This post may contain affiliate links; please see our disclaimer for details.

The hot topic of discussion recently is inflation. As many of you know we are suffering from a surge in inflation. The purpose of this article is to explain what inflation is, what causes it, how it affects each of us, and how to protect yourself against it.

You’ve probably noticed by now when buying groceries adding gas to your car etc. Everything has become more and more expensive.

See the image below that depicts how inflation has increased in just one year!

Inflation Increase Per Category

Right now is the biggest inflation we’ve seen in the United States in the past 30 years and has made many of us overwhelmed.

Things are getting more and more expensive with everyday expenses are getting bigger and bigger!

From the prices of vegetables, fruits, and oil to the prices of cars and housing prices. The rise in everything has affected all aspects of life including our food, clothing, housing, and transportation.

To start off, let us go over what inflation is exactly and what causes it.

What is Inflation?

Inflation in short refers to the increase in the prices of goods and services. It measures how much the price has risen over time and tracks how the value of the currency falls due to the price increase.

The truth is that inflation is nothing new, it is around us every single day.

It’s just that recently inflation has become crazy. This has made us pay more attention to its presence.

Normally inflation increases about 2.5% every 30 years.

But the “annual inflation rate in the US accelerated to 6.8% in November of 2021, the highest since June of 1982”. – Trading Economics

What Causes Inflation?

There are generally two causes of inflation: the first one is Demand-Pull Inflation, the other one is Cost-Push Inflation.

Let’s walk through each one.

Demand-Pull Inflation

Demand-pull inflation can be caused when the demand for goods increases but the supply stays the same.

When there’s a surge in demand and sellers can’t keep up with the supply, their prices will increase. The result is called demand-pull inflation.

Cost-Push Inflation

Cost-push inflation occurs when the supply of goods is low, but the demand for goods is unchanged. As a result, the prices are pushed up.

For example: when COVID-19 broke out, the global supply chain had major disruptions. Because of the lack supply issues like computer chips, caused the car market became very hot. The lack of lumber caused the cost of building a house to become more expensive.

How inflation affects us?

Our standard of living is mainly based on two factors: your income and expenses.

Inflation will reduce the purchasing power of income while increasing daily expenses, thereby harming the standard of living.

Salaried income will only increase a little each year but expenses will suddenly increase a lot. This creates a major negative impact on life.

Our family’s expenses increased by at least $100 monthly for our cost of living.

I currently own a little Toyota Corolla, and it has awesome gas mileage. The cost to fill up the entire tank used to be $25 but now it’s $45!! My heart reaches out to all the SUV and Truck owners out there, gas has become a major expense!

I am still shocked to see how much it costs me each time to fill up. Also when going to the grocery store we can tell the price of food and many other items have increased a lot.

How to Protect Ourselves from Inflation?

Here are three ways that can help you be protected from inflation.

Budget and Save

Invest in the Stock Market

Invest in Real Estate (Even Your Own Home)

1.Budget and Save

No matter what it is important to budget and save money, making sure to not spend money where it doesn’t need to be spent.

Figure out how much money you need for essentials like rent, food, and transportation.

Next, figure out how much you can afford to spend on non-essentials like entertainment and dining out.

When you know how much money you have to work with, it’s easier to stick to your budget.

Subscriptions can really add up and are sneaky with their auto-renewals.

We’ve learned it’s important to control the urge to buy lots of subscriptions.

Right now our only subscription is with Amazon Prime. Well.. actually that and my Xbox live account. haha

When you know how to budget your life well, then you can save more money to invest.

Tip #3 Use Alternatives

Just because you’re trying to save money doesn’t mean you have to give up your hobbies or entertainment.

There are always cheaper alternatives!

Instead of going out to the movies, rent a movie from Redbox.

Or, instead of going out to eat, cook at home.

There are plenty of ways to have fun without spending a lot of money.

2. Invest in the Stock Market

Holding stocks may be a good way to fight inflation. When companies sell their products at rising prices, this will lead to increased revenue and earnings, which inevitably lead to a rise in stock prices.

When it comes to funds, we love the Total Stock Market Fund and S&P 500. If you don’t know what to invest in, they both can be a good starting point!

When you invest your money wisely, you can earn interest and dividends! It is an amazing tool against inflation.

We love how interest and dividends are passive income – you can earn it while sleeping!

A great way to start investing is by putting money into some tax advantage accounts such as an HSA or an IRA. Tax-advantaged accounts can save you a lot of money in tax!

M1 Finance is a great place to get started with their super easy-to-use app. There are NO commission and account management fees.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance if you would like to open a brokerage account or a retirement account! For more details on how you can start investing with M1 Finance click HERE.

3. Invest in Real Estate (Even Your Own Home)

Real estate can be another great tool to fight inflation, and you’ve probably noticed how housing prices have risen over time – just ask a grandparent or parent how much they purchased their house for.

