Generally speaking, there are two main types of FIRE: Fat FIRE, and Lean Fire.

Fat FIRE is focused on saving enough money so that you can retire early and still maintain your current lifestyle.

This requires a higher savings rate than lean FIRE, but it allows you to enjoy your life while still working towards your financial goals.

Strategies for achieving Fat FIRE:

Strive For Higher Income – One strategy is to work towards a high salary. This means finding a career that you’re passionate about and making the most of your earning potential.

You can also look for ways to make extra income so that you can boost your investing rate.

Diverse Income Sources – Another strategy is to focus on building up your passive income streams.

Some ways you could do this is by investing in rental properties, dividend stocks, or peer-to-peer lending.

The more sources of income you have, the easier it will be to reach your financial goals.

Invest Your Money Wisely – Once you have saved up enough money, you will need to invest it wisely in order to achieve your financial goals.

This can be done by diversifying your investments and making sure that you are invested in a variety of different asset classes.

Create Multiple Streams of Income – Another way to achieve Fat FIRE is by creating multiple streams of income. You could invest in real estate or start a side business. By having multiple sources of income, you will be able to reach your financial goals sooner.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

This type of FIRE is helpful for people that want to retire early but don’t want to make major lifestyle changes. It can take longer to achieve Fat FIRE, but it may be more sustainable in the long term.

Lean Fire is focused on saving enough money so that you can retire early and live a frugal lifestyle. This type of FIRE is similar to Fat FIRE, but it does require you to make a few more sacrifices.

Strategies for achieving lean FIRE:

Save as much money as possible – You will need to save a large percentage of your income in order to achieve Fat FIRE. This can be done by living a frugal lifestyle and making sacrifices in order to increase your savings rate.

Live Below Your Means – One of the most important things to do when trying to achieve lean fire is to live below your means. This means being mindful of your spending and only buying what you need. It also means being willing to make sacrifices in order to save more money.

Reduce Expenses – Another way to achieve lean fire is by reducing your expenses. This can be done by cutting back on unnecessary luxuries and finding ways to save money on your essential expenses.

There are a number of different strategies that you can use to achieve lean fire. The most important thing is to find what works for you and stick with it. If you’re disciplined and patient, you can achieve your goal of retiring early.

Lean Fire is a good option for people that want to retire early and do not need luxury experiences or high-ticket products.

It can take less time to achieve Lean Fire, but it can also be less sustainable in the long term.

How to use the FIRE method to retire early?

If you want to achieve FIRE, there are a few things you need to do:

First, you need to figure out how much money you need to retire.

The amount needed will be different for everyone depending on their lifestyle and retirement goals.

Once you have this number, you need to start saving and investing!

The earlier you start, the easier it will be to reach your goal.

One of the best ways to save money is to invest in yourself.

You can invest your time to learn about personal finance and investing. The more you know about these topics, the better equipped you’ll be to make smart decisions with your money.

As mentioned earlier, another way to reach your FIRE goals is to live below your means.

Often jealousy or insecurities prevent people from doing this, but it’s one of the smartest things you can do for your finances.

When you live below your means, you have more money to save and invest.

When you have these metrics figured out, it’s time to increase your income.

You can also invest in assets that produce passive cash flow.

To improve your income, try learning about negotiating if you are employed and sales skills if you are self-employed.

By improving your earned income, you can save more money each month to reach your FIRE goals.

Some passive income-producing assets are real estate, index funds, and dividends stocks. You can also create cash flow by starting a business, starting a blog or writing an e-book.

Once your passive income is above your expenses, you can officially state that you have achieved FIRE. This is because you’re free to spend your time as you’d like.

Your assets pay for your liabilities and you will no longer have to work for money.

However, just because you don’t have to work for money, doesn’t mean you can’t still earn some.

For example, if you enjoy writing, you can work as much as you’d like as a freelancer.

You will still be generating an income, but you’ll be doing it on your own time.

Of course, you could also just spend your time relaxing and enjoying your newfound freedom.

Having delayed gratification is also important when attempting to achieve FIRE.

You need to be ready to sacrifice current consumption for the chance to retire early.

You need to have a plan and be patient in order to achieve your FIRE goals. If you continue to spend on the latest sales and new releases, you will be stuck in a cycle of working to pay for your expenses.

Instead, try investing in assets and reinvesting the cash flow from those assets. This can really begin to snowball and help you reach FIRE much sooner than if you just continued working and spending as usual.

