This post may contain affiliate links; please see our disclaimer for details.

Managing money is a huge source of stress for a lot of people. Figuring out how to effectively manage your money can be daunting, but it doesn’t have to be.

There are some simple rules that you can follow to help make managing your finances easier. The 50/30/20 rule is one such rule.

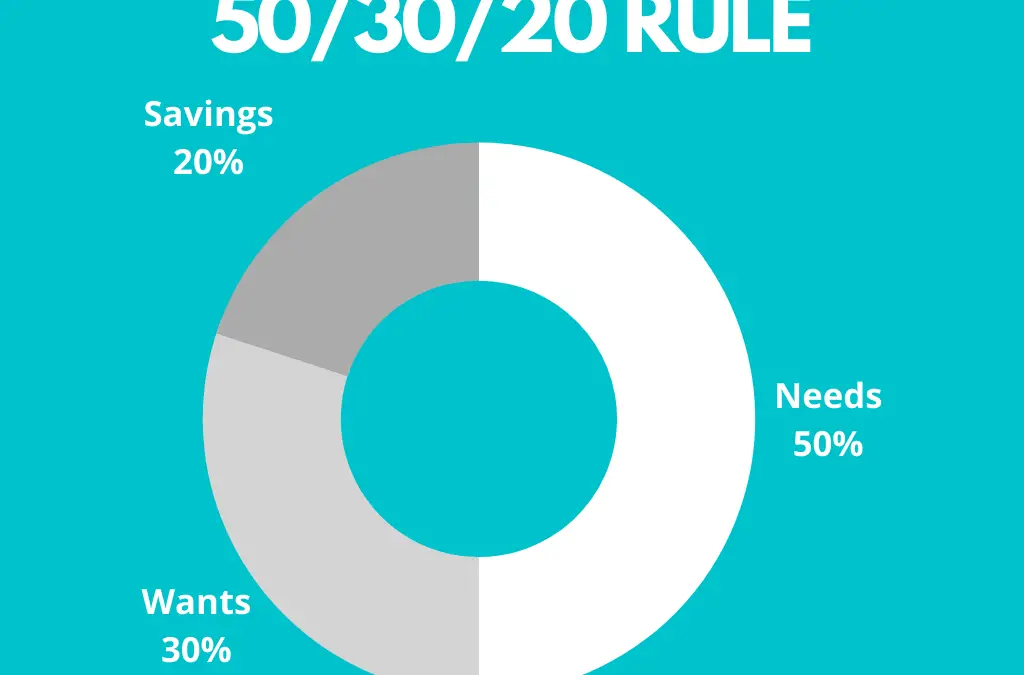

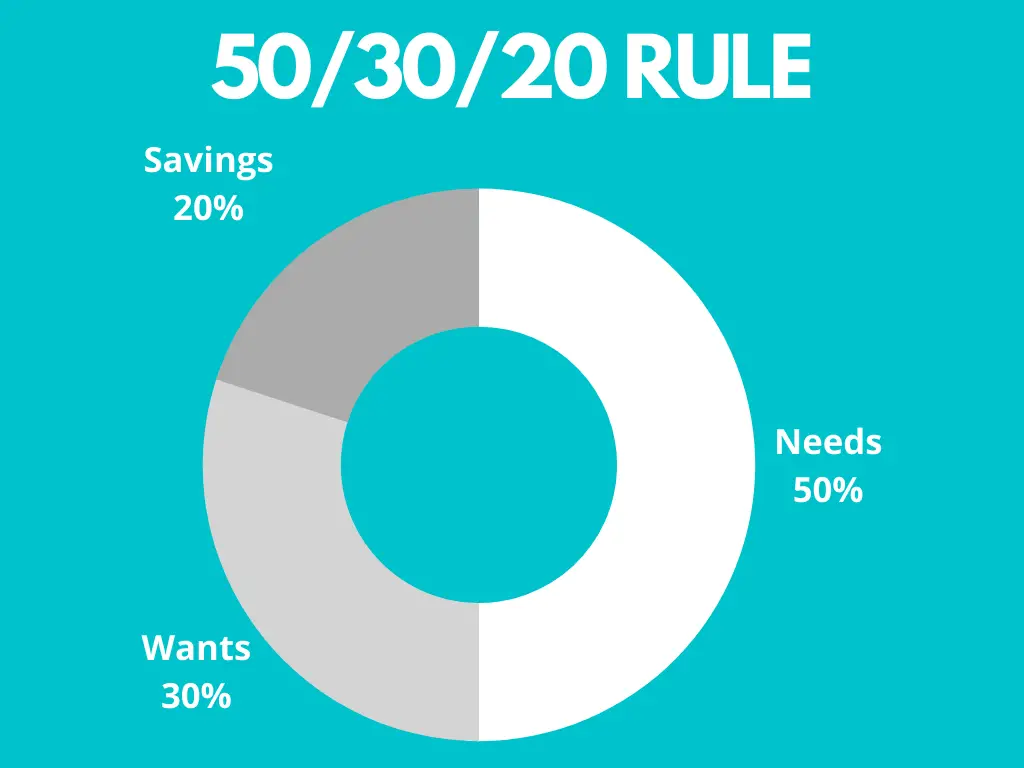

The method states that you should allocate 50% of your income toward essentials, 30% towards wants, and 20% towards savings.

50/30/20 Rule Pie Chart

In this article, I discuss the 50/30/20 rule in more detail and provide tips on how to apply it to your own life!

The 50/30/20 rule is a simple and effective way to manage your money. The rule states that you should spend 50% of your income on necessities, 30% on wants, and 20% on savings and debt repayment.