Indeed, the real estate bubble is usually accompanied by a correction period. For example, the housing crash in 2008. Nevertheless, on average, house prices tend to rise over time which offsets the effects of inflation.

This post may contain affiliate links; please see our disclaimer for details.

Real estate is a very hot investment topic and an incredible tool to help achieve FIRE (Financial Independence Retire Early).

“Ninety percent of all millionaires become so through owning real estate.”

Andrew Carnegie

Many think a lot of money is needed to start investing in real estate, but this is wrong.

You may have heard of people who have achieved great success in real estate investing. Our success may seem small to some but we would like to share our story.

When we purchased our first real estate property, we were just college students at ages 21 and 23. We did not have a lot of money and did not have high-paying jobs!

We started our real estate investment journey with only $20,000.

Now $20,000 has become $250,000 in 4 years while going to school.

We have bought three properties total but sold our first one in order to graduate student-debt free!

We don’t have a lot of money, so there is no way we can afford to buy rental property directly like some people or spend a lot of money to hire professional contractors to do remodeling.

Our real estate investment strategy

Buy as owner-occupied (residential property).

Do some easy remodeling while living there.

Save up a downpayment for the next property.

Buy the next house and rent out the previous one.

Now I’d like to dive into our own investing experiences!

I hope our stories can provide you with knowledge and inspiration for your own investing journey.

First Real Estate Property–Townhome

Shortly after my wife and I were engaged, we started to discuss whether to rent or try and buy a place after we were married.

My in-laws owned real estate in China so my wife possessed a very great investment perspective – regardless of us just being college students.

Many people would tell me, “Just rent! most college couples rent then slowly build up to purchasing their first home”.

My wife would tell me she would not pay rent to a landlord. This will be our first property and not our forever home.

So we decided to buy a place to rent out in the future!

She also mentioned the location we were looking at was an excellent location – close to two colleges!

The townhome we found was $100,000. It was an older, cute townhome built-in 1970 with two bedrooms and 1.5 baths.

The previous owner had some nice remodeling done such as repainting and new flooring.

We were so happy when our offer was accepted!

In total, our downpayment was $20,000. Since the downpayment was 20% of the house price we did not have to pay mortgage insurance, woohoo!

Our monthly mortgage payment was around $850 with HOA, taxes, etc.

I still remember on closing day when the employee at the title company said, “wow! your monthly mortgage payment is even cheaper than couples who are renting!”.

After living at the townhome for a little over one year we bought our second property (condo) and rented out the townhome.

We did some simple remodeling on the townhome such as switching old appliances to new (most affordable) ones, repainting, fixing some damages, etc.

The enhancements and repairs were really just simple. The total expenses occurred from this were around $4,000.

Repainting First Property Front Door

We were happy to find a very nice newlywed couple as our first tenants! The rental income was $1000 a month which gave us $250 extra cash flow each month!

We had been renting it out for around two years then in order to graduate debt-free, we sold it for around $140,000 total.

The original price we bought it for was around $100,000.

Second Real Estate Property–Condo

Before buying our second property (condo) I had received a job offer as an account manager at a financial software company.

At that time I switched all of my college classes to online so my schedule could be more flexible.

Upon receiving the job offer we started looking for another property in Utah. We decided only to do a 5% down payment for a new property.

The reason we didn’t do more than 5% is that we did not have a lot saved and we wanted to purchase a place as soon as possible. The housing market at the time was quite hot.

We knew the sooner we could close the sooner we could start building equity.

Being our second property, we could only apply for a conventional loan with a minimum requirement of 5% down.

We also had to pay PMI (mortgage insurance) since the down payment did not reach 20% of the loan’s total amount.

We eventually found a cozy 3 bedroom/2 bath condo built-in in 2002. The previous owner had new painting and flooring done which made the property very attractive to a young couple like us.

The location was also very close to our college, our first property, and my new company.

On top of that, the condo was also only 3-5 minutes from Walmart, Costco, and other shopping districts! Talk about a great location!

The total price of the condo was $171,000. Our down payment + closing costs were $10,000 total.

The monthly payment with HOA and mortgage insurance included was just about $1,200.

When COVID-19 happened, the interest rates dropped significantly. We noticed these amazing interest rates and decided to refinance this condo!

After refinancing, our monthly mortgage payment went down to around $1,000 (with HOA fees), saving us $200 a month!

After living in the condo for around 2 years we rented it out for $1,300. This gave us around $300 a month in cash flow!

Similar to our first property, we did some simple remodeling before renting it out.

We painted all the old cabinets fresh white! Painting is the cheapest remodel method and only costs us $100.

The microwave broke when we lived there so we bought a new one which was under $200! It was a returned one at Best Buy but had no issues. They had a hard time selling it so the Manager gave us an extra discount 🙂

Currently, we are renting out this amazing condo.

We checked condos in the same community and found the value of our condo has increased by at least $100,000 since we purchased it.

We are so grateful for the equity being built in this cute condo.

