This post may contain affiliate links; please see our disclaimer for details.

As with this image, you will need to tear back certain parts of your life or make changes to find Financial Freedom.

What does financial freedom mean to you? Is it being able to afford whatever you want without having to worry about money? Or is it something else entirely?

In reality, financial freedom is different for everyone. For some, it might mean living a comfortable life without any debt. For others, it might mean being able to retire early and travel the world.

The important thing is that financial freedom means something different to each individual and everyone can achieve it.

So, how do you go about achieving financial freedom? Read on to find out!

There are many different paths to financial freedom. Some people achieve it through hard work and disciplined saving, while others come into money through investing or inheritances. No matter how you reach financial freedom, the important thing is that you have a plan and you stick to it.

Can you achieve financial freedom?

The short answer is yes! Financial freedom is possible for almost everyone, no matter your current situation.

So whether you’re struggling to make ends meet or already comfortable, you can always make changes to improve your financial situation. It might not be easy, but it is possible.

The key to achieving financial freedom is to have a plan and to be disciplined. You need to know your goals and what you’re willing to sacrifice to reach them.

For some people, that might mean cutting back on unnecessary expenses and saving as much money as possible. For others, it might mean taking on additional work or investing in high-yield investments.

For us, the Biesingers, Financial Freedom is living on our terms. Having enough money in savings and investments that we can pivot or change what we do for work or stop working entirely. We believe that flexibility allows us more opportunities to feel peace and happiness.

Let’s turn our attention to how you can obtain financial independence:

Understand your current financial situation

When it comes to financial freedom, the first step is always the hardest. But the journey becomes much easier once you take that first step.

The first step is to take stock of your financial situation. This means listing all of your debts and savings.

Once you have a clear picture of what you owe and have saved up, you can develop a plan to pay off your debts and grow your savings.

One strategy for reducing debt is first to pay the debt with the highest interest rate or try the Debt Snowball Method. Another method for growing your savings is setting up automatic transfers from your checking account to your monthly savings account.

Have clear goals that you can achieve

The second step to achieving financial freedom is to set clear goals. This means knowing what you want to achieve and when you want to achieve it.

For example, do you want to be debt-free in five years? Do you want to retire at age 60?

Perhaps what you what to achieve is financial independence and retire early. Whatever your goals may be, make sure that they are realistic and that you have a plan for achieving them.

To help you understand how much you may need for retirement, you can check out our other blog posts about the 4% rule or the 25x rule.

Be disciplined with your spending

The third step to achieving financial freedom is to be disciplined with your spending. This means knowing what you can and cannot afford and sticking to a budget.

It can be challenging to stick to a budget, but it is possible.

Many helpful resources are available, such as online budget calculators and financial planning apps.

You can’t just be disciplined regarding spending; you need to track every cent you spend. This means knowing where your money is going and ensuring you are not spending more than you can afford.

You can’t get a good picture of your financial situation if you don’t know where your money is going.

Spend far less money than you earn

The goal is to spend far less than you earn to save as much money as possible. This can be difficult, but it is possible.

There are many ways to save money, such as couponing, setting a budget, and cooking at home.

You also need to ensure you are not spending money on unnecessary things. For example, don’t buy anything on credit that you don’t have to.

The interest on credit card debt can quickly add up and make it difficult to get out of debt.

Have an emergency fund

Life can always throw you a curveball, no matter how well you plan. That’s why it’s crucial to have an emergency fund to cover unexpected expenses. This fund should be used for medical bills, car repairs, or job loss.

Your emergency fund is there to protect you from financial ruin, so don’t dip into it unless it is necessary.

I created another article sharing on everything you need to know about Emergency Funds.

Invest in yourself to become financially independent

It can’t be stressed enough that you must invest in yourself if you want to become financially independent. You should consider investing in college or learning a trade to earn more money.

You’ll never succeed in becoming financially independent or retiring early if you don’t have a skill that enables you to earn more money than the average person.

