This post may contain affiliate links; please see our disclaimer for details.

According to Pew Research Center, “most rental properties – about seven in ten – are owned by individuals, who typically own just one or two properties.” Many real estate investors are out there, but not all of us have the proper training.

Reading real estate books can help you avoid costly mistakes and accelerate your progress toward building wealth.

That’s why I’ve chosen five must-read real estate investing books that can give you a solid foundation for real estate investing and open up your investing mindset.

The general aim of real estate investing is to help you own properties and build passive income each month.

A real estate investor can more easily start investing and managing tenants after reading these books and implementing the lessons and strategies taught.

A great way to start investing in real estate without a lot of money is with Fundrise, a crowdsourcing real estate investing platform.

With investment minimums of ONLY $10, you can start making PASSIVE INCOME with your real estate investment portfolio!

Let’s dive in and see why these 5 real estate books can help you become an expert in real estate investing.

Top Real Estate Investing Books

The Millionaire Real Estate Investor

Buy, Rehab, Refinance, Repeat

The ABC’s Of Real Estate Investing

One Rental At A Time

Every landlord’s Legal Guide

1) The Millionaire Real Estate Investor – Gary Keller

The author, Gary Keller, created the impressionable saying, “ANYONE CAN DO IT… but not everyone will… will you?”.

Beginners should understand the proverb Keller shared before investing in real estate. You must prepare yourself and your mind to be like a millionaire, but don’t worry because Keller has you covered!

Real Estate Investor Stories

The book describes the financial journeys and success stories of 100+ millionaires, so a ton of valuable information is shared about the mistakes and successes of real people.

Keller stated in his book that 90% of millionaires become millionaires by investing in real estate.

In his book, the author helps you learn how to make your mindset similar to a millionaire and have a solid investing strategy. This includes tips on how to generate leads and much more.

Some Strategies Taught in His Book

Everyone needs an investing strategy. Beginners have an excellent opportunity to invest individually (without joining others).

How to NOT make a lousy deal.

Create strategic criteria when you are an investor, and only invest when a deal fits your criteria.

This book also shows how you can apply specific techniques to grow your cash flow and increase real estate equity.

This book is great for any beginner or advanced real estate investor; get your hands on a copy today!

2) Buy, Rehab, Rent, Refinance, Repeat – David M. Green

The method of BRRRR is very easy for the investor if you are starting and purchasing your first residential property.

By reading this book, you can learn what ‘Book Buy, Rehab, Rent, Refinance, Repeat’ means and apply the author’s proven plan. Here is a quick recap of each step.

Buy

Your buying strategy should include having the property in a good location with great potential for solid renters. Green will dive into the specifics in his book, including how to buy a property with limited resources.

Rehab

When you start renovating your property, it will increase the value of your property. Good renovations will focus people’s attention and motivate them to rent. Green will give valuable reasons and tips on how to increase the property’s value greatly.

Rent

When the property is well designed and maintained (renovated), make it available for rent. Start depositing the property rental income into your account and create a healthy cash flow.

Refinance

Learn about holding periods and other tips regarding when and how to refinance the property.

Repeat

Lastly is to buy another property based on the BRRRR strategy. By doing this, you will earn and learn more and, one day, become very successful and wealthy from your investments.

You’ll want to check out this book to learn more about effectively implementing the BRRRR method – the method my wife and I have been using and finding much success. 🙂 You can also see our personal story and insights in this article I wrote: The Ultimate BRRRR Method Real Estate Investing Guide.

3) The ABCs of Real Estate Investing – Ken McElroy

Ken McElroy tells us not to accept any information blindly but always to verify it. Especially in real estate, verifying key information first is vital to making a great purchase and long-term investment.

Find and Understand Market Trends

Why does ken McElroy check the trend first? Because before buying a property or investing money in the market, you must check the market trend rather than the property price only.

The Basic Rules…

The market is more critical than the property. The value of the call depends upon the market value and not the property.

Don’t rely on the gut feeling. The rule of real estate investing – find the facts.

Look for a suitable investment like dating.

McElroy teaches many more methods that can help you identify the best investments using basic math, which will help you know when to buy, how long to hold, and when to sell.

Become an expert and obtain a solid investing foundation by following his methods and steps today!

4) One Rental at a Time – Michael Zuber

This book is about how the author worked a normal job but wanted financial independence.