Limiting liabilities can also help you achieve FIRE. A liability is something that costs you money each month, such as a car payment or credit card debt.

If you can pay off your liabilities and live without them, you’ll be one step closer to Financial Independence and retiring early.

Another way to achieve FIRE is by finding creative ways to save money. This could include things like couponing, living in a van or RV, or house hacking.

By finding creative ways to save money, you’ll have more money to invest and reach your FIRE goals faster.

The last thing you need to do is have patience and discipline. Retiring early doesn’t happen overnight.

It takes time, effort, and sacrifice. But if you’re willing to put in the work, FIRE is attainable.

By developing systems and having a long-time horizon, you can achieve your goal of retiring early and enjoy a life of financial freedom.

If you’re willing to make some sacrifices and put in the work, you can achieve FIRE.

It might take some time, but it will be worth it when you reach your goal and can enjoy a life of financial freedom.

The Bottom Line

So there you have it!

These are just a few tips on how to retire early using the FIRE method.

By exercising patience, discipline, and being willing to make sacrifices, you can achieve your goal of financial independence!

Start planning and saving today so that you can enjoy a stress-free

When pursuing FIRE, remember the different types and see which one works best for you.

Lean FIRE can be quicker to achieve but does not leave you much room for luxury expenses. If you are minimalistic, this can be a great option for you.

If you want to have a little more wiggle room in your budget, try Fat FIRE. This will take longer to achieve but will give you more breathing room in your budget.

Whatever route you decide to take, remember that FIRE is attainable for anyone willing to put in the work.

The bottom line is that FIRE is a great way to achieve financial independence and retire early.

So what are you waiting for?

Start planning your FIRE today!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

There are also many paths to FIRE, and that’s a good thing! By reading this article, you too may find a type of FIRE strategy suitable for your life and circumstances.

So, what are the different types of FIRE? Let’s take a closer look.

This post may contain affiliate links; please see our disclaimer for details.

Traditional FIRE / Regular FIRE

The traditional FIRE movement is about saving as much money as possible and investing it in a diversified portfolio of stocks and bonds. The goal is to reach a point where your investment or nest egg returns are enough to cover your living expenses, so you can “retire” from paid work (although you may still choose to work part-time or volunteer).

This approach is often called the “4% rule” because it’s based on the idea that you can safely withdraw 4% of your portfolio each year, adjusted for inflation.

So, if you have a $1 million portfolio, you could theoretically withdraw $40,000 per year ($1 million x 0.04) and never run out of money.

Of course, there’s no guarantee that the markets will always cooperate, and you may have to adjust your spending if there’s a major market downturn. But over the long run, this approach is quite successful.

The best thing about traditional FIRE is that it’s relatively simple to understand and implement. And, if you start early enough, you can reach this type of FIRE with a fairly modest savings rate.

Lean FIRE is similar to traditional FIRE but with a twist. The goal is still to save as much money as possible and invest it in a diversified portfolio. But instead of aiming for the same amount of expenses, the goal is to retire with a lower lifestyle than you have today.

This could mean retiring to a smaller house, driving an older car, or giving up some of your hobbies and travel. The idea is to reduce your costs to reach FIRE with a smaller nest egg.

Lean FIRE is an excellent option for people willing to make some lifestyle changes to retire early. And it can also be a good choice for people who are risk-averse and don’t want to rely entirely on investment returns to fund their retirement.

Fat FIRE

Fat FIRE is the opposite of Lean FIRE. Instead of retiring on a leaner lifestyle, the goal is to retire with the same (or even a better) lifestyle as you have today. To do this, you’ll need to save a lot of money and invest it in a way that generates high returns. This could mean investing in growth stocks, real estate, or other assets that can generate a high return on investment.

Fat FIRE is a good option for people willing to take on more risk to retire with a better lifestyle. It’s also a good choice for people who want the flexibility to retire early and then go back to work if they want to.

Let’s be honest the average person isn’t going to be able to save enough to retire on a fat FIRE lifestyle. But, if you have a high income and are willing to take a few gambles, it’s possible.

Obese FIRE

Obese FIRE is similar to Fat FIRE, but with one key difference. Instead of retiring with the same lifestyle as today, the goal is to retire with an even better lifestyle.

Some of you might be thinking, “Isn’t that just called rich?” And, well, yes. But the term “Obese FIRE” is usually used to describe people who are retiring with a lifestyle that is far above their current lifestyle.

This could mean retiring to a private island, buying a yacht, or just living in a mansion. But, basically, it’s any lifestyle that most people would consider to be unobtainable.