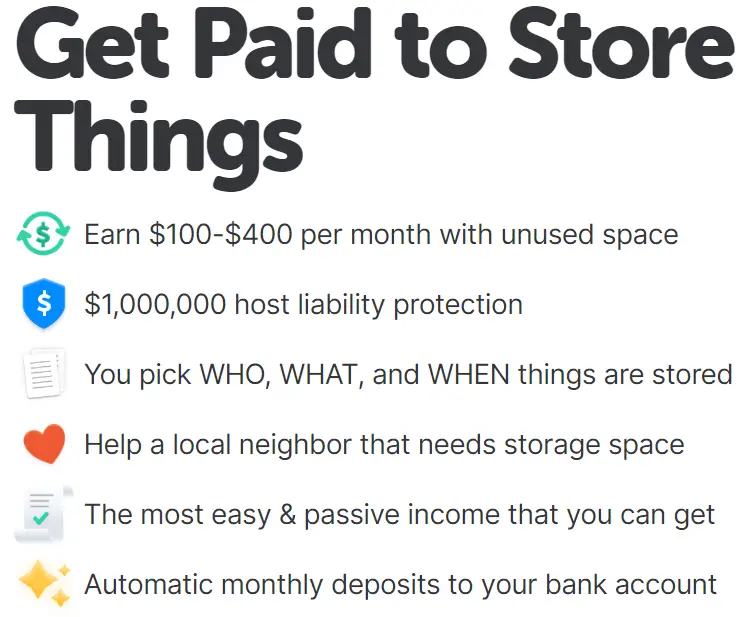

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

Start your own business

One of the best ways to achieve financial freedom is to start your own business. This can be a difficult and risky endeavor, but it can also be very rewarding.

When you own your own business, you control your financial destiny. This means you can earn a lot of money if your business succeeds.

Of course, starting your own business could be something you do on the side. It takes a lot of hard work, dedication, and some risk-taking. But if you are up for the challenge, it can be a great way to achieve financial freedom.

One of the most crucial steps: Paying off debt

Carrying around debt is like having a weight tied around your neck. It can be incredibly stressful and difficult to achieve your financial goals.

That’s why paying off your debt is one of the most important steps to becoming financially free.

There are a few different ways to pay off debt, such as using a debt consolidation loan or making extra payments on your debts.

Whichever method you choose, ensure you are dedicated to getting out of debt as quickly as possible.

Every person reading this can become financially independent

It’s true; every single person reading this can become financially independent. Of course, it will take work, dedication, and discipline, but it isn’t as complicated as you think.

If you are willing to put in the effort, you can achieve financial freedom. It is not an impossible dream; it is within your reach.

The difference between those who achieve financial independence and those who don’t is simply a matter of choice. You’ve got this; we’re rooting for you!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you have wondered what the term “lifestyle creep” means, you are not alone. This is a term that is often used but not always fully understood.

Lifestyle creep can be very dangerous for your finances and quickly lead to debt if not careful.

In this blog post, I will define lifestyle creep, discuss some warning signs, and provide some insights on how to avoid it.

This post may contain affiliate links; please see our disclaimer for details.

What is Lifestyle Creep?

Lifestyle creep is defined as “a gradual increase in spending that occurs when income increases or lifestyle changes.” It’s that tendency to spend more money as your income goes up. This can be a hazardous trap because it can quickly lead to debt.

It feels great to get a pay raise or bonus at work, but oftentimes it leads to more spending or even living outside of our means.

Let’s say someone starts with a salary of $40,000. After working very hard over the years with regular salary increases, and they are now making $70,000.

If not careful, too much money could be spent on wants such as clothes, eating out, or buying new things. Many of us enter this way of thinking and unfortunately end up in debt, regardless of having more income.

Rather than saving or investing the extra money, too many of us go out and spend it all, which can quickly lead to a worse financial position.