He made that dream a reality by investing in real estate, sharing many experiences on how he could gain back 20 years of financial freedom.

Zuber will inspire those who are busy professionals and prove that real estate investing is possible, no matter how busy you are.

He explains what decreases and increases the value of a rental and much more.

See more of his inspiring story and how you can invest serious wealth in one rental at a time.

5) Every landlord’s Legal Guide – Marcia Steward, Janet Portman, Ann O’Connell

This book has you covered when it comes to the legal aspects of managing a rental or multiple rentals as a Landlord. I’ve learned from our personal experiences that it’s important to know the legalities and treat your rental as a business; trying to be a friendly landlord will not cut it.

You will learn the best and safest ways to deal with tenants. Here are some key lessons taught –

The 5 books mentioned in this article will help you learn from others’ mistakes and successes, be a great landlord and give you a solid foundation for real estate investing.

Follow the methods taught in our top 5 real estate investor picks and become an excellent real estate investor in 2022!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

This post may contain affiliate links; please see our disclaimer for details.

Our 2022 Financial Goals

With 2022 underway, we’ve taken some time to set our top 5 financial goals for 2022 with our plan to achieve them. We hope our goals and plans can provide you with some inspiration as you work towards a life filled with joy and financial peace.

Our Top 5 Financial Goals For 2022:

Read 3 finance books.

Emergency fund hit $15,000.

Total investment accounts hit $93,000.

Total net worth hit $430,000.

Under contract for another house.

How We Plan to Achieve Each Goal

1. Stay focused on our WHY

Sometimes it can be hard to see other people buy a nice car or go on a trip to a fun place, buy a lot of great gifts for Christmas, etc., and you want it too!

So here’s our why that we need to remember when times get tough –

Both my wife and I’s financial goal is to hit FIRE (finance independence retire early) one day. We don’t want to be stuck with 9 to 5 jobs until we are 50, 60, or even 70. We truly hope we can retire early to be able to spend a lot of time with family and be free.

Try thinking about and writing down your financial goals for the next year, and for the next 2, 3, 5, or 10 years to come.

Writing down and remembering those goals is crucial because it gives you an empowered mindset and can help a lot when feeling overwhelmed.

When things get tough, remember the pain is not going to last forever, it is temporary.

Short-term pain brings long-term happiness, I think this type of sacrifice is very worthwhile.

For example, my wife said that when she looks back she has forgotten how painful delivering a baby was. She just remembers how cute the baby is and how grateful to have our lovely children now.

Having a baby is much harder but the point is things that are worth it in life don’t come easy.

Set meaningful goals and work hard to achieve them. This is vital to finding success and is also a driving force that will support you.

2. Save and budget

“Don’t save what is left after spending; spend what is left after saving.”

Warren Buffett

For our Emergency Fund, we have an automatic transfer every month of $400 which should help us reach the goal of $15,000 by year-end.

As for our investment accounts, we have just maxed out our Roth IRA contribution amount for 2022. For more on this see Our Top 2022 Investments.

Imagine two people, someone who makes $100,000 a year and spends all of it. Then someone who makes $50,000 a year but only spends $30,000 and invests $20,000.

Which one do you feel is on the path to financial freedom and building net worth?

High income does NOT equal wealth. Knowing how to save, budget, and invest wisely are skills of the wealthy. Learning takes time and commitment, we are still learning new things and doing our best to save and budget.

One way we like to save money is by using an affordable phone plan.

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

Life is a journey of learning lessons, and we have learned this first hand. We learned the importance of learning quickly from mistakes and facing life optimistically.

The mistakes we made were very tough at the time but we need to accept our failures as valuable lessons and do our best to avoid them in the future.

Although hard at that moment, when you look back a long time later you might be thankful for those failures.

Failing is not terrible, what is really terrible is that you have not learned from the experiences.

“We need to accept that we won’t always make the right decisions, that we’ll screw up royally sometimes – understanding that failure is not the opposite of success, it’s part of success.”

Arianna Huffington

4. Be patient

The road to financial freedom requires patience and persistence.

My wife and I would also be envious when we see people who get rich overnight. Especially recently with the hot topic of cryptocurrency, many people benefited from it but many did not.

But neither of us likes to gamble. Gambling can become a scary addiction.

Someone with a lot of extra money could invest in these things but must be willing to lose it all.