Obese FIRE is only an option for a very small number of people. But if you have the income and the investment returns to make it happen, more power to you!

Everyone dreams of retiring early and living a life of luxury. It may be your goal; however, it’s essential to know that if it isn’t your reality, that’s okay too!

It’s perfectly fine to live your life in the clouds as long as your feet are firmly placed in reality. So, if you’re planning to achieve obese FIRE, make sure you have a solid plan in place and that you’re prepared for the possibility that it may not work out.

Coast FIRE

Coast FIRE is a strategy for financial independence that involves saving as much money as possible over a short amount of years, then living off the interest once you reach your goal. With Coast FIRE, you save until you reach a predetermined amount by a specific age, at which point you stop saving and let compound interest “coast” you to your desired retirement nest pile.

You could quit your preparatory work and instead take on a part-time job or establish passive income streams to live off of after reaching your financial independence goal, perhaps 80% there. This would allow you to meet life’s essential expenses.

Coast FIRE is a great way to get off to a fast start with active saving and investing, and it can help you achieve financial independence sooner than you might think.

Flamingo FIRE is a new concept that is quickly gaining popularity. The name comes from the Money Flamingo blog, which discusses various ways to achieve financial independence.

Flamingo FIRE refers to the three stages of retirement: semi-retirement, early retirement, and standard retirement. In the first stage, you work full-time to develop a nest egg by saving and investing.

You enter semi-retirement when you reach half of your FIRE number. During those ten years, you don’t need to invest. You can retire if it doubles in 10 years. After that, you can work part-time or a less-paying job that makes you happy till then. Twenty-five times your estimated living expenditures is full FIRE, stage 3. This final stage is when you are truly retired and no longer working.

The Flamingo FIRE concept is an innovative way to think about retirement. It could be an excellent option for those looking for an alternative to the traditional retirement plan.

Barista FIRE

Barista FIRE is where you’re working part-time to pay for healthcare and whatever costs you encounter. For many people, healthcare is their largest expense in retirement.

Paying for healthcare is one of the biggest financial challenges that Americans face. In fact, healthcare costs are one of the main reasons why people say they can’t afford to retire.

One way to pay for healthcare in retirement is to work part-time. This is what’s known as Barista FIRE.

With Barista FIRE, you’re working part-time to cover your healthcare costs. Once your healthcare costs are covered, you can use the money you’re saving to retire early.

This strategy is becoming more popular as healthcare costs continue to rise. It’s a great way to ensure you have the coverage you need while also giving you the freedom to retire early.

Slow FIRE

Slow FIRE is where you’re working towards financial independence, but you’re not in a hurry to retire. The goal is to reach financial independence, but you’re not in a hurry to quit your job.

It’s a good option for people who want to achieve financial independence but don’t want to retire immediately. It’s also a good option for risk-averse people who want to take a slow and steady approach.

The key to making Slow FIRE work is to find a balance between saving for retirement and enjoying your life. You don’t want to sacrifice your lifestyle today in order to retire tomorrow.

But, if you can find a balance, Slow FIRE can be a great way to achieve financial independence and retire on your own terms.

Fart FIRE (or Fast FIRE)

Fart FIRE is where you’re working towards financial independence, but you’re in a hurry to retire. The goal is to reach financial independence as quickly as possible, so you can quit your job and enjoy your retirement.

If you’re the type who loves to throw caution to the wind, Fart FIRE may be the right approach for you. It’s risky, but it can also be very rewarding.

The key to making Fart FIRE work is having a solid plan. You need to know how much you need to save and how you will invest your money.

You also need to be comfortable with the idea of retiring early. If you’re not ready to retire, Fart FIRE may not be the right approach.

It’s important to remember that when you’re trying to speed up the FIRE process, it’s possible to make mistakes. If you’re not careful, you could end up losing everything you’ve worked so hard for.

So, if you’re going for Fart FIRE, make sure you know what you’re doing.

Which type of FIRE is right for you?

Well, the first thing to do is accept that FIRE is a spectrum. There’s no right or wrong answer. You need to find the best approach for you and your family.

If you’re not sure which approach is right for you, ask yourself the following questions:

What are your goals?

How much risk are you willing to take?

How much time do you have to save?

What’s your lifestyle like?

Do you want to retire early or on your own terms?

Once you answer these questions, you should have a good idea of which type of FIRE is right for you.