Another thing to keep in mind is to calculate your net income. A $2,000 raise will be taxed so it’s important to know exactly how much extra money you have each month and not miscalculate.

There are several warning signs that we should all keep in mind that can lead to lifestyle creep. If you notice any of the following, it may be time to reevaluate your spending habits.

Buying new clothes more often: If you find yourself shopping for new clothes more frequently, it may be a sign that you are spending too much money. Try sticking to a budget and only buying clothes when needed.

Eating out at restaurants more often: Going out to eat to celebrate your new raise once or twice is fine, but if you are doing it all the time, it may be a sign of lifestyle creep. Try to cook at home more often and only eat out on special occasions.

Taking more vacations: If you are planning more and more vacations, it may be a sign that you are spending too much money. Try to take one or two vacations per year and stick to a budget while you are on vacation.

Upgrading your car or home: This is commonly known as “keeping up with the Joneses.” Just because your neighbor gets a new car or house does not mean that you need to as well. It can be difficult at first, but resisting the urge to keep up with the people around you will provide you with many benefits.

Credit card debt is increasing: With a new raise, you may be tempted to use your credit card more often. However, this can lead to debt and financial problems down the road. Try to pay off credit card balances each month and only use it for emergencies.

No any extra funds to save or invest: After a raise, you should hopefully be able to save or invest at least some of the extra money. If not, it may be a sign that your spending is out of control. Try to automate your savings and investments so that you are not tempted to spend the extra money.

If you notice any of these signs, it is important to take action immediately. Lifestyle creep can quickly lead to debt and ruin your finances if you do not catch it early on.

How to Avoid Lifestyle Creep

If you believe you may have become a victim of lifestyle creep, don’t worry! There are ways to switch your spending habits and get back on track.

Here are a few tips:

Prioritize Your Money: This can be done in different ways. There is zero-based budgeting for example where you track every dollar coming in each month and every dollar spent.

No matter the method you choose, the goal of prioritizing your money is to control where it goes each month by sending your income to the most important categories first such as bills, savings, paying off debt, and investing.

A great way to create a budget without lifestyle creep is to use percentages rather than dollar amounts. As your income increases, your budget should automatically adjust without you needing to make any changes.

For example, if you want to save 20% of your monthly income, you would put $400 into savings if you make $2000 per month. If you get a raise and start making $3000 per month, you would then put $600 into savings.

The percentage-based budget saves you more money as your income increases automatically. Additionally, you don’t have to make any changes to your budget.

Save first, spend later: A great way to avoid lifestyle creep is to save your money and spend what is left over. Although this seems common sense, it can be easy to forget when you have extra money in your account.

Try setting up a direct deposit from your paycheck into your savings account. This way, you will never see the money and will be less tempted to spend it.

Invest in yourself: One of the best investments you can make is in yourself. Try to invest in your education or career to earn more money down the road. This will help you keep up with inflation and avoid lifestyle creep.

Be mindful of your spending: It is important to be aware of spending habits. If you are always buying new clothes or going out to eat, try to cut back in other areas.

There is nothing wrong with treating yourself occasionally, but let’s try not to get out of control here. 🙂

Talk to a financial advisor: A financial advisor can help you create a budget, save for retirement, and invest in yourself.

They can also help you stay on track if you have already started to creep into lifestyle inflation.

Live below your means: It is important to live below your means, even if you are making a good income. This means spending less than you earn and saving and investing the rest.

How to manage your money to live below your means can be daunting, but it doesn’t have to be. There are some simple rules that you can follow to help make managing your finances easier.

The method states that you should allocate 50% of your income toward essentials, 30% towards wants, and 20% towards savings.

Invest in cash-flow-producing assets before you buy liabilities: It is important to invest in assets that will produce income. This may include investing in real estate, stocks, or bonds.

Investing in these assets can create a passive income stream that can help cover your expenses.