Third Real Estate Property – Single Family Home

Originally, we were not planning to buy a third property anytime soon. The plan was to wait until I graduated first with my MBA.

We started to look around at different builders just for fun. One of the builder’s sales agents wrote down our contact information and within one week he told us new lots were being released soon.

Since the location was close to my parents’ house, we decided to check it out but still just for fun.

Two days later the agent told us there would be a price increase of $5,000 for any new homes built. Any contract signed within the next few days would keep the lower price.

We thought it through and decided to go under contract.

The prices had been steadily increasing and we felt it would be a good decision to lock in – especially since the house-building process takes many months.

The new home was under construction in July of 2020. The building process was very interesting and took ten months to finish.

We officially closed on the house / third property in May 2021!

The total price of our new single-family home was just around $340,000 (with upgrades included).

We only did a few upgrades and chose the cheapest home base model so we could have a very healthy cash flow.

The square footage of the home is 2,300 with a lot size of 0.12 acres. We put down a 5% down payment which cost us $20,000 total.

Our locked interest rate is 3% with mortgage insurance being about $35. In total, our mortgage payment each month is $1,600.

We finished our entire yard 2 months after we moved in to welcome our sweet Samoyed puppy named Tofu!

Now we are working on furnishing our 833 sqft basement before our daughter is born. It’s a lot of work, but I’m learning many valuable handyman skills! 🙂

The cost for finishing both our yard and basement will be approximately $20,000. A lot we did by ourselves but some parts were hired out.

We have checked the current prices for the same home (model) as ours in our community. Especially with the basement and yard finished, our third real estate property has increased at least $100,000 in value.

Conclusion

The story above is of our three real estate properties that we bought in the time period of 4 years while in college.

You can see that we didn’t spend a lot of money to renovate our first two real estate properties.

There are two reasons for this –

I did not have a lot of handyman skills back then.

As college students, we didn’t have money to hire contractors.

But still, we make some nice profits! Just try your best to start saving now for a down payment!

One more thing I want to say is that we are also been very fortunate.

The past few years have been a very good time to invest in real estate in Utah. We were able to buy a house when the price was still relatively cheap, and then watch it increase in value.

The value is still increasing and having rental income as passive income is an amazing thing!

We are so grateful we have been able to see our real estate investments jump from 20K to 250K in 4 years during college.

We do not place all of our investment eggs in real estate but it has been a powerful FIRE tool!

We’d love to hear your thoughts! Feel free to drop a comment or question below.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

There are so many reasons to spend money, especially when kids come into the picture. Many people may find it incredible or even unbelievable that we save56% of our income with one kid.

But we do it and so can you!

This post may contain affiliate links; please see our disclaimer for details.

“Among respondents, 20 percent said they aren’t saving anything or don’t have an income. Another 47 percent are saving 1 to 10 percent, and 27 percent are saving 11 percent of their income or more”.

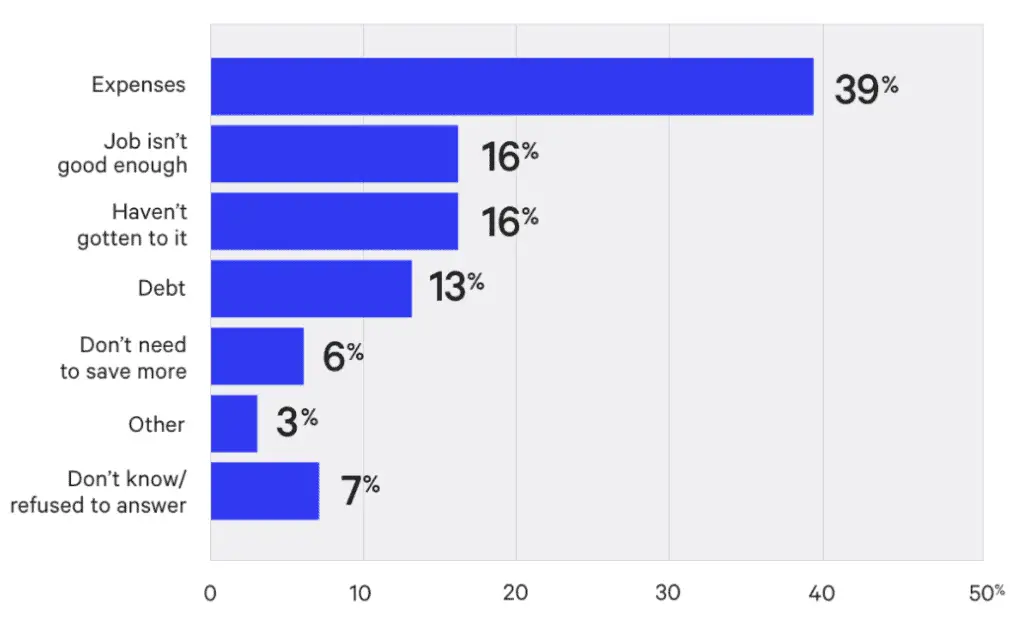

See below for the main reasons people don’t save more money –

Saving Money Survey From Bankrate.com

Before sharing some must-see saving tips, you probably want to know how much we are currently making right?