If you want to retire early, you’ll need to save more money and take on more risks. If you’re not willing to take on as much risk, you’ll need to save more money and plan for a longer retirement.

It’s important to remember that there’s no one-size-fits-all approach to FIRE. You need to find the approach that works best for you and your family.

Conclusion

Almost all of you reading this will want to go the route of traditional FIRE. It makes sense because it’s the most logical and gives you the most control. You can always adjust your lifestyle later on down the road if you want to, but it’s much harder to do the reverse.

Remember, you don’t have to choose just one type of FIRE. You can use a combination of different types of FIRE to achieve your financial goals.

For example, you could use a mix of traditional and barista FIRE to achieve your financial goals. It all depends on your health, age, and desired lifestyle. Whatever type of FIRE you choose, the important thing is to start working towards your financial goals today. The sooner you start, the sooner you’ll be able to retire on your own terms.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Anyone seeking financial freedom to retire early or FIRE knows that many options exist to save and invest money. Today I’m excited to share with you 16 ways to help you reach FIRE faster!

The question is, what’s the best way to go about it? The problem is that there’s no one-size-fits-all answer, as the best method depends on each person’s unique circumstances.

That said, there are still some critical steps that can help anyone on the path to FIRE.

This post may contain affiliate links; please see our disclaimer for details.

1. Decide how early you want to retire

At what age do you want to be financially independent? Are you talking about retiring at 40 or maybe 60? The answer to this question will play a big role in determining how much you need to save and invest.

This is the first question you must ask yourself, as it will shape the rest of your FIRE journey.

There are different ways to calculate how much you will need for retirement. You can check out the other articles I’ve written describing the 4% rule and the 25x rule when considering retirement.

2. Take into account your cash flow and how much you owe

Cash Flow is Key

FIRE isn’t just about saving money – it’s also about ensuring your cash flow is positive. That means you need to consider how much you earn, how much you spend, and how much debt you have.

For example, if you’re earning a high salary but have a lot of debt, it will take longer to reach financial independence. The problem with debt is that it can be like a weight around your neck, dragging you down and preventing you from making progress.

Once you have a handle on your cash flow and debt situation, it’s time to start thinking about investing. Investing allows your money to work for you and grow over time.

There are many different options, so it’s important to research and find the right ones.

If you’re young, don’t be afraid to take some calculated risks. My wife and I purchased our first real estate property in our early 20s while still attending college. We learned many valuable lessons and were able to later turn it into an investment property that brought in passive income.

You might want to focus on more stable investments if you’re older. Adjust your investment strategy to your age and willingness to take on risk.

4. Automate your finances

One of the best things you can do to reach FIRE faster is to automate your finances. Set up automatic transfers from your paycheck into your savings and investment accounts.

This will help you make headway on your goals without even thinking about it. Automation is key to achieving financial independence because it takes the emotion out of decision-making.

You also want to ensure that you automatically invest your money in the right places. You can do this by using a service like Betterment or Wealthfront.

5. Live below your means

One of the most important things to remember to make the path to FIRE faster is that you must live way below your means. This doesn’t mean that you have to live like a monk – but it does mean that you need to be mindful of your spending.

Seriously consider your every purchase and ask yourself if it’s something that you need. A lot of people find that they can save a ton of money just by making small changes to their spending habits.

If you don’t need it, don’t buy it. Of course, that’s easier said than done if you have kids or other financial responsibilities, but it’s still something to keep in mind.

How is this different than living below your means?

Well, living below your means is more of a general principle. Keeping your expenses low is specifically about finding ways to reduce the amount of money you spend each month.

There are many ways to do this, but one of the most popular is downsizing your home. Moving into a smaller house or apartment can save you a ton of money monthly on rent or mortgage payments, utilities, and more.

7. Make extra money

Of course, saving money isn’t the only way to reach FIRE faster. You can also make extra money to help you reach your goals faster.

There are many different ways to do this, but one popular option is to start a side hustle. This could be anything from driving for Uber to starting a blog to selling products on Etsy.

The key is finding something you’re passionate about and can do in your spare time. Making a few extra hundred dollars each month can significantly affect how long you reach FIRE.