We need steady investments because we have kids and families need to take care of.

When it comes to funds, we love the Total Market Fund and S&P 500 fund. If you don’t know what to invest in, they both can be a good starting point!

Compound interest is the most wonderful thing in the world, but it takes time and requires patience.

The main point is to start investing early and start now, you will see how miraculous it is and how it grows like crazy over time!

90% of our stock market investments are in a regular mutual fund, index fund, or ETF. 9% of our investments are in single stocks. Less than 1% is in cryptocurrency.

My wife and I want to be financially free ASAP too, but we keep telling ourselves to be patient.

So hopefully our plan to achieve our 2022 financial goals can be of use to you –

Remember your why

Save and budget

Accept failures as lessons

Be patient

Thank you so much for reading! We would love to hear your thoughts or questions – drop a comment below!

After first getting married to my sweetheart, both I and my wife are just college students and our net worth was way in the negative. A very large chunk came from student loans.

Through patience, continual learning, and persistence, we turned our net worth from a negative to a positive of $350,000. This happened during our 4 years and a half years of marriage.

This post may contain affiliate links; please see our disclaimer for details.

Photo by Monstera on Pexels.com – increase of net worth

Right now, my wife is 25 and I am 27 years old. We are completely debt-free except for our two real estate property loans.

We are excited to share with you today how we went from being in debt to having $350,000 net worth in 4 years during college.

Increasing one’s income is very important to getting out of debt and building one’s net worth. Making an extra $5000 is easier than trying to save $5000.

There are two main ways to increase your income.

First, find side hustles. Second, find a higher-paying job.

Side hustle experience

My wife and I love pets, and helping take care of others’ pets has been an excellent side hustle.

We would help friends or family out to watch their pets. My wife is from China, so many international students don’t have family here. We would help watch their pets while they go back to China.

For us, this was not a job at all, and we both enjoyed playing with each pet (by the way, we would only watch fully trained pets, so it wouldn’t be hard to take care of them).

We also enjoyed using the pet sitting site/app Rover; if interested, click HERE for more details.

We hope you can also find something you enjoy for a side hustle!

Find a higher-paying job

Making more money means you can save and invest more money!

In addition to doing side hustles, I have constantly worked on improving my skills in the workplace to be able to find higher-paying positions.

Back when going to school I would do both full-time school and full-time work.

Having full-time school and full-time work is no easy task. As many of you already know, it takes grit and perseverance, but don’t worry there is light at the end of the tunnel!

I moved up to a supervisor position when I first got married. Next, I was able to obtain an account manager position during the last year of my bachelor’s program. I then became a product development specialist after the first semester of my MBA.

In total, my salary increased by $30,000 (all while still going to school!).

The company I work at as a product development specialist is amazing. They even offered me $3000 each year of tuition reimbursement.

For my two years of studying for my MBA, I received a total of $6000 for tuition reimbursement.

2. Save and Budget

“It’s not how much money you make, but how much money you keep…”

Robert Kiyosaki

Imagine two people, someone who makes $100,000 a year and spends all of it and someone who makes $50,000 a year, only spends $30,000 and invests $20,000.

Which one is on the path to financial freedom and building net worth?

High income does NOT equal wealth. Saving and investing wisely are skills of the truly wealthy.

One way to save money is by using an affordable phone plan.

Mint Mobile has helped us save tons of money, especially during college! We all know how phone plans can get pricy with long, frustrating contracts.

Our friends told us about Mint Mobile many years ago. For many reasons, we are still using them today!

Mint Mobile offers amazing plans at incredible prices, with plans as low as only $15 a month! My wife and I pay only $15 monthly for our phone plans. Check out how you can save money with them today!

3. Pay off all debt except the mortgage

“Debt is the slavery of the free.” – Publilius Syrus

A lot of debt is being accumulated by individuals across the world each year.

According to business insider, the average American has $52,940 worth of debt across mortgage loans, home equity lines of credit, auto loans, credit card debt, student loan debt, and other debts like personal loans.

Debt is the enemy of saving!

Debt steals from the money you could be saved and invested!… when you need to pay $500 in debt payments a month, you are actually losing $500 that could have been extra investment each month.

When it comes to how to pay off debt, we are big fans of the debt snowball method and used it to pay off our $56,000 worth of student debt and had one kid.

The journey is not easy but is worth it.