This may seem like a lot of work, but it doesn’t have to be.

You can start by creating a budget and tracking your spending for a month. This will give you an idea of where your money is going and where you can cut back.

Once you understand your spending patterns, you can begin to implement the 50/30/20 rule.

Start by allocating 50% of your income to necessary expenses such as rent, food, transportation, and utilities.

Then, allocate 30% of your income to wants such as entertainment, dining out, and shopping.

Finally, allocate 20% of your income to savings and debt repayment.

If you spend more than 50% of your income on necessities, try to find ways to cut back.

For example, you may save money on food by cooking at home more often or cutting back on unnecessary expenses.

If you are spending more than 30% of your income on wants, try to find ways to reduce your spending in this area.

For example, you may save money by watching movies at home instead of going out to the theater.

The 50/30/20 rule is a great way to get a handle on your finances.

By following this rule, you can ensure that you are spending your money in a way that is both responsible and enjoyable. So what are you waiting for? Start budgeting today!

Where Did The 50/30/20 Rule Come From?

The 50/30/20 rule is a personal finance guideline popularized by Senator Elizabeth Warren in her book, All Your Worth: The Ultimate Lifetime Money Plan.

The 50/30/20 budgeting method is designed to help you assess your financial needs and make changes to your spending habits if needed.

The goal is to end up with a balanced budget at the end of each month.

How To Budget Your Money With The 50/30/20 Rule?

The 50/30/20 rule is simple. You take your after-tax income and divide it into three categories:

How to budget your money with the 50/30/20 rule

50% goes towards needs like rent, food, transportation, and utilities

30% goes towards discretionary spending like entertainment, dining out, shopping, etc.

20% goes towards savings or debt repayment

Let’s say you make $2000 per month. With the rule, you would only have 50% of that to spend on living costs which is $1000. This probably means you won’t be able to get an upscale apartment or enjoy the luxury of the finest groceries and utilities.

30% of $2000 would be $600. That’s the amount you can spend on fun activities such as eating, watching a movie, or taking a trip.

The final 20% is $400. You would save or use this to pay off debt each month. In this particular scenario, the budget will look like $1000/$600/$400.

This leaves little room for error and forces you to be mindful of every penny you spend. However, it can be a great way to get your finances in order and start saving money.

The rule is flexible, though—if you have high student loan payments or are trying to save up for a down payment on a house, you can adjust the percentages accordingly.

The most important thing is that you are aware of your spending and are trying to save money.

The key concept is to ensure that the 20% assigned for savings and debt repayments does not go any lower.

It can be helpful to increase that number, but you should never look to decrease it.

Be careful with these other common mistakes when using the 50/30/20 rule…

Not including all expenses: When budgeting with the 50/30/20 rule, include all necessary expenses in the 50% category. This includes your phone bill, internet service, and health insurance.

Forgetting to account for irregular expenses: Remember to account for expenses that occur less often, such as car insurance and property taxes.

Treating the 50/30/20 rule as a hard and fast rule: The 50/30/20 rule is meant to be a guideline, not a strict set of rules. If you find that you can’t stick to the percentages exactly, don’t worry. Just try to get as close as you can and adjust as needed.

Examples of The 50/30/20 Method

Earlier in this article, we used the example of an income of $2000 per month. Let’s explore some more examples of different situations and levels of income.

If you earn $4000 per month, you will break it down into:

$2000 for 50% needs

$1200 for 30% wants

$800 for 20% savings & debt repayment

You earn $8000 per month, you would break it down into:

$4000 for 50% needs

$2400 for 30% wants

$1600 for 20% savings & debt repayment

If you earn $12,000 per month, you will break it down into:

$6000 for 50% needs

$3600 for 30% wants

$2400 for 20% savings & debt repayment.

The lessons from these examples are that your percentages will always stay the same, but the actual dollar amounts will obviously change based on your income.

Another thing to remember is that these are just guidelines, and you can adjust them according to what works best for you and your unique financial situation. It’s important to tailor this rule (or any financial rule, for that matter) to fit your own life and needs.

Now that we’ve gone over the basics of the 50/30/20 rule, let’s talk about how you can implement it in your own life.

Here are the steps to getting started…

Determine your after-tax monthly income: This is the amount of money you have to work with each month after taxes, and other deductions have been taken out of your paycheck.

Track your spending for one month: This will give you a good idea of where your money goes each month and where you may be able to cut back to save more.

Calculate your 50/30/20 breakdown: Once you know how much money you have to work with each month, you can start allocating it into different categories.

Make a budget and stick to it: This is probably the most important step in managing your money effectively. Once your budget is set, please do your best to stick to it as closely as possible.

Review and adjust as needed: As we said before, these guidelines are just that – guidelines. They’re not set in stone, so if something isn’t working for you or your circumstances have changed, don’t be afraid to adjust your budget accordingly.

Effective wealth management is imperative to discovering your financial freedom. That’s why we highly recommend PERSONAL CAPITAL.

This rule works so well because it forces you to think about your spending differently. Most people spend all their money on wants and then try to save whatever is leftover.

The 50/30/20 rule flips that around by ensuring you save money and use the remaining amount for your wants.

The 50/30/20 rule is a great way to start saving and budgeting because it provides a simple framework you can follow.

Once you understand how the rule works, you can start to tweak it to better suit your needs.

For example, if you have a lot of debt, you may want to adjust the percentages to put more toward debt repayment.

How the 50/30/20 Method Works

You spend 50% of your income on necessities like housing, food, transportation, and healthcare. This number works because, for most people, these expenses stay relatively constant from month to month.