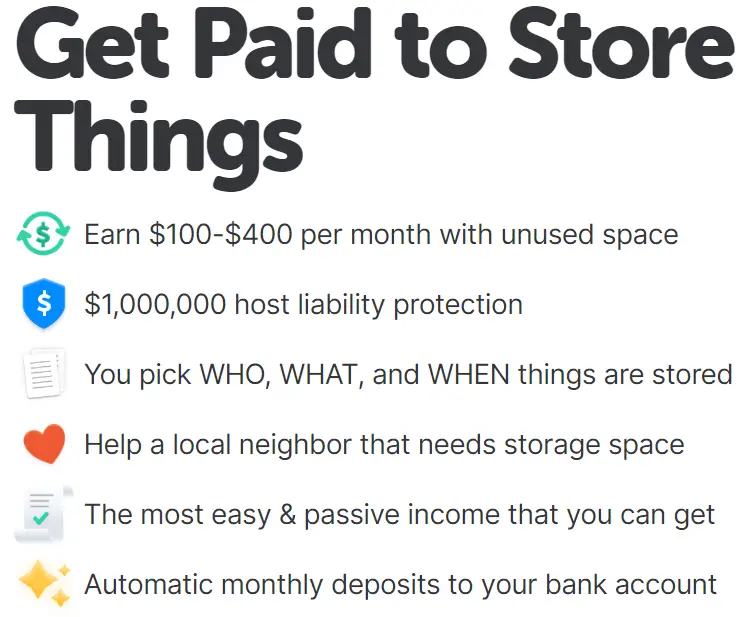

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

8. Go back to school and further your education

No matter where you are in life, there’s always room for further education. Returning to school or picking up a new skill can help you get a better job and make more money.

This doesn’t mean that you need to get a Ph.D. – but taking some classes or getting a certification in something can really pay off.

The goal is to make yourself more marketable and increase your earnings potential. If you can do that, you’ll be well on your way to reaching FIRE faster.

You need to make yourself irresistible to potential employers. Plus, your current job might pay you more if you have more education.

9. Get rid of your debt

To retire early, you must get rid of your debt. We’re talking every last penny – credit cards, student loans, mortgages, car payments, everything.

The reason for this is twofold. First, debt is a massive weight around your neck. It’s emotionally and psychologically draining.

Second, debt costs you money. The interest payments on your debt could go toward your retirement.

The more money you spend on interest, the longer it will take you to reach FIRE. So, if you’re serious about retiring early, you need to get rid of your debt and begin living a debt-free life.

You can always try out the debt snowball method. We used this debt payoff strategy to repay 56,000 in student loans quickly.

10. Put as much money as you can in your retirement accounts

Of course, you want to do this after paying off your debts!

There are tax benefits to doing this, which we’ll discuss briefly. But the most important thing is that you’re putting your money towards your future.

The more money you can put into your retirement accounts, the better. This will ensure you have enough money to live comfortably when you retire.

The best retirement accounts are 401(k)s and IRAs. If you can, you should max out your contributions to both of these every year.

By maxing out your 401(k), you’re putting $18,000 away each year. And if you have a company match, that’s even more money you’re getting for free.

With an IRA, you can contribute $5,500 each year. And if you’re over 50, you can contribute an extra $1,000.

If you can swing it, maxing out these accounts each year is a great way to reach FIRE faster.

11. Reduce your tax burden as much as possible

You’ll need to hire a good accountant to do this. But there are a lot of different ways to reduce your tax burden.

This could be anything from taking advantage of tax breaks, setting up a home office, and deducting your business expenses.

The goal is to keep as much of your money as possible and to have less of it go towards taxes. The less you’re paying in taxes, the more money you’ll have to save for retirement.

You don’t want to cheat on your taxes, of course. But there are legal ways to reduce your tax burden. And you should take advantage of them if you can.

If you do your taxes, ensure you take advantage of all the deductions and credits you’re entitled to.

12. Consider relocating to a cheaper area

This isn’t for everyone. But if you’re serious about retiring early, you might want to consider relocating to a cheaper area.

Moving to a cheaper area will reduce your cost of living and free up more money that you can put toward retirement. We’re talking about lower mortgage payments, cheaper groceries, and lower utility bills.

If you work remotely, this is an especially good option. You can live anywhere in the world and still work from your laptop. The only downside is that you might have to say goodbye to your current lifestyle and social circle.

13. Take good care of your health

Your health is one of your most important assets. The healthier you are, the less money you’ll have to spend on medical bills.

You’ll earn more money now if you’re healthy and can work longer hours. And you’ll have more money in retirement if you don’t need to spend it on medical bills.

If you can be healthy when you’re young, you’ll be more likely to stay healthy in retirement. So, take good care of your health now, and you’ll reap the rewards later.