We are 100% debt-free except for the mortgage. Staying away from debt allows us to save (and INVEST) more of our income and reach financial freedom sooner.

4. Invest in tax-advantaged accounts

Whenever we hear or see the word tax-advantaged, we pay special attention to learn all we can about it.

My wife and I love tax advantage accounts because we don’t want to worry about tax at all when we retire. The thought of being a tax-free millionaire in the future is exciting.

When you invest your money wisely, you can earn interest and dividends! You will be making money even while sleeping!

Compound interest is an amazing thing that can really go to work for you.

We highly recommend investing early and starting now. The growth may seem slow at first but it grows like crazy over time!

Check out this example below –

The average monthly student debt payment in the USA is around $400 a month. If you instead invest $400 a month in a reliable fund (like the S&P 500) with average an average return of 12%, you will have around $92,000 in 10 years and ONE MILLION in 28 years!

A great way to start investing is by putting money into some tax advantage accounts like 401Ks, HSA, IRAs, etc. Tax-advantaged accounts can save you a lot of money in tax!

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

Real estate investing, even on a very small scale, remains a tried and true means of building an individual’s cash flow and wealth.

Robert Kiyosaki

Real estate is a very hot investment topic and an incredible tool to help achieve FIRE (Financial Independence Retire Early).

Many think a lot of money is needed to start investing in real estate, but this is not always true.

You may have heard of people who have achieved great success in real estate investing. Our success may seem small to some but we would like to share our story.

In total, we have purchased three properties. We sold our our first property to help me graduate student debt-free.

At that time we were just regular college students. We did not have a lot of money and did not have high-paying jobs!

We started our real estate investment journey with only $20,000.

Now $20,000 has become $250,000 in 4 years while going to school.

So what was our real estate investment strategy?

Buy as owner-occupied (residential property).

Do some easy remodeling while living there.

Save up a downpayment for the next property.

Buy the next house and rent out the previous one.

The past few years have been a very good time to invest in real estate in Utah. We were able to buy a house when the price was still relatively cheap, and then watch it increase in value.

The value is still increasing and having rental income as passive income is an amazing thing!

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

After first getting married to my sweetheart, our net worth was in the negatives for sure, especially because of all of the student debt I had acquired.

Through patience, continual learning, and discipline, we have been able to turn our net worth into a positive number!

During our 4 years and a half years of marriage, we used the debt snowball method and investing to help me graduate student debt-free with my MBA and build a total of $350,000 net worth.

Right now, my wife is 25 and I am 27 years old. We are completely debt-free except for our two real estate property loans.

Before breaking down our $350,000 net worth, I want to share some interesting statistics.

This post may contain affiliate links; please see our disclaimer for details.

So what is the average net worth by age for Americans?

Let’s see the average net worth by age for Americans according to CNBC.

For those under age 35, the average net worth of Americans is $76,300.

For those ages 35 to 44, the average net worth of Americans is $436,200.

For those ages 45 to 54, the average net worth of Americans is $833,200.

For those ages 55 to 64, the average net worth of Americans is $1,175,900.

For those ages 55 to 64, the average net worth of Americans is $1,217,700.

For those ages 75 and above, the average net worth of Americans is $977,600.

What is Net Worth?

Net worth is the total value of all assets, minus the total of all liabilities.

In other words, net worth is everything you own minus all that you owe.

How to Calculate Net Worth?

Basically, the equation is NET WORTH = ASSETS – LIABILITIES.

Examples of Assets: real estate, checking accounts, saving accounts, retirement accounts, etc.

Examples of Liabilities: real estate loans, student loans, credit card debts, car loans, etc.