For example, if you want to improve your lifestyle by subscribing to a $100 monthly gym membership, you should invest in assets that produce at least $100 per month. By doing you are improving your lifestyle without putting yourself at financial risk.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

Focus on improving your skills rather than acquiring stuff: One of the best ways to improve your lifestyle is to improve your skills. This may include taking free online courses, reading library books, or training to fit better.

Finding hobbies and passions that do not require much financial investment can help you live a better lifestyle without spending more money.

Don’t get too excited about promotions and stick to your financial plan: It can be easy to get caught up in the excitement of a promotion or raise. However, it is important to stick to your financial plan. Work on saving extra money that you make so you do not start lifestyle creep.

Lifestyle creep is a real problem, but it is possible to avoid it.

Following these tips, you can keep your finances on track and live a comfortable life without lifestyle creep.

The Bottom Line

If you are always living paycheck to paycheck, even after a raise, it may be time to look at your spending habits. Lifestyle creep can be a dangerous trap to fall into, but there are ways to avoid it.

Try to stick to a budget, save or invest your extra money, and resist the urge to keep up with the people around you. These simple steps can help you avoid lifestyle creep and keep your finances on track.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

I never imagined that a book could have such a profound impact on our lives. After reading Total Money Makeover by Dave Ramsey, I realized that I had been living beyond my means and was in debt up to my eyeballs.

The book taught me five important lessons that changed my thoughts about money.

In this article, we will discuss those five lessons in detail.

If you are struggling with your finances, then know these lessons could change your life too!

This post may contain affiliate links; please see our disclaimer for details.

Book Summary (Total Money Make Over – Dave Ramsey)

Ramsey’s book is based on the idea that ‘we must live like no one else now so that later we can live like no one else.’

In other words, we need to make sacrifices now to enjoy a comfortable retirement later.

The book covers various topics, such as how to get out of debt, save for emergencies and retirement, and invest wisely.

Ramsey also stresses the importance of giving back to charity.

What resonated with me were the five key lessons that he discusses in detail:

The first step to getting your finances in order is to create a budget. This may seem like a no-brainer, but you’d be surprised how few people do this.

A budget forces you to be mindful of your spending and helps you make better financial decisions.

Once the written budget is created, you can better understand where your money is going each month.

You may be surprised that you are spending more than you realized on unnecessary items.

Creating a budget is the first step to taking control of your finances.

It may not be the most exciting task, but it is necessary if you want to achieve financial success. He recommends including insurance for the following items in your written budget:

Auto and homeowner insurance

Life insurance

Long-term disability

Health insurance (If your nation/state does not provide this)

Long-term care insurance

Although adding insurance bills to your budget is never fun, they can save you a lot of money in the long run.

Items that can be removed from your budget are:

Cable TV

New cars

Eating out

Clothes shopping

Gym memberships

Latte factors (small, daily expenses that can add up)

These are just a few examples, but the point is that you need to be mindful of your spending.

Once you have a handle on your spending, you can start to make changes that will help you save money.

Lesson #2 – Create a Debt Snowball

I created a Debt Snowball by listing all my debts, regardless of interest rate, from smallest to largest.

Next, I made the minimum payments on all my debts except the one with the smallest balance. I paid as much as I could afford each month on that debt.

I was motivated to stay out of debt because I saw my balances going down each month.

This system also allowed me to pay off my debt faster because I put more money into the smaller debts first.

If you’re struggling with debt, I encourage you to try the Debt Snowball method. It works!

Starting with the highest interest rate could save more money in the long run, but psychologically, this method was the best for me, and we had low-interest rates.

3) Save for Retirement Now

Delayed gratification and thinking long-term are two important aspects of personal finance. Dave Ramsey famously said –

“Adults devise a plan and follow it, children do what feels good“.

Dave Ramsey

It’s never too early to start saving for retirement, and the sooner you start, the more time your money has to grow.

Ramsey suggests investing 15% of your household income into tax-advantaged accounts.