You’ll also save money once you retire if you’re in good health. That’s because you won’t need to buy as much insurance.

14. Invest every cent that you don’t spend

Any money left over at the end of each month should be invested. Let’s say that you budget yourself $300 a month for entertainment.

But at the end of the month, you only spent $200 on entertainment. That extra $100 should be invested. You might think the $100 is meaningless, and you can let it sit in your checking account.

But that’s not true. That $100 can grow into a lot of money if you invest it. Toss that $100 in a rising tech stock and let it sit for a few years. You’ll probably get a better return on your investment than letting the money sit in your savings account.

One way you can increase your savings and investments is by mico-investing.

ACORNS is a popular platform that can round up money from purchases and automatically allocate those funds to diversified investments.

If you’re unhappy with how things are going, don’t be afraid to make changes. That’s true in both your personal life and your financial life.

If you don’t like your job, quit and find something else. End it if you’re in a relationship that’s not working out.

If you’re not happy with your current financial situation, make changes. That could mean getting a better-paying job, finding a cheaper place to live, or investing more money.

Whatever it is, don’t be afraid to make changes. Life is too short to be unhappy. And you’re in control of your own happiness.

Although easier said than done, you can start making baby steps today toward meaningful change.

16. Don’t let your emotions get the best of you

Your emotions can lead you astray, especially when it comes to money.

Don’t make financial decisions based on your emotions. That’s a surefire way to lose money.

For example, don’t sell all of your stocks when the market is crashing. And don’t buy stocks just because everyone else is buying them.

Investing is a long-term game. You need to take a long-term view if you want to be successful.

You’ve Got This!

So, by now you should know how to retire early. It’s not easy, but it’s possible. You need to be disciplined with your money and make smart financial decisions. Try focusing on one or a few tips in this article to help you reach FIRE faster.

You begin by assessing your current financial situation and setting some goals. Then you need to create a budget and start investing your money.

You should also make sure that you’re taking good care of your health. That way, you can stay healthy and work harder. The harder you work now, the faster you’ll get to enjoy FIRE.

Please comment below with ways you’ve been able to gain control over your finances and speed up your financial freedom journey!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you are looking for a book to help you achieve FIRE (financial independence and retire early), then “The Simple Path to Wealth” is the perfect read for you. I read it and found its principles to be very true and applicable.

J.L. Collins wrote this book, providing a step-by-step guide on building wealth and achieving financial freedom.

In this blog post, we will discuss some of the key takeaways from this book and share our own experiences with it!

This post may contain affiliate links; please see our disclaimer for details.

Keep Things Simple

Pursuing financial freedom may seem like a daunting task. After seeing how others achieved FIRE (financial independence/retire early), it seems like one needed a complex strategy and luck.

However, “The Simple Path to Wealth” shows that FIRE is achievable for anyone willing to commit to it for the long term. The book breaks down the process of building wealth into simple steps anyone can follow.

One of the most important lessons from this book is to keep things simple. Collins advocates using a simple investment strategy that doesn’t require constant monitoring or worry.

Rather than getting caught up in researching every possible investment, he recommends keeping it simple. This approach removes the stress of making complex investment decisions and allows you to focus on other things.

When I could keep my investing process simple and automated, I could focus on my career and generate more income. With more income, I could invest at a much higher rate which ultimately led me to become financially free sooner.

I share this story with you because it feels like many people seeking FIRE try to over-optimize their investment strategy. While there’s nothing wrong with being diligent, don’t forget to keep things simple as well.

Use Tools of The Trade, AKA Index Funds

When I say trade, what I mean is index funds. It’s important to look at stocks as ownership in a company, not just a gambling vehicle.

If you’re looking to build wealth, index funds are one of the best tools at your disposal. Index funds are low-cost, diversified investments that track a specific market index. They offer many benefits, including:

Low fees: When you invest in an index fund, you’re not paying a high management fee to a professional. This alone can save you thousands of dollars over time.

Diversification: Index funds expose you to hundreds or even thousands of different companies, reducing your risk.

Simplicity: Index funds are simple to understand and easy to invest in.

If you’re new to investing, index funds are a great start. They offer a simple way to build wealth over time and don’t require much maintenance. I started investing in index funds when I first started with FIRE, and they have been a crucial part of our ongoing journey to financial freedom and peace.

Income > Expenses = Invest The Rest

The author recommends keeping your expenses low so that you can invest more. This can be a real eye-opener since many feel FIRE is achievable only for those with a high income.