My wife and I’s total pre-tax income is currently $100,000 including both of our salaries (basic salary + bonuses) and our extra rental income. After-taxes are we are looking at about $7,000 a month (net).

The 56% is calculated using our net income/after-tax income which equals us saving roughly $47,000 a year.

Now I hope you’re ready for our 12 useful tips – we can’t wait to share them with you!

If you’d like to watch our YouTube video instead, please see the video below.

1) Pay off all Debt Except for the Mortgage

A lot of debt is being accumulated by individuals all across the world each year.

According to business insider, the average American has $52,940 worth of debt across mortgage loans, home equity lines of credit, auto loans, credit card debt, student loan debt, and other debts like personal loans.

Debt is the enemy of saving!

Debt steals from the money you could be saving!… when you need to pay $500 in debt payments a month, you are actually losing $500 that could have been extra savings each month.

When it comes to how to pay off debt, we are big fans of the debt snowball method and used it to pay off our $56,000 worth of student debt and had one kid.

The journey is not easy but IS worth it.

Now we are 100% debt-free except for the mortgage. Staying away from debt allows us to save (and INVEST) more of our income and reach financial freedom sooner.

2) Avoid Becoming ‘House Poor’

Someone who is house poor has maxed out their mortgage payments so the majority of their income goes to the mortgage.

BTW, those who are house poor are not only includes homeowners but also renters.

We know many people who have maxed out their loans when buying a home. They all have a very high DTI (debt to income ratio) which ends up around 45%.

Ouch!

45% of your pre-tax income all going to debt?! – Big NO-NO for us.

Our largest expense is our monthly mortgage payments but we had a plan when buying a home.

When applying for our house loan our goal was to keep all house costs (mortgage+utilities+internet) under 30% of our net income.

We feel 30% with everything is a healthy percentage. We don’t want to max out our house loan debt because we’d rather not be house poor.

By keeping our mortgage payment as low as possible we are able to have extra cash to save and invest – woohoo!

3) Mint Mobile – Incredibly Priced Phone Plan

Phone plans can get super pricy with long contracts!

Our friends recommended Mint Mobile back in the day and we have been using them ever since.

Their plans have incredible prices with plans as low as only $15 a month!

My wife and I only pay $15 each for our phone plans (a month). Their service has been very reliable. To see these incredible deals, click HERE or on the image below.

4) Cancel Unnecessary Subscriptions

Subscriptions are eating most people’s money every month!

Control the urge to get lots of subscriptions, it’s important to recognize wants verse needs.

Right now our only subscription is with Amazon Prime. Well.. actually that and my Xbox live account. haha

We are fortunate to be able to use our parents’ or other family members’ subscriptions like Netflix, Disney+, and others. Big thanks to my family here!

Amazon Prime has been amazing though and has been worth it for us so we’d like to share some awesome things about it.

Here are 3 main benefits which made us buy and KEEP it.

First, we love the free 2-days shipping.

Second, we love that Amazon Prime offers unlimited photo storage space because we have tons of pictures! If you need to pay monthly for online photo storage, why not just get Amazon prime bundled with the other benefits that they offer?

The third is Amazon music. Their music has been great at increasing my productivity and boosting my mood.

5) Side Hustles

Making an extra $10K is easier than trying to save 10K. The sooner you understand that the sooner your life will improve.

We love pets! Finding a side hustle you enjoy is the best.

We would help friends or family out to watch their pets. My wife is from China so she knew a lot of international students who don’t have family here so we would help watch their pets while they go back to China.

For us, this was not a job at all and we both enjoy playing with each pet (by the way, we would only watch pets that were fully trained, so it wouldn’t be hard to take care of them).

We also enjoyed using the pet sitting site/app called Rover, if interested you can click HERE for more details.

Another side hustle I took up was donating plasma.

You can make around $400 a month, sometimes even more! Each donation took me around one hour total and up to two donations can be scheduled each week.

Donating plasma was easy and is also for a great cause. I still donate plasma sometimes when they have a good promotion going on.

We hope you can also find something you enjoy for a side hustle!

6) Find a Higher Paying Job

Making more money means you can save and invest more money!

In addition to doing side hustles, I have constantly worked on improving my skills in the workplace to be able to find higher-paying positions.

Back when going to school I would do both full-time school and full-time work. I was able to move up to a supervisor position when I first got married. Next, I was able to obtain an account manager position during the last year of my bachelor’s program. I then became a product development specialist after the first semester of my MBA.

I understand how difficult it can be to leave a position or company you are comfortable with, but I was able to increase my knowledge, capabilities, and income!

Each change in job position gave me about a $15,000 increase in salary.

In total, my salary increased by $30,000 during school! I quickly moved to another position once I became comfortable with my job responsibilities and looked for opportunities to expand my knowledge and skills.