I knew retirement was in the cards but I realized I could start preparing better and preparing NOW.

We are maxing out our Roth IRA contributions each year, and I am on track to retire much sooner than I ever thought possible.

4) Pay Cash for Everything: Cash IS King

Spending with credit cards reduces the brain’s ability to feel pain.

When we make a purchase using cash, it feels much different than when we use a credit card. That’s because we physically see the money leaving our hands.

But when we use a credit card, it doesn’t feel like we’re spending real money. This can lead to overspending and accumulating debt.

It’s important to be mindful of your spending and only charge what you can afford to pay off each month.

You can earn slightly more money from credit card cash back, but it’s important to consider psychological factors. Credit card companies are very good at getting us to spend more money than we have.

It’s important to be aware of this and only use the credit card as a tool to build credit, not for shopping sprees.

Although the lessons taught in this book about credit cards are valuable, we’ve found that using a credit card wisely has many benefits.

Just be aware, do not overspend, and pay down credit cards on time – just our thoughts on this topic.

For most people, the mortgage is the biggest expense.

The author advocates for paying off your mortgage as quickly as possible so you can be debt-free and have more financial freedom.

There’s a saying that the grass feels different in your yard once you’ve paid off your mortgage because you fully own that land.

We, the Biesinger’s, personally feel investing at a young age is important, and real estate is generally increasing in value over the years. For these reasons, we have not started paying off our mortgage early yet, but it could be an option in the future.

Dave Ramsey’s lesson here is to take a zero-risk approach, but we want to have a small amount of risk to see more significant returns.

The choice is ultimately yours; paying off the mortgage provides peace of mind, but mathematically speaking, investing that money in the S&P 500 has more significant rewards.

You won’t be able to turn your financial life around overnight.

It took me years of bad spending habits to get into the mess I was in; my Wife and Dave Ramsey were able to help me correct those bad habits.

I could make significant changes in my financial life by taking small steps.

I started by reading this book and then implementing the lessons I learned.

Over time the steps brought me to accomplish my financial goals, even though they were small.

Try these baby steps from Dave Ramsey if you are struggling with finances. Like us, you can emphasize specific steps, such as getting out of debt but also focus on investing.

In Summary

This book is a great place to start if you want to pay off your debt or improve your financial situation.

It gave me a great personal finance perspective, and I’m sure it can do the same for you.

I recommend this book to anyone who wants to get their finances in order.

It’s an easy read and packed with valuable information to help you make better financial decisions.

If you’re looking for a personal finance book that will change your life, look no further than Total Money Make Over.

If finances overwhelm you, don’t worry because many people like me were in your shoes before reading this book.

The lessons I learned from Total Money MakeOver has helped me get my finances in order.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

When it comes to financial advice, there are few people as well-known as Dave Ramsey. His 7 Baby Steps have helped millions of people get their finances in order and achieve their goals.

But you may be asking yourself, does the program really work?

In this blog post, we will break down each step of the program and give you our opinion on whether or not it is effective.

We will also provide some tips on how you can follow the steps yourself and see results!

This post may contain affiliate links; please see our disclaimer for details.

Breaking Down the Dave Ramsey 7 Baby Steps

Dave Ramsey’s philosophy for personal finance is based on the idea that you shouldn’t take unnecessary risks with your money.

A simple and disciplined approach will set you up for success in the long run.

It is not the most exciting approach, but it has proven effective for many people.

However, it may not work for everyone. This is because mindset and behavior are key factors in financial success.

Some people don’t find any issue with a slow and methodical approach, while others crave the excitement of taking risks.

Dave Ramsey’s baby steps will work wonders for someone looking to settle down, raise kids and save for retirement.

Young entrepreneurs with ambitions that differ from these aspirations may find the program too restrictive.

It depends on your goals, lifestyle, and risk tolerance.