30% of your income goes towards wants or discretionary purchases. This could include things like travel, entertainment, and clothes. Using 30% should work for these purchases because they shouldn’t cost more than your living expenses.

It also gives a fair amount of wiggle room for unexpected expenses.

20% of your income is saved or invested for the future. This could be for retirement, an emergency fund, or other financial goals.

Consistently saving, investing, or paying down debt with 20% of your income works because it allows you to make significant progress on your long-term financial goals.

Is The 50/30/20 Budget Right For You?

Ask yourself these questions to find out if the 50/30/20 budget is right for you.

Do I have a shopping habit?

Do I get paid a lot but don’t have money to pay down debt?

Do I have trouble setting a framework for my personal finances?

Do I need to start budgeting to have more financial freedom?

If you answered “yes” to any of the above questions, the 50/30/20 budget might be a good fit for you.

If you find that you are not able to stick to the 50/30/20 rule, don’t worry. The most important thing is that you start trying to save and budget your money.

The 50/30/20 Rule Is Right for you if…

You want a simple framework to follow

You need help allocating your income into different categories

You want to start saving and budgeting but don’t know where to begin.

It’s up to your lifestyle & money choices

In some circumstances, the 50/30/20 budget might not be right for you. This can be true for those that don’t need to spend anywhere close to 30% on fun activities and have most of their living expenses covered (living with relatives, walking to work or working from home, etc.)

If you have high debt or want to save to invest sooner, you can adjust a percentage from the 30% fun category and increase your 20% savings column.

For some people, the rule can look like 50/10/40. This scenario would result in very little discretionary spending, but it will also get you out of debt or save for investments much more quickly.

If you have low living expenses and not much desire to spend on fun activities. The rule in this case, can look something like 30/10/60. This means 30% goes to living expenses, 10% to fun, and 60% to savings, debt repayment, and investing.

This accelerated rule is a great way to reach financial freedom faster, but it can be stressful. That’s why the 50/30/20 rule is great. It’s a stress-free and manageable way to budget effectively!

So is the 50/30/20 budget right for you?

As you can see, there is no one-size-fits-all answer to this question. The 50/30/20 budget may be right for you, or you may need to adjust it to fit your unique circumstances. The most important thing is to make an effort to save and budget your money.

Try out different methods and see what helps you save the most money.

You may even want to try using multiple methods at once. However, this can overcomplicate things. That’s why the 50/30/20 rule is the perfect standard to follow.

For most people, the 50/30/20 budget is a great starting point. It’s simple and easy to follow, making it perfect for those just getting started with budgeting.

If you believe you can benefit from the 50/30/20 budget, give it a try! You may be surprised at how much easier it is to save money than you thought.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Looking to improve your credit score fast? Don’t worry, you’ve come to the right place.

It’s no secret that mortgage rates are on the rise. According to CNBC, “In just a matter of months, mortgage rates have surged just over 3% for a 30-year fixed loan to just north of 5%”.

This article will discuss 13 genius tips that will help boost your credit score! Follow these tips, and you’ll be on your way to a better credit rating in no time.

You can check out our YouTube video if you prefer to watch instead of reading.

In this day and age, your credit score is super important. A good credit score can help you qualify for a loan, get a lower interest rate, and rent an apartment.

On the other hand, a bad credit score can result in higher interest rates and difficulty getting approved for loans.

That’s why it’s important to do everything you can to improve your credit score.

And fortunately, there are a few simple things you can do to give your score a boost.

This post may contain affiliate links; please see our disclaimer for details.

How are credit scores calculated?

Credit scores are calculated based on several factors, including:

Payment history

Credit utilization

Length of credit history

Types of credit

New credit inquiries

Let’s take a closer look at each of these factors and how you can improve your score in each area.

Payment history is one of the most important factors in determining your credit score.

Therefore, it’s important to always make your payments on time.

If you have missed any payments in the past, now is the time to start making them on time. This will show creditors that you’re serious about paying your debts and improve your chances of getting approved for new loans.

Credit utilization is another important factor in determining your credit score.

This is the amount of credit you’re using compared to the amount of credit you have available.

For example, if you have a credit card with a $1000 limit and you’re carrying a balance of $500, your credit utilization would be 50%.

You can improve your credit utilization by paying down your debts and keeping your balances low.

Creditors like to see that you’re not maxing out your credit cards, so this is a great way to improve your score.

Length of credit history is another factor that lenders look at when determining your creditworthiness.

The longer you’ve been using credit, the better.

Therefore, it’s important to keep old accounts open even if you don’t use them often.

Creditors will see and care that you have a long history of responsible credit use.

Types of credit also affect your credit score. Creditors like to see that you’re using a variety of different types of credit, such as revolving credit (e.g., credit cards) and installment loans (e.g., auto loans). This shows that you’re able to manage different types of debt responsibly.

New credit inquiries are the last factor we’ll discuss. Whenever you apply for new credit, it will result in a hard inquiry on your report.

Too many hard inquiries can hurt your score, so it’s important to only apply for new credit when you really need it.

Now that we’ve discussed the factors that go into your credit score, you might be wondering, does a good credit score matter? The simple answer is yes.

Why Does A Good Credit Score Matter?

A good credit score can save you money. A bad credit score can cost you money. It’s as simple as that.

For example, let’s say you’re looking to buy a new car. If you have good credit, you’ll likely qualify for a lower interest rate on your loan. This could save you hundreds or even thousands of dollars in interest payments over the life of the loan.