7) Buy a Second-Hand Reliable Car with Cash

The average value of a new vehicle drops around 20% in the first year of ownership, and will drop up to 60% of its value within the first five years!

Buying a reliable car with cash can save you tons of money! Here is my story below –

Ever since I was a kid I loved the Land Rover Discovery model. During college, I decided to get a car loan for a second-hand Land Rover that had high mileage.

I did not realize what I had gotten myself into…

At first things I was living the dream… or so I thought! I would go off-roading with my buddies but then the nightmare arrived.

The vehicle started having many small issues which were VERY costly to repair. Being a Land Rover model, the repairs and basically everything is very pricy.

The cost to fill up on gas was very high and the gas mileage was terrible. Then my tire blew out when off-roading with friends. The cost to replace all tires cost me almost a thousand dollars! I had no savings left over each month and needed to get rid of it.

I was able to sell the vehicle (after a long time) and used the money to pay off my car loan completely.

That was a relief! No more car debt.

I then purchased a second-hand Toyota Corolla from my brother-in-law at a really good price. My brother-in-law has his own car shop and Toyota is his number one favorite brand due to its reliability.

I was very happy with my Toyota Corolla as it had no issues. The gas mileage was also so much better compared to the gas guzzler I previously had.

See HERE for more on my luxury car nightmare story.

8) 48-Hour Cooldown Rule

We all have ‘wants’ that sometimes just feel like needs! lol

It doesn’t help if the thing we want is also something a friend or family member just purchased and is pressuring us to do the same.

My wife and I have set a 48-hour calm time to prevent misspending of our money. Usually, we calm down after a night’s sleep but extending it to 48 hours has worked well for us.

It’s important to distinguish between what you want and what you need – try finding someone else who can support you in the 48-hour cooldown.

If there is still something I really want I will donate plasma as extra money. For example, I really want the brand-new released x-box and I did not cool down haha. So I donated plasma and bought it.

9) Live More Frugal – Buy Second-Hand and Discounted Items

We buy a lot of things second-hand, and found it’s usually not worth it to buy brand new!

We like using the Facebook marketplace and have found items like our baby’s toys, stroller, pack-n-play, and more!

We also look for sales. Before going to Smith’s or Costco, we always check what’s on sale first.

Essentially everything we buy from Costco is on sale, no kidding!

If you have a baby, we highly recommend buying the Target store brand up&up for diapers and wipes.

Here are 4 reasons we recommended using Target –

First, they are one of the cheapest brands out there with good quality. We used Walmart store brand Parents’ Choice which is around the same price, but it doesn’t compare in quality.

Second, Target often offers “buy $100 get $30 off” promotions so I always buy a bunch during those promotions. I think with the promotions, the Target store brand up&up has the cheapest diapers and wipes. At least we haven’t found anything cheaper than that.

Third, Target also offers Target RedCard. You don’t need to open a credit card, just open a debit card! The debit card they have offered 5% cashback when you shop in Target!

Last but not least, Target also has a Target Circle Rewards program. Target Circle is a loyalty program where you can earn 1% in Target Circle earning rewards every time you shop!

The above four reasons can really help parents with babies like us to save A LOT of money. That’s why we are using Target store brand up&up for our babies.

10) Shop Around for Insurance

After we first got insurance we would talk about finding cheaper insurance or bundling but we didn’t do anything for a long time. Thinking back on it now we both regret not taking action to find cheaper insurance faster.

The insurance we currently have is for the car, house, and rental (landlord) insurance.

We switched to an insurance company recommended by our real estate agency. The insurance for our car, home insurance, and landlord insurance are combined/bundled.

Having your car and house insurance together with the same insurance company is usually cheaper. The new insurance company we chose gave us a plan that is cheaper than our old plan by about $100 per month.

Saving an additional $100 a month means you can save $1,200 a year! Making the switch may be well worth it.

11) Minimalize

We started watching minimalism videos and were very intrigued by the idea of simplifying our lives and removing things that do not add value.

This also gave us more motivation to not spend money on things we didn’t need. Having a minimalist mindset helps us know what we really need, we ask ourselves, “does this item really add value to my life?”.

We also don’t want to have too much clutter in our home so we will ask ourselves questions when shopping like “do we need this?”, “is it necessary?”, or “how long/much will I use this item?”.

We are not full-blown minimalists, but the idea teaches us valuable lessons on what matters most and how to save our income.

12) Invest Your Money

When you invest your money wisely, you can earn interest and dividends! You will be making money even while sleeping!

Compound interest is an amazing thing that can really go to work for you.

We highly recommend investing early and starting now. The growth may seem slow at first but it grows like crazy over time!

Check out this example below –

The average monthly student debt payment in the USA is around $400 a month. If you instead invest $400 a month in a reliable fund (like the S&P 500) with average an average return of 12%, you will have around $92,000 in 10 years and ONE MILLION in 28 years!