That said, Dave Ramsey’s baby steps include insightful wisdom about personal finance that anyone can benefit from.

Let’s explore each of his financial steps in more detail!

Baby Step 1: Save $1,000 to start an emergency fund

The first step is to save $1000 as quickly as possible.

This may seem like a lot, but it is important to have an emergency fund in case something unexpected comes up.

Once you have saved this money, you can move on to the next step.

Tips for this baby step:

Start by saving $50 from each weekly paycheck. This will get you to your goal of $1000 in 20 weeks.

If you get a bonus or tax refund, put it towards your emergency fund.

Cut back on expenses so that you can save more money each month.

Dave Ramsey recommends this because it will save you a lot of money in interest payments.

He also believes that your home should be paid off before you retire.

Having a place where you can live rent-free can be a huge financial burden lifted off your shoulders in retirement.

It can free up cash flow for other things, like travel or hobbies.

Tips for this baby step:

Make extra payments each month.

Refinance to a shorter loan term.

Apply any windfalls towards your mortgage balance.

Baby Step 7: Build Wealth and Give (Like No One Else!)

Dave Ramsey recommends that you invest in mutual funds.

He also believes that you should give generously to charities and other causes that are important to you.

His belief on wealth is that it should be used to bless others and not just for your personal gain.

Dave Ramsey is not a fan of gambling or higher-risk investments. This is because he has seen too many people lose their hard-earned money in these types of investments.

Tips for this baby step:

Invest in a mix of different mutual funds to help minimize risk.

Save automatically each month with a dollar-cost-average strategy.

Give generously to charities and other causes that are important to you.

Do the Baby Steps Really Work?

Ramsey’s baby steps have helped people across the globe get out of debt and live better lives.

Although we do not follow all of his steps, we feel most of his teachings are on the right track, especially for those looking to gain control over money and avoid risk.

Having an emergency fund has provided us with profound peace of mind. The debt snowball helped me pay off 56K in student debt!

Using cash to buy reliable second-hand cars has been a great benefit to us as well.

We have also opened up education savings accounts for both of our kiddos.

We follow most of Dave’s teaching but with a few key differences.

We believe that you should start saving for retirement as early as possible.

The earlier you start, the more compounding interest will work in your favor, even if it’s just a little each month.

We agree that consumer debt should be paid off aggressively. However, not all debt is bad debt.

Debt can be a wise investment decision and can be used to purchase assets, such as real estate or a business.

We currently have one rental property and see it as a valuable asset where the reward outweighs the risk.

Using credit cards to build credit has been a great tool for us, but they must be used very carefully.

Step 5 is also not applicable to everyone as some people prefer not to have children or cannot have children. In this scenario, people can still benefit from following the other steps.

All in all, we think that Dave Ramsey’s baby steps are a great starting point for anyone looking to get out of debt and improve their financial situation.

However, it is important to take into account your personal circumstances when following his advice.

Some people believe that Dave Ramsey’s advice is too ‘old school’ and that he is too rigid with his approach.

Critics believe that he needs to get caught up with the new realities of finances. However, it is difficult to deny the timeless wisdom he teaches.

It clearly applies to money management, no matter what the current economic conditions may be.

Dave Ramsey Baby Steps: Conclusion

Whether you agree with him or not, Dave Ramsey’s baby steps have helped millions of people get out of debt and improve their financial situation.

For that, we believe that he is worth considering if you are looking for advice on getting your finances in order.

Dave Ramsey seems like a genuine person and really does take plenty of time to help people.

He is America’s favorite financial coach, and for good reason.

Ramsey provides practical solutions that have helped millions get out of debt and improve their lives.

Although we do not agree 100% with his exact steps, his teachings are fundamental and can undoubtedly be a saving grace for many people, including us.

We hope this has helped clear some things up for you if you are wondering whether Dave Ramsey’s baby steps actually work.

Do your own research and be sure to carefully consider your personal circumstances before making any financial decisions.