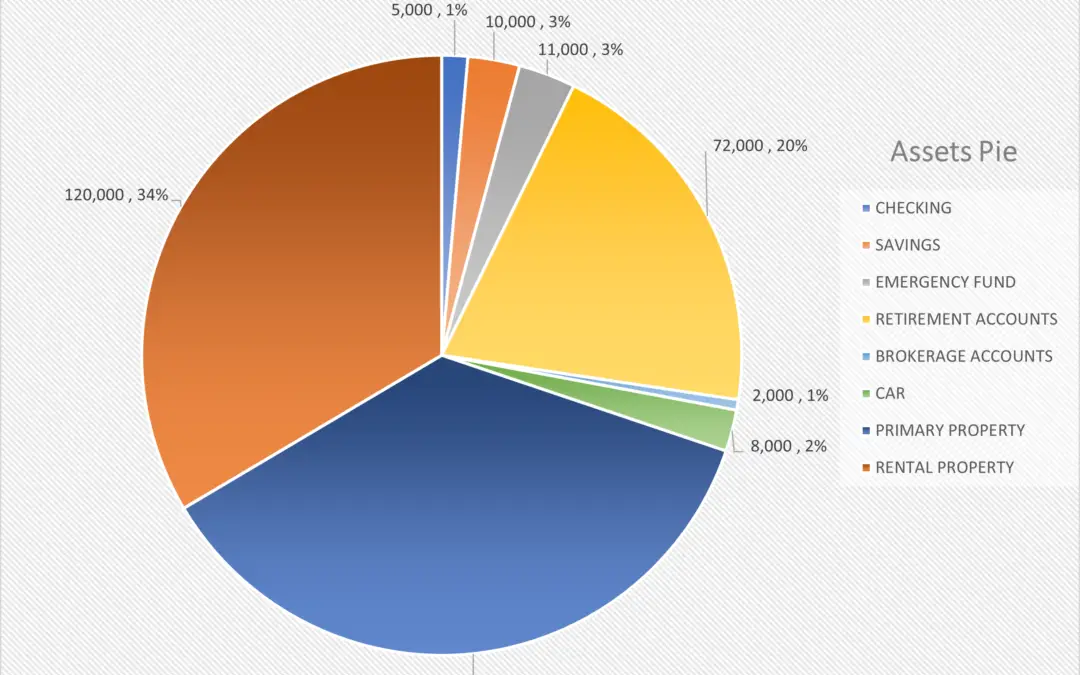

Our Net Worth Breakdown

Net Worth Pie Chart

1) Checking Accounts: $5000

We have two checking accounts, one for me and one for Shan. We have a total of $5000 combined between both of our checking accounts.

Our goal is to not put a lot of money into our checking accounts but is to keep a little more than our total monthly expenses.

2) Saving Accounts: $10,000

We also have 2 saving accounts, one for me and one for Shan. In total, we have $10,000 saved up for both of our savings accounts combined.

We use this money for big purchases such as saving up for a new home, travel, etc.

3) High Yield Saving Account AKA Emergency Fund: $11,000

We have one high-yield saving account which is also our emergency fund.

Each month we transfer $400 to our High Yield Saving Account / Emergency Fund and will continue to keep transferring money until we have enough savings to cover 6 months of expenses.

Having a fully-funded emergency fund is important to us and provides peace of mind.

4) Retirement/Tax Advantaged Accounts: $72,000

We have two Roth IRA accounts, both of which we max out each year.

One roll-over IRA account is from 2 of my previous employers’ traditional 401K accounts.

We then have two Roth 401K accounts with each of our current employers and contribute enough to our company’s Roth 401Ks to get the company match.

We also have one HSA saving account. My wife and I are on separate health insurance plans. I have an HDHP plan and my company matches part of the money that I put into my HSA. I max out my HSA every year because it has triple tax benefits and can also be a secondary/regular retirement account when you are 65 years old.

Combining all of those retirement accounts totals, we have $76,000.

5) Brokerage Accounts: $2,000

Right now we have one brokerage account and only invest $100 each month in it. We want to invest more in tax-advantaged accounts so that’s why we do not invest a lot in our brokerage account at the moment.

One car works great for us, we are very fortunate. My wife works from home permanently and I am on a hybrid schedule where I work in the office on certain days and from home on other days.

To be honest, we both don’t like to count the car as our asset because it decreases in value.

Generally speaking, the car should account as your asset.

7) Primary Residential Property: $130,000

We built a single-family house which is our primary residential property right now.

The new home was under construction in July of 2020. The building process was very cool and took ten months to finish.

Finishing our entire yard took two months after we moved in. We soon after welcomed our sweet Samoyed puppy named Tofu to the family! We finished our basement next.

Finishing a basement is a lot of work, but I’m learning many valuable handyman skills! A lot we did by ourselves but some parts were hired out.

After checking the current prices in our community, we found the equity in our home to be at least $130,000, especially with the basement and yard done.

8) Rental Property: $120,000

We have one rental property and sold our first townhouse rental a while back.

After first living in the condo for around two years we decided to rent it out. We also did some simple remodeling before renting it out.