A great way to start investing is by putting money into some tax advantage accounts like an HSA or an IRA. Tax-advantaged accounts can save you a lot of money in tax!

F1 Finance is a great place to get started with their super easy-to-use app. There are NO commission and account management fees.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using F1 Finance if you would like to open a brokerage account or a retirement account! For more details on how you can start investing with M1 Finance click HERE or on the image below.

Conclusion

The most important thing to saving your income is to cut down on expenses and increase your income! That’s how we are able to save 56% of our income!

I hope the 12 tips shared can give you a good idea of how to start saving half of your income.

Here is a quick summary of all 12 tips:

Pay Off Debt Except for the Mortgage

Avoid Becoming ‘House Poor”

Mint Mobile, $15 Phone Plan

Cancel Unnecessary Subscriptions

Side Hustles

Find a Higher Paying Job

Buy a Second-Hand Reliable Car

48 Hour Cooldown Rule

Live More Frugal – Buy Second-Hand and Discounted Items

Shop Around for Insurance

Minimalize

Invest Your Money

What other things are you doing to help you save more each month? Be sure to comment below and share with us!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

I’d like to start out my weight-loss story by first sharing my weight-gain story. Then we can dive into the 12 weight loss tips I’ve prepared.

The first tip really shows how I was able to lose weight and make money.

It all began back when I started working at a call center. I sat most of the day and enjoyed unhealthy snacks and soda a bit too much.

Not long after starting my new job I met the girl of my dreams and got married in 2017.

At that point, I was still on the fast weight-gain track and continued to gain lbs ended up with a big ‘dad bod’ weighing a whole 270 lbs!

I had tried so many different weight loss strategies such as a low-carb diet, intense intermittent fasting, a low-calorie diet, etc.

Each method was difficult to maintain and I found myself losing a little weight and then gaining it back super fast.

I tried and failed different workout programs such as Insanity. Consistency was lacking in my life and it became very discouraging.

I’m sure many of you can relate to the ups and downs of trying to lose weight.

In 2020, my incredible Son was born and I realized I had to be in better shape for both my Wife and Kiddo.

I became very serious and signed up for a Triathlon with two of my brothers. I also started a HealthyWage challenge.

In this article, I want to share how I changed my entire mindset and habits to finally lose some real weight. I’ve learned the importance of starting small and being consistent.

Small and consistent habits will change your life!

Here is a before and after picture (don’t mind the weird bandanna that had fake long hair attached to it) haha.

This post may contain affiliate links, please see our disclaimer for details.

The outcome of my weight-loss journey so far has been amazing – I feel much healthier and am now working towards a new goal of getting down to 200 lbs!!

Now I’d like to share with you 12 weight-loss success tips I learned myself and have used to lose 35 pounds in 6 months! These tips have also helped me maintain better mental health while losing weight.

Tip #1 – Find a way to make yourself accountable (and MOTIVATED).

When becoming very serious about weight loss I found my WHY, but really dug into my why and kept asking questions until I found my ‘root’ desire for losing weight.

Try searching for your reason or why FIRST and then find a way to keep you accountable.

I loved the idea of doing a Sprint Triathlon to keep me accountable and motivated.

When signing up for the triathlon with my two brothers I was extremely out of shape.

Many doubts about being able to get ready in time hit me but I was able to summon up enough courage to sign up. This action kept me both accountable and motivated to not give up when things got tough.

Second, I had heard about HealthyWage where you can bet money to reach a certain weight in a specific amount of time. Not only could I lose weight, but I could also MAKE MONEY!

I bet $200 for 6 months ($1,200 total) that I could lose 35 pounds in those six months. I would then win $338 in interest for a grand total of $1,538!

Making this big of investment was scary but VERY motivating! Making an investment in your health is more than worth it.

Signing up for HealthyWage is super easy and you can choose how much you want to bet each month – making it customized for your needs and goals.

The app is also very user-friendly and helps show you where you should be at DAILY on your weight. You can also join other challenges to increase your winnings.

Below is a screenshot of when I reached my weight goal and was able to cash out my winnings! 🙂

My Success Using HealthyWage

By signing up for a Sprint Triathlon and HealthyWage I was held accountable and given extra motivation when I felt unmotivated.

Tip #2 – Be aware of calorie consumption, but don’t over-stress it!

Alright, so I probably tried 20 + calorie calculators to make sure I have the EXACT amount of calories needed to lose weight each day.

I quickly found out that calories are not all created equally with some calories keeping you fuller for longer.

I also tried low-calorie (and low carb) diets, both left me hungry most of the time and I kept running out of calories fast!

Don’t get me wrong, having a calorie deficit is important for weight loss, but don’t over-stress calorie counting.

For example, I have an idea of how many calories I eat each day but I try to focus on consuming the RIGHT and BEST calories for my body such as fruits, veggies, lean meats, etc.

If you’re a busy individual and want a custom meal plan then I highly recommend trying NutriSystem! You can start by taking a survey and then will have balanced and nutritious meals and snacks sent to you!