If you are considering using Ramsey’s baby steps to help you get out of debt, we suggest you speak with a financial advisor to see if it is the best action for your unique situation.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Sometimes it can be hard to know the best place to start spending your tax refund wisely.

Most of the time, the first place we want to spend our money is at the stores. We purchase new clothes, electronics, shoes, and probably more products than we need.

Getting caught up in the hustle and bustle of looking cool is easy. Many try keeping up with the Joneses down the street; however, there are much wiser places to put your money that can help your financial goals.

So let’s explore 9 smart ways to spend your upcoming tax refund money to set you up for a better future!

1. Pay Off Your Debt

We know this is not the most glamorous or fun way to spend your money but paying off debt has many benefits.

With a little extra money in your pocket, it’s the perfect time to lessen the stress of those bills.

Almost every adult has some student loans, house bills, or credit card debt that needs to be paid. Tax refund money can help to help ease this burden.

Student Loans: Right now, almost one-third of American students will owe something in student debt, and the average student loan debt in 2020 was over $38,500 per person. These numbers are staggering and only expected to increase. Another crazy statistic about student loans is that about 9% of people who have student loans are falling behind on their payments.

Mortgage: According to the Federal Reserve Bank of New York, mortgage debt has risen to over $10 trillion by the fourth financial quarter of 2020. This has been increasing dramatically since the peak in 2008. If you are a home-owning adult with a mortgage, it may be a good idea to start decreasing your debt with a jump-start from your tax refund.

Credit Card Debit: Unfortunately, many struggle to break free of credit card debt worldwide. In the last quarter of 2021, the credit card balance was at a staggering $860 billion. These numbers are far from the number reached during the 2008 financial crisis. With your tax refund, it is time to start chipping away at your credit card debt and building your financial portfolio.

We can never anticipate every twist life throws at us. What if your car doesn’t start one morning, or if the pipes burst in your house while you were on a trip, and your home insurance doesn’t cover flood damage?

These are real problems we can run into, and if you don’t have a little extra money put aside, you may be adding more to your credit card debt or would have to take out a personal loan.

CNCB says that only 39% of Americans can afford an extra $1000 toward an unexpected purchase.

If you haven’t already, it is a good time to put aside some extra money for these unexpected purchases.

As a rule of thumb, some people like to have enough money in an emergency fund to cover anywhere from three to six months of expenses.

Let’s say you got laid off and didn’t have enough to cover the bills. This would be stressful for anyone, but having an emergency fund provides peace of mind.

It is time to ease your worries and start saving for these mishaps by creating an emergency fund.

3. Add to Your Retirement Account

You have likely said, or a coworker has said: “can I retire yet?” Retirement and even early retirement (and maybe having a house on the beach) are what most people are striving to achieve.

Using your tax refund money to add to your 401K, Roth IRA, or Traditional IRA is a smart way to spend that money.

If you haven’t set up a brokerage account to invest in a retirement fund, this is a great time to start, so you aren’t working until you are 80.

By setting up a brokerage account, you are building your way toward financial freedom. If you dedicate all or some of your tax refund every year to your retirement fund, you will be in a great spot by the time you are ready for that phase of your life.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

Although all of the following are fun, by reinvesting in yourself, I don’t mean buying a luxury car, having a spa day, or going on a shopping spree.

If you want to take a budgeting course or purchase some new self-help books, using your tax refund would be a great way to use that money.

We rarely have money fall in our laps, so when we have some (like after tax season), it can be nice to use it to improve ourselves.

One way to better reinvest is to take a course on something that will earn you more money. There are countless courses on becoming successful at affiliated marketing, writing, investing, real estate, or other ways to make passive income.

Investing in yourself is a smart move when it comes to your tax refund.

5. Home Renovation

Have you been putting off upgrading your kitchen or getting new floors for the bathroom?

Home renovations are a common expense, but with the help of your tax refund, it might be a wise place to use your money.