On the other hand, if your credit is poor, you may not qualify for a loan at all. Or, if you do qualify, you’ll likely be stuck with a high-interest rate which will end up costing you more in the long run.

A good credit score can also help you get into an apartment.

Many landlords check your credit score before approving you for a lease application. And if your score is low, you may be denied service or required to pay a deposit.

Another reason why a good credit score is important is that it can help you get a job. Many employers will check your credit history as part of the hiring process. And if your score is low, it could be a red flag for them and they may decide to hire someone else instead.

As you can see, having a good credit score is important for many different reasons. Fortunately, there are a few simple things you can do to improve your score.

So a good credit score is important because it can save you money and help you get approved for the things you need in life. By following the tips we’ve discussed in this article, you can start boosting your credit score today!

How To Increase Your Credit Score?

Now, let’s discuss how you can increase your credit score.

Here are 13 genius tips to improve your credit score fast…

Before we begin, it’s important to note that there is no one-size-fits-all solution when it comes to improving your credit score.

What works for one person might not work for another. So, take these tips as general guidelines and tailor them to your own situation.

Tip #1: Pay your bills on time

One of the biggest factors that affect your credit score is your payment history.

So, if you want to boost your credit score fast, you need to make sure that you’re always paying your bills on time.

Even one late payment can negatively impact your credit score, so it’s important to be vigilant about making all of your payments on time, every time.

Tip #2: Keep your balances low

Creditors like to see that you’re not maxing out your credit cards, so keep your balances low.

You can improve your credit utilization by paying down your debts and keeping your balances low.

Tip #3: Use a mix of different types of credit

Creditors like to see that you’re using a variety of different types of credit, such as revolving credit, installment loans, and even store credit cards.

So, if you want to boost your credit score fast, make sure to use a mix of different types of credit.

Tip #4: Check your credit report regularly

Another important tip to boost your credit score fast is to check your credit report regularly. This will help you catch any errors or discrepancies that could be dragging down your score.

You can get a free credit report from each of the three major credit bureaus once per year.

Remember always to ensure that it is a soft check, not a hard one. Keep reading as we go over the differences between the two.

Tip #5: Dispute any errors on your credit report

If you do find any errors on your credit report, make sure to dispute them right away. You can do this by writing a letter to the credit bureau that issued the report.

Tip #6: Use automatic payments

One easy way to make sure that you’re always paying your bills on time is to set up automatic payments.

That way, you’ll never have to worry about forgetting a payment or being late on a payment.

Tip #7: Consider a balance transfer

If you have multiple high-interest credit cards, another great way to boost your score is to transfer the balances to a single low-interest card. This will help reduce your overall debt and show creditors that you’re working to pay off your debts.

Just make sure you don’t incur any new debt on the cards while you’re working on paying off the balance transfer.

Tip #8: Use a credit monitoring service

If you want to keep an eye on your credit score and ensure you’re always taking steps to improve it, consider using a credit monitoring service.

These services can help you track your progress and give you personalized tips to improve your score.

Tip #9: Get help from a professional

If you’re having trouble boosting your credit score on your own, consider getting help from a professional.

A credit counselor or financial advisor can provide valuable guidance and help you create a plan to improve your credit score.

Tip #10: Ask for a higher credit limit

A helpful tip to consider if you want to boost your credit score is to get a credit card with a higher limit. This will improve your credit utilization and show creditors that you can manage more credit responsibly.

Just make sure you don’t max out the card and always pay your bill on time. If you do, you’ll see a significant boost in your credit score in no time.

Tip #11: Prepay the balance and plan ahead

If you know you’ll be carrying a balance on your credit card for a couple of months, one way to avoid paying interest is to prepay the balance.

This way, you can pay off the entire balance before interest accrues. Have the money available in your account so you don’t overdraw and incur fees.

This helps to prevent you from going over your credit utilization ratio for larger purchases.

It’s a good idea to have a couple of months’ worth of payments saved up so you can prepay when necessary.

Tip #12: Get a lower interest rate credit card

Another tip to consider if you want to boost your credit score is to get a credit card with a lower interest rate.

Doing so will help you save money on interest and show creditors that you’re a responsible borrower.

Tip #13: Stay patient

Last but not least, it’s important to stay patient when you’re trying to boost your credit score.

It takes time to make improvements, so don’t get discouraged if you don’t see results overnight. Just keep working at it and you’ll eventually see the improvements you’re looking for.

Take these 13 genius tips and put them into action to boost your credit score fast!

Remember –

The sooner you start working on improving your credit, the better off you’ll be in the long run.

So don’t wait – get started today!

How Long Does It Take To Rebuild Credit?

The answer to this question largely depends on your credit situation. If you have a long history of late payments, it will take longer to rebuild your credit than if you have a shorter history or no late payments.

You can expect changes every 30 to 45 days, so it may take a few months to see significant improvement. It’s important to do a soft credit check, not a hard credit check, as the latter can harm your score.

Soft Credit Check: This type of credit inquiry does not impact your credit score. This is the ideal type of credit check to do if you are looking for new credit, such as a credit card or loan.

Hard Credit Check: This type of credit inquiry will show up on your credit report and temporarily lower your credit score. This is the type of credit check you should avoid if at all possible.

Patience is important when rebuilding your credit. The key takeaway is to follow all these steps and avoid the common mistakes that could hurt your progress.

If you’re having issues with improving your credit, I highly recommend checking out The Credit Pros! They are a very reputable company that offers incredible credit repair services.

They have all of the tools needed to help rebuild your credit, and you can check your credit score for free!