Right now you can buy a month and get an entire month free! – Click HERE to get started! 🙂

Tip #3 – When things get tough, take a HUGE step back.

Many times during my weight loss journey I would feel down or depressed. Sometimes the cravings felt too hard to resist.

Taking a HUGE step back and going to a quiet, calm place really helps!

For me, I love getting outside for fresh air and taking deep breaths. After calming down and remembering my WHY the cravings tend to fade away.

I also learned it’s ok to sometimes have sweets or just have them in small amounts. Restricting anything 100% is very difficult and not healthy in the long run.

Tip #4 – Being consistent MOST OF THE TIME is key.

Too many times I would start BIG. I would try an intense workout or diet but each time I would fail.

I highly recommend starting small, super small. Find something achievable that can be accomplished on a regular basis.

The key is being consistent MOST OF THE TIME with small, achievable habits when first starting out.

When working on building muscle, I literally started with 5-10 minutes of floor workouts but would MAKE SURE to be consistent.

Tip #5 – Remember, you can always start fresh.

It’s okay to slip up. Try to not be too hard on yourself, love yourself, and use positive self-talk.

Go back to the basics, and remember those small achievable goals you’ve set.

I’ve also learned the importance of NOT waiting for Monday to come around! Too many times I would put off my health goals until the next week.

By having small achievable goals, it is much easier to start again immediately – a fresh start is always available.

Tip #6 – Don’t require perfection, it’s not gonna happen.

Getting out of the ‘I’ve completely failed’ mindset is difficult and can still be a challenge.

I’ve learned that we should not expect perfection from ourselves, but expect improvement.

This also goes back to not restricting anything 100%. This makes cravings more intense and binging more likely to happen. I know that whenever I would have tons of sweets or unhealthy foods it felt harder to change.

Remember to love yourself, and be forgiving if you make a mistake.

Finding joy in the journey is most important.

Tip #7 – Exercise takes many forms.

Exercising doesn’t have to always be for a set amount of time or a specific exercise/program. Don’t get me wrong, exercise programs can be great and provide structure/accountability.

What I would like to emphasize is it’s important to be flexible.

I worked full time while going to school full time for a long while and would be hard on myself if I didn’t get in a certain exercise or amount of time in for exercise.

I believe it’s good to have structure and set aside time for exercise, but many times I would not have a lot of time so I would make sure to walk more that day or at least do something.

Try doing exercises that you enjoy and get creative! Going on an outing or playing sports with family or friends is just one example of an enjoyable form of exercise.

Tip #8 – When I say start small, I mean small!

This tip goes hand in hand with tip #7 – exercise takes many forms. An example of starting really small is that I would go on a lot of outings with our kid or work on finishing our basement.

At first, I wouldn’t count these activities as exercise and felt I needed to run a mile to get a good workout, but I realized I actually was walking and moving a lot.

When first creating a new habit it’s important to start small and acknowledge your successes.

My body was in an ACTIVE STATE so I knew I was doing something good.

Try building small habits first.

Another example is how I didn’t start running, cycling, or biking every day to prepare for my triathlon. I would start with a 5-10 minute designated walk then slowly work my way into a jog as the weeks continued.

Tip #9 – Limit sugar, bad fats, processed foods, and fried foods.

It’s honestly best to cut out these types of foods or at least for the most part.

The truth is, they don’t provide you with the necessary nutrition.

I try my best to limit these types of foods and only have them as part of a cheat meal once a week. That way I didn’t worry about never having them again.

When you eat healthy foods instead of sugars, processed foods, etc. the calories don’t seem to matter very much and do not add up as fast as having a large hamburger with fries – save that for one cheat meal (NOT cheat day, not cheat week).

Tip #10 – Find alternatives – focus on what you CAN eat

Focusing on alternatives was a great way to help me lose weight.

Finding alternatives is a great way to help train your mind to change.

Instead of saying “I can’t eat that”, I would try to tell myself “I can have THIS instead”.

This is a list I used while losing weight that really helped me realize there are many healthy and yummy alternatives out there.

Whole Foods

Fruits

Veggies

Protein Shakes

Zero sugar drinks

Grilled food

Vitamins

Water, water, water

No added sugar foods

My Alternatives

Try writing a list of your favorite alternatives and put it somewhere you can see it frequently to remind you that losing weight shouldn’t be that hard!

The list I provided is more generic but there are many specific foods (or drinks) for each one that I love.

Tip #11 – Beware of items labeled “low fat”

You’ll see lots of items in the supermarket labeled low fat.

I found out that many times they can even be worse for you. For example, reduced-fat peanut butter lacks important healthy fats for your body. Instead, I use “no added sugar” peanut butter.

Any time I see something labeled as reduced or low fat I will make sure to do more research before risking my health.

Many times these types of items have MORE sugar than the regular product.

Tip #12 – Change your relationship with food

It’s important to have a positive outlook on ALL foods.