If there are “absolutes” when it comes to your home for home renovations (i.e., you NEED a new water heater, or your washer is held together with duct tape), that is probably where you should spend your money first; however, there are other options that can save you big down the road.

Here are some home improvements to consider that can save you money in the long run:

Switching to low-flow toilets and showerheads: This can help to reduce the cost of water.

Upgraded security system: If you have an outdated security system yet more valuables in your house, it might be a wise choice to update that to protect your valuables when you are away.

Shifting to LED light bulbs: These light bulbs can help you to save money on your next energy bill

Using your tax refund money to upgrade your house and add value is an excellent way to get the most out of your money!

Before renting our second property, we painted all cabinets white (see picture below). This did not cost much money and helped make the place look a lot nicer / added value. 🙂

Are you new to the world of investing? It can be overwhelming to try and follow the stock market and know what purchases to make.

However, if this is something you have always been interested in and want to try, using your tax refund money is a good start (that way, if you make a wrong decision, you aren’t using your life savings).

A safe place to start when it comes to the stock market is the S&P 500. The S&P 500 (Standard & Poor’s 500) is an index that tracks the most notable 500 companies in the U.S. These companies have some of the greatest impacts on the economy.

By investing in the S&P 500, you own a small portion of those 500 publicly traded companies. If you are new to investing, this is safer for your money than purchasing individual stocks.

With individual stocks, you risk losing all the money you put into that company going bankrupt.

If you have been dying to dip your toes into investing, why not start this year with some of your tax refunds?

7. Jump Start Your Business

You have a little extra money and a great idea. Why not leap and start your business?

You can use the money to hire a website creator or buy the necessary supplies. You can also file for an LLC with the money.

Investing your money into creating a business can help bring you financial freedom and allow you to have more money in the future. Take this as a sign to jump-start your business with your tax refund money.

8. Travel

Although this may sound like a way of wasting your money, hear us out because we don’t mean drinking endless margaritas on a beach (even as tempting as that sounds).

Taking a vacation to clear your mind, discover your passions, and learn about a new culture is not wasted.

Traveling allows you the opportunity to explore our world and all its uniqueness with it. You could also travel to do volunteer work.

If you have always wanted to volunteer abroad, you could use some of your tax refund to finally do it. There are plenty of affordable programs that do 1–2-week volunteering opportunities.

Traveling can also be good because it gives you experiences that can give you an edge.

Many companies ask about your experiences with diversity or what diversity means to you in an interview.

If you have traveled and have experiences with new cultures, you have a great answer to those types of questions because you have had that experience.

Spending your tax refund money on a new and exciting adventure could be a wise decision that can benefit you for years.

If you have never heard of a 529 plan, don’t worry because you aren’t alone.

A 529 plan (also known as a qualified tuition plan) is a way to save money for possible future educational costs for your children.

To be a little more specific, according to the U.S. Securities and Exchange Commission, the 529 plan is a “tax-advantaged savings plan designed to encourage savings for future educational costs.”

The two types of plans are prepaid tuition and education savings plans.

Prepaid plans allow the saver (you) to buy credits, at the current price, to a university for your child. Prepaid plans are typically only for tuition and fees and do not help cover room and board.

The biggest advantage to a prepaid plan is it allows you to pay at today’s prices versus the future prices of college.

Education savings plans allow the saver to open an investment account to save for all higher education costs, including room and board.

These plans are known to be a bit riskier depending on how you invest your money. They also are not as protected by the state as many prepaid plans.

It is important to do your homework regarding the best option for you and your family when it comes to opening and investing in a 529 plan; however, if you know your kids have dreams of going to college, this may be a smart option for you when it comes to your tax refund this year.

In Conclusion

There are a variety of smart ways you can spend your tax refund money. We want you to make the best decisions for yourself with your money.

Whether saving for retirement or paying off your debt, you will set yourself up for a better financial future!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.