Our rental property is giving us around $300 every month in cash flow now.

We checked condos in the same community and can say we have at least $120,000 house equity in it.

Side note: when calculating net worth for home loans you take the current market value minus what you owe on the loan.

Checking Accounts

$5,000

Savings Accounts

$10,000

High Yield Savings Accounts / Emergency Fund

$11,000

Retirement / Tax-advantaged Accounts

$72,000

Brokerage Accounts

$2,000

Car

$8,000

Primary Residence Property

$130,000

Rental Property

$120,000

TOTAL

$358,000

Net Worth Chart

“When you invest, you are buying a day that you don’t have to work.”

Aya Laraya

The past few years have been a very good time to invest in both real estate and the stock market.

We were able to buy a house when the market was slightly cooler, and then watch it increase in value.

The value or equity is still increasing and having rental income as passive income is an amazing thing!

We are so grateful we have been able to make $250,000 profits from our real estate investments with just $20,000 starting in 4 years during college.

We believe diversifying investments is extremely important and not just for real estate. Investing in tax-advantaged accounts is also very important in building our net worth.

Thank you for reading! Please drop a question or comment below – we’d love to hear your thoughts.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

If you haven’t already, make sure to contribute to your 2022 IRA!

What better way to ring in the new year than by contributing to your investment accounts. We are so excited to share that we just maxed out our Roth IRAs $6000 each, for a total of $12,000!

This post may contain affiliate links; please see our disclaimer for details.

A Roth IRA is an amazing FIRE friend to have on our fire journey.

Before sharing our investment choices, let’s walk through some important information first!

The 2022 contributions limit for Roth and traditional IRAs is $6,000 if you are under 50 years old or $7,000 if you are 50+. You must have enough earned income to cover the contribution.

Example: If you only made $1000 in 2022, you can only contribute up to $1000 to your IRA in 2022.

In 2022, the annual income limit is $144,000 for single and $214,000 for married filing jointly. This means if you are above that income, you will not be able to contribute to the IRA.

The deadline to max out an IRA each year is typically the same as the filing tax return deadline – April 15.

For example, you can still contribute to your 2021 IRA up until April 15, 2022.

What is a Roth IRA?

A Roth IRA is an Individual Retirement Account where you can contribute after-tax dollars.

Contributions and earnings can grow tax-free. Withdrawals of the money can be tax-free and penalty-free if certain conditions are satisfied. For example: if you are the age 59½.

We come from different walks of life and are in different financial situations. It’s important to know the differences between a Roth IRA and Traditional IRA before choosing one (or both).

My wife and I chose the Roth IRA because we don’t want to worry about taxes when we retire.

The thought of being a tax-free millionaire in the future is exciting. After paying off our student loan debt of 56K, we started to max out our two Roth IRAs for a total of $12,000 a year.

Where to open a Roth IRA?

There are many different places to open an IRA, but we highly recommend using M1 Finance.

M1 Finance is a great investment opportunity with its robust yet simple app. There are ZERO commissions or account management fees.

Deposits $1,000 or more into your M1 Invest account within two weeks of signing up and get a cash bonus of $30-$500 to that account.

It is not just a trading stock brokerage account but also offers an IRA option that allows you to invest in your retirement.

We highly recommend using M1 Finance to open a brokerage or retirement account! M1 Finance can undoubtedly help you on your financial independence journey.

The goal of FZROX is to provide investment results corresponding to the total return of a broad range of U.S. stocks.

The expense ratio is very low at 0!

As of 12/31/2021, the average one-year return rate is 26.01%, 3-year return is 25.81%.

“There will be good years and there will be bad years, but the compounding will continue on unabated.”

Pietros Maneos

Compound interest is one of the most wonderful things in the world. Start investing early; no matter how small, and you will see how miraculous those investments grow over time.

Thanks for reading! We’d love to see which investments you have chosen for your IRA(s) in 2022!

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

When buying a new home from a builder you’ll notice there are many different upgrades to choose from – this can be both very exciting and overwhelming. This is our story where we identify six smart upgrades to consider when building a new home.

This post may contain affiliate links; please see our disclaimer for details.

Third Property Under Construction – Choosing Smart Upgrades

Our third real estate property is a brand-new single-family home. We went through a builder and chose some smart upgrades for investing.