However, after reading “The Simple Path to Wealth,” you can realize it is possible to achieve FIRE or financial freedom without stressing about moving up the tax bracket.

As long as your income is more than your expenses and you stay consistent with investing the rest, you will eventually reach financial freedom. It might take longer if your expenses are high, but it is still achievable.

My wife and I are on the way to FIRE by keeping my expenses low and investing the rest of our combined incomes. This allowed us to save a Save 56% of Our Income and will allow us to reach financial independence sooner.

As mentioned before, this simple formula helped me focus on achieving a higher income. Cutting expenses help widen the gap between income and expenses and are key to reaching FIRE. If you want financial freedom, I recommend using this simple formula.

This might seem common sense, but the complexity and need for perfectionism often deter people from taking action.

If you can keep it simple and focus on income > expenses = invest the rest, you will be well on achieving FIRE. It’s not the most exciting process, but it’s simple and works.

Plus, when you achieve FIRE, you’ll have much more time and freedom to do what truly excites you!

Credit cards have become the norm. Mortgages, car loans, personal lines of credit, layaway, etc., have also been a part of most people’s lives.

We’ve become so used to being in debt that it seems normal. It’s not. It’s one of the biggest impediments to wealth building.

When you’re in debt, you’re paying interest on the money you’ve already spent. This is money that could be working for you and helping you build wealth. Instead, it’s being used to line the pockets of the lenders.

Imagine how much extra money you could be investing if you didn’t have a debt burden. It’s financially harmful and can also affect your mental and emotional well-being.

You must get out of debt if you’re serious about building wealth. The author explains that if the debt has an interest rate of less than 3%, it’s okay to let it ride and invest instead. If the interest rate is 3-5%, you can pay it off early or invest. If it’s 5% or above, it should be paid off as soon as possible.

Getting out of debt is one of the best things you can do for your financial future. It will free up money that you can use to invest and save.

It will also reduce your stress and give you more peace of mind. If you’re currently in debt, plan to get out as soon as possible.

Create a Plan and Stay the Course

Another important lesson from the book is the importance of creating a plan and staying the course. There will be ups and downs when you’re working towards financial freedom.

There will be times when you feel like you’re making progress and times when it feels like you’re not moving. It’s essential to have a plan and stick to it, even when things get tough.

Creating a plan is the first step. You need to know how much money you need to save and invest each month to reach your goal.

Once you have a plan, it’s essential to stick to it. Even when things get tough, remember why you’re doing this and keep moving forward. Remember, there are ways that you can enjoy your FIRE journey.

If you can stick to your plan and weather the storms, you will eventually reach your goal of financial freedom. It might take longer than you originally planned, but it will be worth it in the end.

As soon as I sat down and started to budget and wrote down how much I needed to achieve financial freedom, it became much more straightforward. I could stay the course even when there were setbacks because I had a plan and knew where I was going.

Trying to achieve FIRE without a plan is like driving to a new city without a map. You might eventually get there, but it will take longer and be more complicated than if you had a plan.

So, if you’re serious about reaching financial freedom, sit down and create a plan. Then, put it into action, and don’t give up! You’ve got this!

Conclusion

To summarize the book, it’s essential to keep things simple, get out of debt, and create a plan. These are the three main lessons I took from the book and helped me on my journey to financial freedom.

If you’re looking for a simple, straightforward guide to wealth building, I highly recommend “The Simple Path to Wealth” by JL Collins for anyone looking to achieve FIRE. It’s helped me greatly, and I’m sure it can help you too.

What are your thoughts on the book? Have you read it? What lessons did you take away from it? Let me know in the comments below.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Breaking the chains of poverty can be a difficult task. It requires hard work, dedication, and, most importantly, change. The ten poor habits outlined in this article are commonly seen in those struggling financially.

If you want to improve your financial situation, it is important to break these poor habits and replace them with positive ones!

This post may contain affiliate links; please see our disclaimer for details.

1) You Don’t Have a Plan

How do you expect to achieve your financial goals if you don’t have a plan? Having a budget is one of the most important things you can do for your finances.

A budget allows you to track your income and expenses and adjust as needed.

2) You Live Paycheck to Paycheck

This is a common habit among those who are struggling financially. If you’re living paycheck to paycheck, you’re not saving money. It then becomes difficult to build an emergency fund or save for other financial goals.

To break this habit, you need to start budgeting and making a plan for your finances. Begin by setting aside money each month to save.

Even if it’s only a small amount, it can make a big difference in the long run.