By following the 13 genius tips above, you can give yourself a much better chance of success. Do your best to stay patient and consistent with your payments, and you’ll eventually see your score improve.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

When receiving your electricity/energy bill each month, do you ever wonder what it really means? It’s not just about the numbers; it’s about the energy used to power your home.

Electricity is a necessity in today’s world.

We use it for everything from powering our homes to cooking our food, so it’s important to know how much we are using and how much we are spending.

It’s important to remember the amount of energy we use can also impact the environment.

So as consumers, we often think about how to cut costs and save money in our daily lives.

This can range from saving money on groceries, catching general sales, and overall household budgeting. But what about your electric bill?

The electric bill seems like one of those bills that happen and you have little control over it.

In modern times, lighting, cooling, and heat are necessities so going without electricity sounds absurd. But that doesn’t mean you have to like paying a high electricity bill every month.

There are ways to help lower your electricity bill without sacrificing your electricity.

One of the easiest ways to reduce your electric bills is by turning off the lights when you are not in a room.

This will not only save money on electricity, but it will also help the environment by reducing carbon emissions and air pollution.

The cost of electricity has been rising steadily for the past decade, and prices are expected to continue climbing.

Lowering your electricity bill should be a priority if you’re trying to save money and fortunately it’s quite easy to do and there are several ways you can tackle this!

The Benefits of Lowering Your Electricity Bill

With the cost of living rising, many people are looking for ways to lower their electricity bills.

Lowering your thermostat could be one of the ways to save money on your tax bill.

In the winter, you may want to lose heat in your house by taking down a couple of window panes to lower the interior temperature. High humidity can cause mold and mildew growth, so a dehumidifier could help save on electric bills.

The average person spends $2,000 on electricity a year. This can add up to a $200+ monthly bill.

One of the most surprising benefits of lowering your electricity bill is that you can save up to $120 per year on your electric bill.

If you lower your energy use by 10%, you’ll save $20 each month and $120 a year.

10 Surprising Ways To Lower Your Electric Bill

1. Use a programmable thermostat

Programmable thermostats are great for controlling your home’s temperature on a schedule.

You can set it to adjust the temperature when you are away from home automatically.

This means that your heating or cooling system is only working when it needs to be, which will save you money on your utility bills in the long run.

Below is a very popular choice; the Nest Thermostat uses a sensor and GSP from your phone to know whenever you are leaving home.

2. Install LED light bulbs

LED light bulbs are more energy-efficient than traditional light bulbs and last much longer.

They also emit less heat, so they won’t raise the temperature in your home as much as regular bulbs.

This will help keep your energy bills down and make it easy to light your home efficiently.

3. Turn off the lights

Turning off the lights when you are not using them may seem a little obvious, but it can be surprising how much we forget to flip the switch when we leave the room.

This is highly beneficial because it saves money, energy, and pollution.

Most importantly, it helps to save the planet by reducing greenhouse gas emissions.

4. Turn off the electronics

Much like our lights, we may also forget to shut down other electronic devices.

They can drain our energy even when we are not using our electronics. We use a lot of electricity to power these devices.

The best thing you can do to save energy is to turn them off when you are not using them.

5. Use your dishwasher more efficiently

Use the dishwasher only for full loads of dishes and turn it on only during periods of high energy demand (usually in the evening).

Running your dishwasher when it is not full of dishes can waste water and energy.

If the dishwasher runs during periods of high energy demand, you will be charged a higher rate for electricity.

Appliances with motors, such as clothes washers, dishwashers, and ovens can use up to 3,600 kilowatt-hours per year.

You could alternatively wash your dishes by hand.

6. Dry your clothes on a clothesline

You can do this with a timer instead of running your electric dryer all day.

This is a big green living tip.

The convenience of a dryer is great, but if the weather is nice and warm, it can be much more beneficial to hang our clothes on a clothesline.

This also gives your clothes a nice natural scent to them.

7. Reduce the use of all major appliances during peak hours

This includes dishwashers, clothes washers and dryers, ovens and stoves, space heaters, air conditioners, and dehumidifiers.

We mentioned dishwashers above, but applying the same idea to all of your major household appliances can be beneficial.

Even the smallest appliance can use a lot of power. A space heater uses up to 1,000 kilowatt-hours per year. And an air conditioner or dehumidifier can use between 2,400 and 10,800 kilowatts per year.

Your energy provider should know how much your appliances use if you want to know the exact numbers.

8. Install energy-efficient windows

Use a double-paned glass that is tinted for better insulation from the heat in summer and cold in winter.

This is beneficial as it will help keep your house at a more balanced temperature, and you won’t need to use the air or heat as often.

9. Use a power strip with multiple outlets

Doing this can help you control and turn off all appliances that are not in use.

When you’re not using your electronics, it’s best to turn them off. But what should you do when there aren’t enough outlets in a room to plug all of them in?

You could use a power strip with multiple outlets to plug all of your devices into one outlet while they are turned off. This will help reduce the amount of energy wasted when they are plugged in but not in

Unplug appliances not in use or have an automatic shut-off after a certain period. This will prevent them from using energy when they’re not needed. It is estimated that about 10-15% of the energy used in a house is wasted because of appliances that are plugged in but not in use.

The best way to reduce this usage is by unplugging appliances that are not being used for an extended time or have an automatic shut-off after a certain time.

10. Install power-saving devices on appliances

These devices will automatically turn off the appliance when it is running at full capacity and then turn it back on when it needs to be used again.

With higher power rates, it is necessary to ensure that you use your appliances efficiently.

To learn more about these sorts of devices, contact your electricity company. Not only will this save money, but it will also cut down on wasted energy.