Construction began in July of 2020. The building process was very cool and took ten months to be finished. We officially closed on our new home in May 2021!

The most fun and exciting part for us was choosing upgrades for the exterior and interior of our new home.

A design center was available where we can choose options and upgrades the builder has available.

Many basic options were available where we did not need to pay anything extra – each builder is a little different on which options are free and which options are considered a paid upgrade.

We didn’t want to max out our loan and become ‘house poor’ so we did our best to stay calm at the design center – this was tough at times!

There are so many attractive upgrades that initially made us want to spend more money, but not all were smart upgrades that would add value in the long term.

Only select the most necessary and smart upgrades.

These types of upgrades give the property more value, making it a better investment property in the future.

We first looked at a lot of different new home construction builders and the floor plans for each of their home models. Each builder offers different sizes of homes with different floor plan layouts for each one.

For example, a floor plan will show if a kitchen island is already included or if it can be added as an upgrade. Some models included granite countertops while others did not.

Make sure to ask your builder what is included in the base price for each model.

Getting Started: Structural vs Non-Structural Upgrades

New home upgrades are divided into two categories: structural and non-structural.

It’s important to consider structural upgrades first. Structural upgrades affect the structure of the new home and will need to be decided at the beginning of construction.

An example of a structural upgrade is to put a vaulted ceiling in the master bedroom.

Changing anything to the structure of the home after it is finished will be a big project and cost a lot of money.

Non-structural upgrades are more decorative and usually will be easier to change in the future.

For example – lighting fixtures or a kitchen backsplash. Adding these types of non-structural upgrades yourself can save you a lot of money.

Here are the 6 smart upgrades you should consider when buying a new home. We’ve added a bonus #7 as well!

Smart Upgrade #1 – Kitchen

The kitchen is without a doubt an important focal point of a home.

If you plan to rent out or sell your home in the future, a beautiful kitchen will go a long way to attract potential renters or buyers.

We did a total of 4 upgrades for our kitchen:

Kitchen Island

Having a kitchen island has always been my wife’s dream. Our past two real estate properties did not have one.

Many new house construction builders include kitchen islands in the basic home models, but ours did not. So to include it was an upgrade but totally worth it.

Not only is it attractive to future renters or buyers, it made my wife happy! Happy wife = happy life. 🙂

Granite Countertops

We upgraded our kitchen countertops to be granite countertops, including our kitchen island.

This upgrade was one level above the most basic countertop type but very worth it since granite is durable and lasts a long time. It can also withstand a high level of heat.

Upgraded Cabinets

The type of cabinets included in the basic plan was older looking with only a couple of color options.

We upgraded to the next level of cabinets that were smooth and more stylish. We were also able to choose a light gray color that coordinated great with our floors.

Staggered Cabinets

Having high cabinets always look so nice, but is so expensive to upgrade to have taller cabinets. The person at the designer center told us we can do staggered cabinets, meaning only a few cabinets will be a little higher than others.

This sounded like a great option and looked very nice. More important is it only cost around $150!

For this price, we had no reason to refuse, haha.

Smart Upgrade #2 – Laminate Floors

Many builders, including our own, have carpet in the living room area as the basic plan. We felt it necessary to upgrade to laminate floors on the entire first floor.

Laminate flooring looks just like a wood floor and improves the look of the home.

When you decide to rent or sell, it will be more stunning in the pictures and more attractive for buyers or renters.

Laminate floors are also easier to clean compared to cleaning carpets. Especially when pets are in the picture!

We got a Samoyed puppy named Tofu after 2 months we moved into our new home. The laminate floor saved our lives during the potty-training process.

Our plan originally was to upgrade to LVP floors which are waterproof and scratchproof. Turns out it was pretty expensive for this upgrade. With our builder, it would have cost $5000 to convert our kitchen, dining room, and living room area to LVP flooring.

We then asked to see how many house buyers did the LVP upgrade. He said in his memory he only knows 2 or 3 house buyers who upgraded to the LVP floor. Basically, 99% did laminate flooring and had no issues even with pets.

We followed his direction and haven’t regretted it!

Smart Upgrade #3 – Lighting

We do not recommend spending money to upgrade your lighting fixtures but some common areas do need more lighting to make your house brighter during the night. One such area is the living room.

No one wants the house to be dark when friends come to play, or when children play with toys or read books.

