use online search tools to find properties that are selling below market value.

The key is finding a property you can buy at a significant discount. This will give you the most equity in the property and the best chance for success.

Step Two: Renovate the property to add value.

Once you’ve found a property you can buy at a discount, it’s time to start the renovation process.

The goal is to add value to the property to maximize your return on investment.

Get multiple bids from contractors before you start the renovation process.

Make sure you have a detailed budget and timeline for the renovation project.

Be prepared for the unexpected.

Start with a vision and plan of how you want the finished project to look. You will need to get estimates from contractors for the work that needs to be done.

Decide if the renovations will add enough value to offset the costs. Once you have a budget, you can start finding a contractor and completing the work.

Step Three: Find tenants and start generating income.

The next step is finding tenants and generating income from your property.

The goal is to make enough monthly money to cover your mortgage, taxes, and insurance. This will create a positive cash flow situation for you.

Tips For (R)ent:

Screen your tenants carefully.

Make sure you have a detailed lease agreement.

Be prepared for repairs and vacancies.

You can find tenants by advertising your property online or through word of mouth.

Once you have tenants, it’s important to screen them carefully and make sure they are qualified.

Step Four: Refinance the property and pull out your equity (if needed).

After you’ve built some equity and paid off some of your mortgage loan with the help of your tenants, it’s time to refinance the property. This is where the BRRRR method gets its name.

Tips For (R)efinance:

Get multiple quotes from different lenders.

Make sure you understand the terms of your new loan.

Be prepared for closing costs.

You will need to find a lender willing to give you a loan for the property’s value after renovations. Once you have refinanced, you can pull out equity in the home as cash for the next property.

Step Five: Repeat and build your portfolio.

After completing the first 4 steps, you can now repeat the process and start building your portfolio.

The BRRRR method is great for building equity and creating a passive income stream.

By carefully selecting properties and managing your finances, you can succeed in real estate investing with the BRRRR method.

Tips For (R)epeat:

Keep track of your finances.

Diversify your portfolio.

Stay disciplined and learn from past mistakes.

The BRRRR method can be a great way to succeed in real estate investing if you know how to lower your risks.

If you are patient and careful, you can use this strategy to build a portfolio of assets that will provide passive income.

In Conclusion

The BRRRR method is great for those looking to make money in real estate investing.

It is important to research and understand each step of the process before getting started.

If you follow the BRRRR method, you can successfully invest in real estate! Another way to invest in real estate without being a landlord is with Fundrise.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.