Find foods you love to eat, try new things!

One thing I’ve tried recently that I love is hot lemon & honey water. It’s delicious and refreshing.

Also remember it’s okay to eat unhealthy foods once in a while! Just work on putting more healthy foods into your body.

Extra Thoughts & Summary

Another weight-loss method I used was intermittent fasting which really accelerated my fat loss. For more details on what I’ve learned about intermittent fasting click HERE.

The quote below is simple yet powerful. It helps me remember failure only happens once we give up entirely.

“You never fail until you stop trying”

Albert Einstein

If you are on your own journey of losing weight and becoming healthier remember I’m rooting for you!

Be flexible with your exercise – including when, where, and what type of exercise you do.

Remember the importance of finding healthy alternatives to unhealthy foods.

Focus on getting the RIGHT and BEST calories into your diet. They will give you more natural energy and help you feel fuller longer.

Start with small, achievable habits and work on being consistent most of the time with those habits.

Above all else love yourself and try to focus on the positives. 🙂

Disclaimer

The content on this blog includes our personal experiences and opinions in regard to pursuing a healthier lifestyle. We hope the information provides valuable insights to every reader but we are not health advisors. When making your health choices, we recommend researching multiple sources and/or receiving advice from a doctor or licensed health professional.

Back when my wife Shan and I were first married we both didn’t understand the importance of having an emergency fund. We actually had never even heard of the term!

This post may contain affiliate links, please see our disclaimer for details.

Later on, we were fortunate enough to learn from Dave Ramsey the importance of having an emergency fund. During times like the 2008 economic recession and COVID-19, many people lost their jobs and emergency savings would have helped lots of people in need.

CNCB states only 39% of Americans can afford an extra $1000 to put toward an unexpected purchase. If you haven’t already, it is a good time to put aside some extra money for these unexpected purchases.

An emergency fund isn’t just in case of losing a job but applies to other big and sudden things that happen in life.

For example, if your car engine breaks down or if there is a sudden home repair. An emergency fund gives us peace of mind.

Just imagine having enough money in a specific account for all types of emergencies.

What is an Emergency Fund?

An emergency fund is a separate savings account you’ve specifically set aside to cover or offset life’s unexpected events. Like a broken car, job loss, or sudden illness.

It shouldn’t be used to buy a new car, vacation, Christmas gifts, etc. Instead, the money in your emergency account should only be used for real unexpected emergencies. The cash is easy and quick to access and will cover the emergency cost.

Why Do You Need an Emergency Fund?

For us, the reasons for having an emergency fund are because unexpected emergencies always happen.

Having emergency savings can give us more peace of mind and the ability to deal with those unexpected emergencies. The money is also easy to access and is stable in a savings account.

How Much Should You Save in an Emergency Fund?

There are three different situations/categories:

Posses debt (expect house mortgage)

No debt

Retired folks

First, If you have debt (except house mortgage): we recommend first saving up $1000 in your emergency fund. Then we recommend using the debt snowball method to pay off all your debt except the mortgage.

If you fall in the second category, congrats!! Paying off all your debt except your house mortgage is a huge feat!

We highly recommend those in this category start saving a 3–6-month fully-funded emergency fund.

This means if you lose your job, you have a 3-6 month fully-funded emergency savings account to pay all of your bills and living expenses such as house mortgage payments, rent, food, etc.

We personally prefer having a 6-month fully-funded emergency account which gives us greater peace of mind.

If you’re trying to decide how much to save in your fully-funded emergency fund, there are several factors you should consider like job stability, any medical issues, or other factors.

If you fall into the third category, first off congrats!! We hope you are enjoying an amazing retirement life!

For those retired, having 2 years saved in an emergency savings account should be sufficient. Because when the next recession or stock market crash hits, there will be enough money in the account so that no money needs to be taken out of retirement investment accounts.

Instead, you will be able to wait until the stock market recovers.

Where to Put Your Emergency Fund?

We have an emergency fund and keep it separate from our regular checking and savings accounts. The emergency money is put into a high-yield savings account.

We recommend NOT putting your emergency fund into an investment account(s) since you will need quick access to the money.

When to Use The Money in Your Emergency Savings Account?

Don’t use the money in your emergency savings account to buy wants – that new TV can wait! 🙂

Instead, use emergency funds for a legit unexpected emergency. Job loss, broken A/C, etc.

As adults, we should all hopefully know what a real unexpected emergency is.

In Conclusion

In conclusion, taking the time to prepare and save up an emergency fund is really important.

Just imagine when losing your job or having the water heater go out, you will have enough cash to cover all those unexpected emergencies.

This feeling is unmatched and also really good for your mental health and relationships.

Start saving now even if it’s a little by little.

We currently transfer $400 a month to a High Yield Saving Account which is our designated emergency fund. We will keep transferring money until we hit our 6-month fully-funded goal!

We would love to hear your experiences when saving up for or using an emergency fund – feel free to drop a comment below!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.