Conclusion

Reducing Your Electric Bill Is a Great Way to Boost Your Finances While Also Doing the Planet a Favor

The average American spends $2,000 a year on electricity. However, many people don’t know how to reduce their electric bills and are paying too much for their energy usage.

However, we know that there are various ways to reduce energy consumption and save money without feeling like you’re sacrificing any convenience.

Reducing your electric bill is a great way to boost your finances while also doing the planet a favor.

Use our helpful tips above to reduce your electric bill. Remember to turn off any electronics when they are not in use.

Install LED bulbs in addition to specially made energy-saving bulbs. Invest in a programmable thermostat to have smarter control over the temperatures in your house.

Be sure to double-check smaller devices such as laptops, lamps, TVs, and computers for more places you save electricity.

Finally, going back to hand washing your dishes and hanging your clothes out to dry may seem archaic and this day and age, but it can go a long way in helping you save on your electricity bill.

Please do your part and see the benefits in your wallet and on our planet. Let us know other ways you’ve been able to save money on electric usage in the comments section below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

There’s much debate about whether you should pay off your mortgage early or invest your money.

Both options have their own set of pros and cons. Finding out which one is the right choice for you can be tricky.

In this article, we’ll look at both sides of the argument. Hopefully, by the end of this post, you will be able to make an informed decision for your financial future!

Should you pay off your mortgage early or invest the money?

This is a question that many people are asking these days, including us on our fire journey.

It’s important to note that both options have their own benefits and drawbacks.

Let’s examine each option in more detail to help you decide which is right!

This post may contain affiliate links; please see our disclaimer for details.

Pay off the mortgage early or invest

What Does the Math Say? Loan Interest Saved vs. Investment Gains

When deciding whether to pay off your mortgage or invest your money, it’s important to look at the numbers.

First, let’s see what the math looks like if you didn’t pay off your mortgage early and didn’t invest money.

You have a $180,000 total mortgage on a 30-year plan (10% downpayment of $20,000).

Over the 30-year amortization period at a 5% interest rate, you would have made 360 monthly (12x per year) payments of $960.64. You would have paid $180,000.00 in principal, $165,831.56 in interest, for a total of $345,831.56.

If you do not pay your mortgage early, you will have paid almost as much interest as the principal.

But what would happen if you paid even just $100 extra per month on top of your minimum?

The math of paying off your mortgage first ($100)

Let’s use the same data listed above but say you paid only $100 extra per month.

You would have made 292 monthly (12x per year) payments of $1,060.64 ($960.64 + $100.00) and one final payment of $469.09. You would have paid $180,000.00 in principal, $130,176.91 in interest, for a total of $310,176.91.

In this scenario, your 30-year mortgage would be paid off approx 5.5 years sooner, and you’d save $35,654.65 in interest charges!

The math of paying off your mortgage first ($500)

Let’s step it up a little. What would happen if you paid even just $500 extra per month on top of your minimum?

Over the 30-year amortization period at a 5% interest rate, you would have made 172 monthly (12x per year) payments of $1,460.64 ($960.64 + $500.00) and one final payment of $655.86.

You’d still have paid $180,000.00 in principal but only $71,886.49 in interest for a total of $251,886.49.

In this scenario, your 30-year mortgage would be paid off approx 15.5 years sooner, and you’d save $93,945.07 in interest charges!

As you can see with the math, paying off your mortgage early is advantageous. But how does that compare to investing your money first?

The math of investing your money first ($100-$500)

On the other hand, choosing to invest could potentially see much higher returns.

For example, if you started with $20,000 and invested $100 per month in the S&P 500 with an average return of 10.5%, in 30 years, you will have $616,908.93.

That’s a huge difference compared to if you kept that in the bank earning next to 0% interest. You’d only have $56,000 saved in the bank after 30 years!

With an investment of $500 per month in the same asset with the same average return for 30 years, you can expect to see a balance of $1,485,140.10!

Paying Off Your Mortgage First: The Pros

When it comes to paying off your mortgage early, there are several pros to consider:

Save money each month. You’ll save on interest payments over the life of the loan, which can add up to a lot of money.

Peace of mind: Knowing that your mortgage is paid off will give you peace of mind and financial security. Especially when you know you have a physical place you can live in.

Build equity: Paying down your mortgage will help you build equity in your home faster. This can open opportunities for a home equity line of credit, allowing you to borrow against your house to buy more assets if you wish.

Lower Interest Rate: You may get a lower interest rate on your mortgage if it’s paid off early.

Debt Free Sooner: You’ll be debt-free sooner and won’t have to worry about making monthly mortgage payments.

More Financial Freedom: Once your mortgage is paid off, you’ll have more financial freedom and can use your money for other things.

Less Risky Than Investing: Paying off your mortgage is relatively low-risk, whereas investing can be risky. With mortgage payments, you can easily track how much longer it would take to pay off your house and own the property.

Paying Off Your Mortgage First: The Cons

While there are definite advantages to paying off your mortgage early, there are also a few potential drawbacks.

Missed Opportunities: You may miss out on potential investment gains if you use your money to repay the loan. Compound interest is a powerful tool, and over time you could earn more money by investing your money than you would save by paying off the mortgage.

Strained Budget: Paying off a mortgage early can strain your monthly budget, as you’ll have less money to work with each month. This can make it difficult to cover other expenses or save for future goals.

Difficult To Save For Other Assets: It may take longer to save up for a down payment on a new home if you’re putting all of your extra money toward the mortgage

Less Flexibility: You may not have as much flexibility with your finances if you’re focused on paying off the loan as quickly as possible

These are all valid concerns that should be considered before deciding whether to pay off your mortgage early or invest your money.