There will never ever be too much lighting in your home. Having adequate lighting in all suitable places is essential for everyone in the house’s comfort and enjoyment.

Our builder also said that whenever they make a spec home, they will add 4 can lights in the living room. We felt this was a wise and smart upgrade for our new home.

Smart Upgrade #4 – Vaulted Ceiling

As mentioned before, making a ceiling vaulted is a structural upgrade. If you want this upgrade make sure the builder knows sooner or later since it would be a huge project to change in the future.

My parents own a rambler (two-level house). They have a vaulted ceiling on the main level. Their living room, dining room, and kitchen feel very spacious and open.

Our house is a three-level house, and we had the option to upgrade our master bedroom to have a vaulted ceiling.

Many home models had a large master bedroom. For example, the model home created by our builder had a vaulted ceiling that looked very nice.

Our home model however is the smallest one the builder offers in our community, so our master bedroom is much smaller. We felt it is was not worth it to spend a lot of money on the vaulted ceiling upgrade for a small master bedroom.

If we were in a similar home as my parents or had a large master bedroom then we would definitely consider upgrading to a vaulted ceiling.

Smart Upgrade #5 – Water Softener

I don’t know what your area or city is like, but we here in Utah have hard water. Adding a water softener is very important to protect your pipes and appliances.

The two properties we bought before did not have any water softener. One is a townhouse built in 1970 and the other one is a condo built-in 2002. We could see how the water has left many hard water stains.

Considering the long-term, water softener saves will help save money.

With our builder, it costs $1900 to install a water softener with everything.

If you are a handyman or have a handyman family member or friends, you can choose to just do the rough-in and then install the main water softener appliances by yourselves later after you moved.

This would definitely be the most cost-effective option. For our builder, the rough-in only cost $300.

Smart Upgrade #6 – Railing

Many builders will not offer a railing for free but have a mini wall instead. Having a nice see-through railing is a paid upgrade but does make a home feel more open and spacious.

Someone we know bought a new townhome that has an open-to-below ceiling in the living room. He upgraded the railing going up the stairs which looks amazing.

We don’t have an open-to-below living room and do not feel it is worth it to spend the money to upgrade for our type of model.

We love open-to-below living room designs and it’s our dream to build a house that has an open-to-below living room in the future. If in the future we really have a chance to build our dream home, we will upgrade the railing for sure!

Bonus Smart Upgrade #7 – Basement Apartment

These two structural smart upgrades are important if you’re thinking about renting out your basement: separate entrance basement door and rough-in plumbing.

Planning for those in advance will save your time and money.

Imagine having to drill through concrete in a basement to add a separate basement entrance door and piping. That doesn’t sound easy or cheap!

Recap of all 7 smart upgrades

Kitchen Upgrades

Laminate Floor

Lighting

Vaulted Ceiling

Water Softener

Railing

Bonus – Basement Apartment

We know many people who have maxed out their loans when buying a home. They all have a very high DTI (debt to income ratio) which ends up around 45%.

Don’t let that happen to you!

45% of your pre-tax income all going to debt?! This is a big NO-NO for us.

When applying for our house loan our goal was to keep all house costs (mortgage+utilities+internet) under 30% of our net income.

30% with everything included is a healthy percentage. We don’t want to max out our house loan debt because we’d rather not be house poor and have healthy cashflows.

By keeping our mortgage payment as low as possible we are able to have extra cash to save and invest – woohoo!

When you walk into the designer center, remember your budget, and stick with it!

I still remember the builder telling us how if we spend $5,000 more on upgrades, that breaks down to around $25 a month for 30 years.

This is a trap! Having too much debt is a trap.

Our builder gave us seven days to change our upgrades without any additional fees. If your builder does the same, then you have a ‘calm down’ period to consider what is most necessary and suitable for your family after you go home. We took away a few things that we didn’t feel were necessary within those seven days.

We’d love to hear what smart upgrades you’ve done! Please leave a comment or question below.

Disclaimer:

We hope the information in this article provides valuable insights to every reader but we, the Biesingers, are not financial advisors. When making your personal finance decisions, research multiple sources and/or receive advice from a licensed professional. As always, we wish you the best in your pursuit of financial independence!

Greetings from the Biesingers! Welcome to our financial independence retire early (FIRE) blog! We are so excited you are here and to share valuable financial freedom and health content with you. For more information about us, click HERE.