3) You Have High Debt Levels

Another common habit among those who are struggling financially is high debt levels. This can make it difficult to manage your finances and make ends meet.

If you have high debt levels, it is important to create a plan to pay it off. Begin by making a list of all of your debts and their interest rates. You can focus on paying off the debt with the highest interest rate first or focus on paying off the smallest debt amount first with the Debt Snowball Method.

As you progress, you can start working on paying off the other debts.

4) You Don’t Invest

Investing is one of the most important things you can do for your finances. It allows you to grow your money over time and build wealth.

However, many people who are struggling financially don’t invest. This is usually because they don’t have the money to invest or don’t understand how it works.

If you’re not investing, it’s time to start. Begin by setting aside a small amount of money each month to invest.

You can then use this money to purchase stocks, bonds, or other investment products. As your investments grow, you’ll be on your way to building wealth.

5) You Don’t Have an Emergency Fund

An emergency fund is a savings account that you use to cover unexpected expenses. This could include medical bills, car repairs, or job loss.

Many people who are struggling financially don’t have an emergency fund. This can leave them in a tough situation if they experience an unexpected expense.

It would be best to start saving for an emergency fund to break this habit. Begin by setting aside a small amount of money each month. Doing this will help you build up enough savings to cover unexpected expenses.

My wife and I set up automatic transfers to a high-yield savings account, our Emergency Fund. It provides us with great peace of mind knowing we are prepared for the worst.

A great place to get started with your savings account isCIT Bank. They offer very competitive saving rates with no monthly maintenance fees.

With their Saving Connect Account, you can earn 12x the national average! There are no ATM fees, and you have the convenience of online banking.

If you don’t have a retirement plan, it’s time to start one. A retirement plan is a savings account used to save for retirement. Many people who are struggling financially don’t have a retirement plan. This can make it difficult to retire when you’re ready.

You must begin saving for retirement at the earliest possible age to break this bad habit. Start by setting aside a small amount of money each month.

By building up your retirement savings, you’ll be on your way to a comfortable retirement.

Increasing your income is essential to your financial freedom. Many individuals who are struggling financially suffer from this issue. It often stems from a limited belief about their earning potential.

In this situation, looking for ways to increase your income is important. This could include getting a better-paying job or starting a side hustle.

Making more money is a great way to break the cycle of poverty. If you can find ways to increase your income, you’ll be on your way to financial success.

An excellent way to increase your PASSIVE income is by renting out extra space! With NEIGHBOR, you can easily rent out extra space, such as your garage, self-storage unit, rooms, etc.

From neighbor.com

8) You Don’t Have or Stick to a Budget

If you don’t have a budget, it can be not easy to manage your finances. A budget is a plan for your money that helps you track your spending and ensure you’re not overspending.

Many people who are struggling financially don’t have a budget. This can make it difficult to stay on track with your finances.

To break this habit, you need to create a budget. Begin by tracking your spending for one month. This will help you see where your money is going and how much you spend each month.

Once you understand your spending well, you can create a budget that will help you stay on track.

9) You Don’t Stay Disciplined

Discipline is essential for financial freedom. It can be not easy to manage your finances without out. This is a common problem for many people who are struggling financially.

In this situation, it’s important to find ways to stay disciplined. This could include things like setting up a budget or tracking your spending. Staying disciplined is a great way to break the cycle of poverty.

10) You Don’t Live Within Your Means

Making ends meet can be difficult if you don’t live within your means. Finding ways to cut back on your spending is important in this situation. This could include things like eating out less or downsizing your home.

Poor spending habits can often be caused by insecurity or not having delayed gratification.

For example, if you want something but can’t afford it, you may be tempted to put it on a credit card. This can lead to debt and further financial problems. If you’re struggling to live within your means, finding ways to curb spending is important.

There are some simple rules that you can follow to help live below your means. The 50/30/20 rule is one such rule.

The method states that you should allocate 50% of your income toward essentials, 30% towards wants, and 20% towards savings.

All in All

These are just a few of the common habits that keep you poor. If you want to improve your financial situation, it is important to break these poor habits and replace them with positive ones.

If you break these habits, you’ll be on your way to financial success!

A plan to achieve your financial goals, budgeting, investing, saving, living within your means, and paying off debt are great ways to start. Breaking the chains of poverty can be difficult, but it is possible.

With hard work and dedication, you can achieve your financial goals. So don’t give up and keep working towards your goals. You can achieve anything you set your mind to.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.