Invest Your Money First: The Pros

Now let’s look at the other side of the argument, investing your money instead of using it to pay off your mortgage. There are several potential benefits to this approach; let’s learn more.

Start investing sooner: You may be able to grow your investment faster than you could pay off the loan. This can be essential for long-term compounding.

More options for lucrative investment opportunities: You’ll have more flexibility with your finances if you’re not focused on paying off the mortgage as quickly as possible

Diversify your portfolio: Owning more assets and diversifying your portfolio can help reduce your overall risk.

Potential for higher returns: With a good investment, you could make more money than you would save by paying off your mortgage.

These are all good reasons to consider investing your money or using it to pay off your mortgage. However, there are also some potential drawbacks to keep in mind.

Invest Your Money First: The Cons

Just like there are pros to paying off your mortgage early, there are also cons to investing your money instead:

Bad investments: There’s always the risk of losing money on your investments; that’s why it’s important to diversify investments and not put the majority of your money into high-risk investments.

Riskier Than Paying Off Mortgage: Investing is inherently riskier than paying down your mortgage, as there’s no guarantee you’ll make any money back.

Takes Longer To Pay Off Mortgage: If you choose to invest your money, it will take longer to pay off your mortgage. This could mean paying more in interest over the life of the loan.

These factors are worth considering before deciding which route to take with your money.

Which is better? Paying off your mortgage or investing your money?

There’s no easy answer, as it depends on each individual’s unique circumstances. However, you can make the right decision by carefully considering all the pros and cons.

When weighing the pros and cons of each option, it’s important to consider what could happen in the worst-case scenario. Doing so will help you make an informed decision about what’s best for you and your finances.

Worst Case Scenarios

When deciding which option to choose, investing or paying off your mortgage, it can be helpful to look at the worst-case scenarios.

To make an informed decision, you need to understand the risks and the potential rewards involved.

Paying Off Your Mortgage Late: The Worst-Case Scenario

If one day you lose your job or main source of income, and you can’t make your monthly mortgage payment, you could end up in a very difficult situation. You may have to sell your home at a loss or even face foreclosure.

Investing Your Money: The Worst-Case Scenario

If you invest your money and the stock market crashes, you could lose a significant portion of your investment. This could leave you in a difficult financial situation and cause you to miss out on important growth opportunities.

A Synergistic Approach

The good news is you don’t have to pick only one strategy! You can pay more than your minimum monthly payments and automate an investment strategy.

This synergistic approach will allow you to reap the rewards of compound interest while also paying off your mortgage early.

What a $100 split strategy would look like:

For example, let’s say your mortgage payments are $960.64 and you have an extra $100 per month. You can pay $50 as a monthly prepayment allowing you to pay off your mortgage faster and use the other $50 to invest in an asset like the S&P 500 which returns on average 10.5%.

By the end of the amortization period, with your monthly (12x per year) prepayment of $50, you save $20,174.19 in interest and pay your mortgage off 37 months sooner than if you had the same mortgage with no prepayment.

With the other $50 per month invested (after an initial $20,000 investment, same as 10% on a $200,000 house), you will have $508,380.03.

Here’s what it would look like with $500 split between the two options evenly:

With your monthly (12x per year) prepayment of $250.00, you save $66,450.76 in interest and pay your mortgage off 129 months sooner than if you had the same mortgage with no prepayment.

In 30 years, you will have $942,495.62 if invested using the same metrics above except with a $250 monthly contribution.

As you can see, splitting your allocation evenly between the two options can help you gain both of the benefits. By the end of it all, you’d have a solid retirement fund and get to enjoy being debt-free sooner.

You may prefer debt-free sooner over a large fund in a few decades. If so, you can allocate more of your monthly income towards that endeavor. However, this should help illustrate the benefits of using both strategies.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

You can customize your investments with your debt management to your preference.

Just remember that compound interest works best when starting early. It’s also important to know that the S&P 500 has relatively predictable returns. Each investment will have its own risk-to-reward ratio.

A synergistic approach may be the best overall strategy for you. Paying more than your minimum monthly payments and automating an investment strategy will help ensure success on both fronts.

Ultimately, the choice between paying off your mortgage or investing your money is a personal one. There’s no right or wrong answer, and the best decision for you will depend on your unique financial situation.

You could try enjoying the benefits of both strategies. Invest some of your money and pay more than the minimum monthly payment on your mortgage.

Whatever you decide, remember to start early and do your research before making any decisions with your money.

We hope this blog post has helped you weigh the pros and cons of each option. Best of luck to you on your financial journey!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Getting approval for a home mortgage may not be easy, especially if you are a first-time homebuyer. Lenders look for many things when deciding whether or not to approve a mortgage application.

According to Forbes, about one-third of Americans without a high credit score are rejected for a home loan mortgage.

This blog post discusses 15 expert tips to increase your chances of getting approved for a home mortgage!

This post may contain affiliate links; please see our disclaimer for details.

Being approved for a mortgage can be a nightmare if you do not know these strategies and tips. This is because a mortgage is a large loan, and lenders are careful when they lend their money.

They want to make sure that you can repay the loan, and they will look at various factors to determine this.

So let’s jump into the 15 tips I’ve prepared!

1) Track all income and expenses.

One of the most important things you can do before applying for a mortgage is to create a budget and stick to it. Know where all your money is coming from and leaving to.

This will show the lender that you are financially responsible and can stay disciplined within your budget. It is important to include all of your income and expenses in your budget, including debts and bills.

Lenders want to see that you can afford your monthly mortgage payments, other expenses, and/or debt payments.

If you show them that you can live within your means, they will be more likely to approve your mortgage application!

Another thing that lenders look at when considering a mortgage application is the amount of money you have saved up for a down payment.

The more money you can put down on your home, the more likely you will get approved for a mortgage.

Generally, if you cannot put down a 20% down payment, you will need to pay mortgage insurance.

The larger the down payment, the lower your monthly payments will be, and the more likely you will get approved for a mortgage.

If you struggle to get a mortgage, a lower total loan amount can help. Saving up can be difficult but well worth it in the long run. I wrote another article specifically sharing 15 Frugal Living Tips to Save a Ton of Money; feel free to check it out!

3) Have a good credit score.

Lenders consider your credit score one of the most important factors when approving a mortgage application.

If you have a good credit score, it will show lenders that you are responsible for your finances.

If you have any negative items on your credit report, it is important to clean them up before applying for a mortgage.

This will show lenders that you are improving your finances and are more likely to make your monthly payments on time.

To boost your credit score, make sure to pay your bills on time, keep your credit utilization low, and don’t apply for too many loans at once.

4) Get pre-approved for a mortgage.

Getting pre-approved for one is a good idea if you want to increase your chances of getting approved for a mortgage.

This means that you have already been through the underwriting process and have been given conditional approval for a mortgage loan.

Doing so will give lenders confidence that you are a good risk and increase your chances of getting your mortgage approved.

You can use a traditional or an online lender to get a pre-approved mortgage.

Online lenders can often give you a decision more quickly, but they may not have as many loan options available.

5) Have a solid job history.

Lenders also look at your job history when considering a mortgage application.

They want to see that you have been employed for two years, which shows stability and responsibility.

If you have been unemployed or had a lot of job changes, it may not be easy to get approved for a mortgage.

6) Have a low debt-to-income ratio.

Another thing that lenders look at when considering a mortgage application is your debt-to-income ratio. This is calculated by dividing your monthly debts by your monthly income.

Lenders want to see that you can afford to pay for debt payments, along with all of the other living expenses.

If you show them that you can handle debt effectively, it can help raise your chances of being approved for a mortgage.

We were able to pay off $56,000 of school loan debt by using the debt snowball method, this helped lower our DTI significantly!

Tips for raising your income:

Job hunting

Ask for a raise

Start a side hustle

Invest in assets that produce passive income

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

A low debt-to-income ratio is important for mortgage approval.

For example, consider the two following scenarios:

Consistent income of $100,000 per year and have $0 in debt.

Earning $15,000-$20,000 per year and having $10,000 in debt.

If you were a mortgage lender and only had money to invest in one borrower, which one would you choose to lend to? The answer is clearly number one.

7) Save up for closing costs.

When applying for a mortgage, you must save up for closing costs.

These are the fees and expenses that are associated with getting a mortgage. Closing costs typically range from about three to five percent of the total loan amount, so it is important to budget for them.

By showing your lender that you are prepared for all the costs associated with getting a mortgage, you will increase your chances of getting approved.

8) Get help from a Mortgage broker.

If you are unsure how to get approved for a mortgage or have been denied, it may be helpful to work with a mortgage broker.

A mortgage broker can find you the best possible deal on a mortgage and help you navigate the application process.

9) Wait until you are ready.

One of the most important things to remember when applying for a mortgage is to wait until you are ready.

Don’t apply for a mortgage unless you are sure that you can afford the monthly payments. This will only lead to disappointment and could damage your credit score.

Your lack of confidence in paying your monthly payments will cause lenders to disapprove your application.

11) Start building credit ASAP

If you don’t have a lot of credit history or do not have a good credit score, it is important to start building credit (or fixing it) as soon as possible.

This will show lenders that you are responsible with money and can be trusted to make your monthly payments on time.

When applying for a mortgage, shopping around for the best options is important. This means comparing interest rates, terms, and fees from different lenders.

By doing your research, you can find the mortgage that is best for you.

The more mortgage options you have, the more likely you will be approved by at least one. However, it’s still important to consider the other tips on this list.

12) Find a co-signer

If you have difficulty getting approved for a mortgage, you might consider finding a co-signer.

A co-signer agrees to sign the loan with you and is responsible for making the payments if you default. This can be a family member, friend, or business partner.

The co-signer will need to have good credit and a steady income. And they should be aware of the risks involved before agreeing to sign the loan.

If you default on the loan, the co-signer will be responsible for the debt, and their credit will be impacted. So it is important only to use a co-signer as a last resort.

13) Rent to own

This is a type of contract in which you agree to rent a property for a specific period, with the option to purchase it at the end of the lease.

This can be a helpful way to get approved for a mortgage if you don’t meet all the requirements.

15) Lease options

This is similar to renting to own but gives you the option to buy the property immediately instead of waiting until the end of the lease.

This can be a good option if you are unsure if you want to purchase the property.

15) Government-backed loan

If you have difficulty getting approved for a mortgage, you may consider a government-backed loan.

These loans are backed by the federal government and have more flexible requirements than traditional mortgages.

Government-backed loans include FHA loans, VA loans, and USDA loans. Each loan program has eligibility requirements, so be sure to research which is right for you.

You may also want to talk to your local housing authority about government-sponsored mortgage assistance programs.

Conclusion

These are just a few tips that can help you get approved for a mortgage.

Be sure to research and talk to a lender about the best options. And remember, it’s always best to prepare for a mortgage well in advance.

Following these tips can improve your chances of getting approved for a mortgage. We wish you the best on your purchasing home journey.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.